FactSet (NYSE: FDS) beat Wall Street expectations in Q1 Fiscal 2026, reporting adjusted diluted EPS of $4.51 (vs. consensus of $4.36) and GAAP revenues of $607.6 million (vs. consensus of $600.8 million), a 6.9% year-over-year increase. Shares rose approximately 3% in pre-market trading on December 18, 2025, following the announcement.

About FactSet Research Systems

FactSet Research Systems (NYSE: FDS | NASDAQ: FDS) is a global financial digital platform and enterprise solutions provider headquartered in Norwalk, Connecticut. Founded in 1977, the company delivers integrated data, analytics, and workflow solutions to buy-side and sell-side financial professionals, wealth managers, private equity firms, and corporate clients. FactSet combines proprietary financial data with third-party sources and advanced AI tools to streamline decision-making across the investment lifecycle.

As of Q1 Fiscal 2026, FactSet serves more than 9,003 clients and over 239,863 individual users in more than 19 countries, and is a member of the S&P 500. The company reported a market capitalization of approximately $10.9 billion ahead of the Q1 earnings announcement, and its employee headcount stood at 12,886 as of November 30, 2025, up 2.5% over the prior year. FactSet pays a quarterly dividend of $1.10 per share, with a 91% client retention rate and an annual ASV retention rate exceeding 95%.

Top Financial Highlights

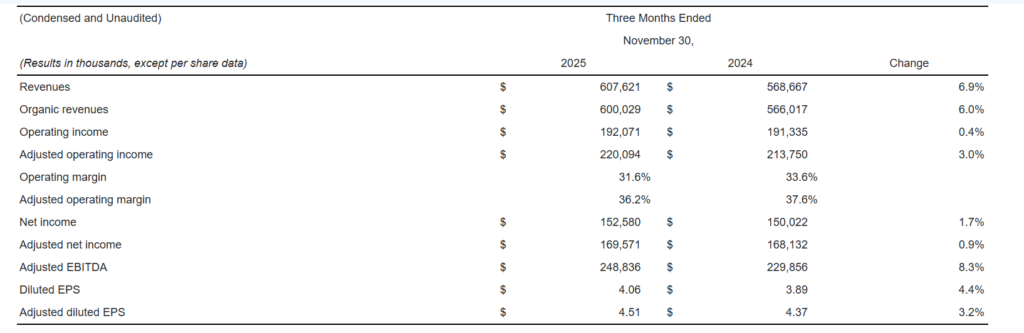

- Total GAAP Revenue was $607.6 million, up 6.9% year-over-year

- Organic Revenue grew 6.0% year-over-year to $600.0 million

- GAAP Net Income was $152.6 million, up 1.7% from $150.0 million in Q1 FY2025

- GAAP Diluted EPS increased 4.4% to $4.06 from $3.89 in the prior year period

- Adjusted Diluted EPS rose 3.2% to $4.51 versus $4.37 in Q1 FY2025

- Adjusted Operating Income increased 3.0% to $220.1 million

- GAAP Operating Margin declined approximately 200 basis points to 31.6% from 33.6%

- Adjusted Operating Margin was 36.2%, down 137 basis points from 37.6%

- Adjusted EBITDA rose 8.3% to $248.8 million

- Free Cash Flow surged 49.5% year-over-year to $90.4 million

- Net Cash from Operating Activities grew 40.4% to $121.3 million

- Organic Annual Subscription Value (ASV) reached $2,389.6 million, up 5.9% year-over-year

- Cash and Cash Equivalents stood at $275.4 million as of November 30, 2025

- FY2026 Revenue Guidance reaffirmed at $2,423 million to $2,448 million; Adjusted EPS guidance of $16.90 to $17.60

Key Financial Measures

Beat or Miss?

| Metric | Reported | Estimated | Analysis |

| Adjusted Diluted EPS | $4.51 | $4.36 | Beat by +2.7% above consensus |

| GAAP Revenue | $607.6M | $600.8M | Beat by +1.4% |

| Organic Revenue Growth | 6.00% | 5.12% | Beat consensus organic growth estimate |

| Adjusted Operating Income | $220.1M | $211.3M | Beat by approximately +4.2% |

| Adjusted Operating Margin | 36.20% | 35.80% | Margin above estimate, down YoY |

| Americas Revenue | $396.2M | $389.5M | Beat estimate by +1.7% |

| EMEA Revenue | $149.5M | $146.7M | Beat estimate by +1.9% |

| Asia Pacific Revenue | $61.9M | $61.7M | Marginally ahead of estimate |

What Leadership Is Saying?

“FactSet’s strong start to the year underscores the quality of our data and products and the strategic role our platform and analytical services play across the financial ecosystem. We see significant opportunity ahead and are executing with urgency to deliver tangible results, with three clear priorities: driving commercial excellence, increasing productivity, and advancing our long-term strategy.” – Sanoke Viswanathan, CEO, FactSet

“Our first quarter performance demonstrates the robustness of client demand and solid execution. We are investing thoughtfully in product and infrastructure to drive sustainable growth. At the same time, expanding our share repurchase authorization reinforces the conviction we have in our financial strength and the long-term value of our business.” – Helen Shan, CFO, FactSet

Historical Performance

FactSet Q1 FY2026 vs. Q1 FY2025 (Year-Over-Year)

| Category | Q1 FY2026 | Q1 FY2025 | Change (%) |

| GAAP Revenue | $607.6M | $568.7M | 6.90% |

| Organic Revenue | $600.0M | $566.0M | 6.00% |

| Net Income | $152.6M | $150.0M | 1.70% |

| Adjusted Net Income | $169.6M | $168.1M | 0.90% |

| GAAP Diluted EPS | $4.06 | $3.89 | 4.40% |

| Adjusted Diluted EPS | $4.51 | $4.37 | 3.20% |

| Total Operating Expenses | $415.6M | $377.3M | 10.10% |

| Operating Income | $192.1M | $191.3M | 0.40% |

| Adjusted Operating Income | $220.1M | $213.8M | 3.00% |

| Adjusted EBITDA | $248.8M | $229.9M | 8.30% |

| Free Cash Flow | $90.4M | $60.5M | 49.50% |

| Organic ASV | $2,389.6M | $2,256.7M | 5.90% |

Competitor Comparison

The following table compares FactSet’s most recently reported quarter (Q1 FY2026, ended November 30, 2025) against competitors’ most recently reported quarters. Note that competitor fiscal calendars differ from FactSet’s, so periods are not perfectly aligned.

| Company | Period | Revenue | YoY Revenue Change | Net Income / Adjusted EPS | YoY EPS Change |

| FactSet (FDS) | Q1 FY2026 (Nov 2025) | $607.6M | 6.90% | $4.51 adj. EPS | 3.20% |

| MSCI (MSCI) | Q4 CY2025 (Dec 2025) | $822.5M | 10.60% | $4.66 adj. EPS | 11.50% |

| Morningstar (MORN) | Q4 CY2025 (Dec 2025) | $641.1M | 8.50% | $2.83 diluted EPS | 4.40% |

| MSCI | Q1 CY2025 (Mar 2025) | $745.8M | 9.70% | $4.00 adj. EPS | 13.60% |

| Morningstar | Q1 CY2025 (Mar 2025) | $581.9M | N/A | N/A | N/A |

Key Observations:

- MSCI leads the peer group on both revenue scale and growth rate, with Q4 2025 organic revenue growth exceeding 10%

- Morningstar is delivering 8.5% revenue growth with particularly strong performance in Morningstar Credit and PitchBook segments

- FactSet’s 6.9% top-line growth trails MSCI but demonstrates steady momentum driven by institutional buy-side and dealmakers clients

- FactSet’s adjusted operating margin of 36.2% remains robust, though margin compression from technology and content investment is a watchpoint across all three peers

How the Market Reacted?

FactSet’s stock responded positively to the Q1 FY2026 results, rising approximately 3% in pre-market trading to around $305 following the earnings release on December 18, 2025. The market appeared encouraged by the dual beat on revenue and EPS, alongside FactSet’s significant expansion of its share repurchase authorization from $400 million to $1 billion.

Over the three months preceding the earnings release, FDS shares had gained 2.8%, outperforming a 10.6% decline in its sector peer group and running ahead of the Zacks S&P 500 composite’s 1.8% gain over the same window. The overall sentiment was bullish, supported by strong free cash flow growth, accelerating AI product adoption with sequential growth exceeding 45%, and reaffirmed full-year guidance.