Introduction

Li Auto Statistics: Li Auto Inc. entered 2025–2026 navigating a complex transition phase, which included decreasing delivery numbers and increasing competition, and its decision to adopt battery electric vehicles (BEVs) as its main product direction.

The company, which once led the Chinese market for extended-range electric vehicles (EREVs), faced severe financial challenges because of market saturation and competition that used aggressive pricing strategies. The company demonstrates its future success through its current funding for research, development, and product creation, and its entry into the new energy vehicle market.

The article will present the Li Auto statistics that shows organization’s structural challenges and transformation opportunities.

Editor’s Choice

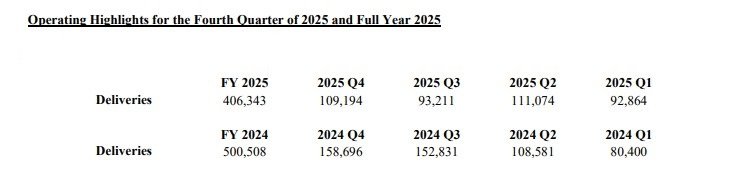

- Li Auto experienced an 18.8% decline in its fiscal year 2025 deliveries, which reached 406343 units compared to 500508 units in 2024.

- The Q4 2025 deliveries experienced a 31.2% decline, which brought the total to 109194 units and showed that demand had decreased significantly.

- The 2025 quarterly delivery numbers showed fluctuations, which produced delivery totals between approximately 92000 units and 111000 units.

- The total revenue decreased by 23.0% compared to the previous year, reaching RMB 112.3 billion because of pricing pressure and decreased sales volumes.

- The vehicle margin decreased from 19.8% to 17.9%, which caused the gross margin to drop to 18.7%.

- The company showed an operational loss of RMB 521 million, which contrasted with the previous year’s profit of RMB 7.0 billion.

- The operating margin decreased from 4.9% to -0.5%.

- The company experienced an 85.8% decrease in net income, which brought the total to RMB 1.14 billion because of earnings pressures.

- The company reported operating cash flow as negative at RMB -8.6 billion.

- The company reported free cash flow of RMB -12.8 billion, which showed the company needed to spend more capital for its operations.

- The company increased its R&D expenses to RMB 11.3 billion, which showed its ongoing commitment to innovation.

- The company achieved a 12.8% decrease in selling and administrative expenses, which brought costs down to RMB 10.7 billion because of its successful budget management.

- The Q1 2026 deliveries reached 95142 units, which exceeded the forecasted delivery range by 6 to 12%.

- The March 2026 delivery total reached 41053 units, while the Li i6 vehicle showed month-over-month growth of approximately 55%.

- Cash reserves of RMB 101.2 billion, which represented more than two times the cash reserves of XPeng.

Li Auto Delivery Performance

(Source: ir.lixiang.com)

- The delivery data from Li Auto demonstrates that the company currently experiences difficulties while going through a period of improvement in its vehicle sales results.

- The total deliveries for FY 2025 amounted to 406,343 units, which represented an 18.8% decrease from the 500,508 units delivered in FY 2024 because the EV market underwent changes that affected year-to-year growth.

- The Q4 2025 delivery figure stands out as the most critical element because it shows a delivery total of 109,194 vehicles, which represents a 31.2% decrease compared to the 158,696 units delivered in Q4 2024.

- The reduction indicates that consumer demand has decreased while competitive pressures have increased, together with possible changes to the product development schedule.

- Q2 2025 reached its highest point with 111,074 units delivered, while Q1 and Q3 delivered steady performance, which showed delivery counts of 92,864 and 93,211 units, respectively. This pattern demonstrated erratic sales progress.

- The 2024 quarterly results demonstrated better growth patterns since Q3 delivered 152,831 units and Q4 produced 158,696 units, which brought about higher comparison results.

- The 2025 decline may stem from economic challenges, together with changing electric vehicle market conditions and mounting price pressures that impact China’s EV market.

- Li Auto begins a consolidation period because its automotive industry performance metrics indicate that the company must achieve delivery growth while it develops its product portfolio and builds its market presence to restore its previous growth path.

Li Auto Financial Performance

(Source: ir.lixiang.com)

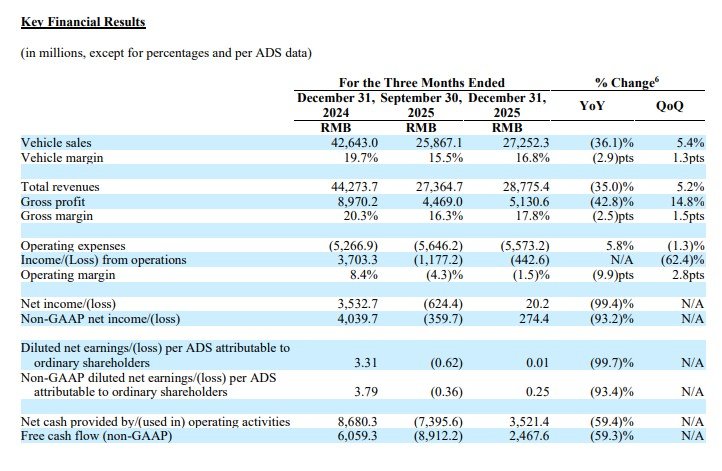

- Li Auto delivered a striking reversal in its latest annual results, reflecting a year defined by demand softening, margin pressure, and cash flow deterioration.

- The company demonstrates a transitional stage through its financial performance and profitability metrics and its current standing in the electric vehicle market.

- The vehicle sales decline resulted in a 23.0% decrease, which brought total revenues down to 112.3 billion RMB.

- The Chinese electric vehicle market shows a decline in delivery operations because of growing competition between companies, which leads to pricing battles and product oversaturation that decreases revenue growth.

- Li Auto’s vehicle margin decreased from 19.8% to 17.9% because its gross margin dropped to 18.7% through a 1.8% decrease.

- The compression results from the company using aggressive discounting techniques while experiencing increased input expenses and operational difficulties that affect their costs and profitability from electric vehicle production.

- The company experienced an operating loss of RMB 521 million after it recorded an operating income of RMB 7.0 billion.

- The operating margin decreased from 4.9% to -0.5% because the company suffered an operating loss.

- Net income plunged 85.8% year-over-year to RMB 1.14 billion, signaling significant pressure on earnings quality.

- The diluted EPS experienced a significant decline, which showed that the company’s earnings quality had worsened.

- The cash flow situation has undergone a major transformation, which currently causes the company its most significant problems.

- The operating cash flow turned negative at RMB -8.6 billion, while free cash flow fell to -12.8 billion, indicating rising capital intensity and potential liquidity strain—critical metrics for assessing financial health in capital-heavy EV businesses.

- The organization achieved a 5.0% decrease in operating expenses, which demonstrated some success in controlling costs.

- The current path of Li Auto shows how the electric vehicle market experiences cyclical downturns. The company needs to regain customer trust through its brand strength and market position by achieving revenue growth, maintaining gross profit margins, and increasing cash flow.

Li Auto 2025–2026 Strategic Highlights

- Li Auto is using its current AI solutions and smart transportation systems to create new business opportunities in international markets.

- The launch of Livis AI Glasses in December 2025, priced at RMB 1,999, marks a bold entry into the AI-powered wearable ecosystem.

- The product weighs 36 grams and uses ZEISS lenses while incorporating proprietary technologies, which include Li Xiang Tong Xue Agent and Livis OS to provide intelligent Q&A and multimedia capture and vehicle connectivity features. This development shows how Li Auto works to create a system that connects all devices and vehicles to improve customer satisfaction and brand loyalty.

- The company shows international growth through its operations in Egypt, Kazakhstan, and Azerbaijan, which helps it reach international customers who want electric vehicles.

- Li Auto establishes a strong competitive advantage through its dedication to safety standards and health performance.

- The Li i8 secured top-tier ratings across all categories in the China Insurance Automotive Safety Index (C-IASI), including a “G” rating, the highest benchmark for crashworthiness.

- The Li i6 achieved the highest NEV score because it performed well in air quality and health protection and energy efficiency assessments.

Li Auto Margin Compression and Cash Flow Growth Transition

- Li Auto’s 2025 financial performance shows a complete profit downturn, which results from decreased vehicle shipments, reduced profit margins, and worsening cash reserves despite the company’s ongoing research and development spending for future business expansion.

- The cost structure analysis indicates that sales costs experienced a major reduction, which reached 20.4 % to RMB91.3 billion (USD 13.1 billion) because of decreased vehicle shipments, which serve as an important market demand indicator and production volume measurement.

- The company achieved better cost management through its expense reduction efforts, which increased its operational efficiency, but its business needs to reach larger operational levels before it can achieve financial success.

- The company spent more on research and development (R&D), which reached RMB11.3 billion, showing that it remains dedicated to developing technology through artificial intelligence and developing electric vehicle platforms, which represent its main business priorities.

- Reduction in selling expenses, together with general expenses and administrative expenses by 12.8%, which reached RMB10.7 billion because of decreased share-based compensation, while the company achieved better cost control and expense management.

- Incurred an operating loss of RMB521 million instead of achieving an operating income which had reached RMB7.0 billion in 2024, while its operating margin dropped to -0.5% from +4.9%.

- The company’s core business operations faced extreme financial difficulties, which caused its operating income to decrease 92.4% to RMB736.6 million, according to non-GAAP accounting standards.

- The company reported non-GAAP net income of RMB2.4 billion, which represented a decline of 77.5%, while basic earnings per ADS decreased from RMB8.06 to RMB1.12, which showed a decline in returns for shareholders and a reduction in earnings quality.

- The company posted an operating cash flow deficit of RMB8.6 billion, which represented a complete contrast to its previous operating cash flow surplus of RMB15.9 billion from 2024 due to decreased cash payments received from customers.

- A free cash flow decline, which reached RMB12.8 billion, because it needed to obtain funding from outside sources and use existing cash reserves to maintain its daily business operations and capital projects.

- Li Auto continues to employ 30728 workers despite facing financial challenges, which helps the company achieve its objectives in intelligent transportation solutions and electric vehicle research and development.

- Li Auto faces a difficult 2025 because of decreasing profit margins and tight cash flow, yet the company can recover through its ongoing commitment to technological advancement and artificial intelligence ecosystem development, and its streamlined operational performance.

Li Auto Q1 2026 Performance

- Li Auto started 2026 with its core business operations running at full capacity after facing a complete supply chain breakdown.

- The company achieved its first-quarter volume target through its March 2026 delivery of 41053 units, which reached a total of 95142 vehicles that exceeded the company’s forecast by 6 to 12%.

- Investors who follow the Li Auto 2026 outlook will find renewed trust after this operational recovery, which demonstrates their ability to execute plans and maintain vital operational functions.

- Li Auto has established itself as a major player in China’s competitive new energy vehicle market through its total delivery of 1.63 million units, which demonstrates its ability to produce electric vehicles at a premium level.

- The Li i6 sales performance serves as the primary engine for growth because it has become the main product of the company.

- March monthly deliveries reached 24000 units, which showed a 55% increase from the February total of 16000 units. This increase demonstrates that customers have started to purchase products after supply demands were met.

- The implementation of a dual-supplier system with CATL and Sunwoda has solved battery supply issues, which resulted in a major operational transformation.

- The new system, which enables quick product changes, has decreased delivery times to between 2 and 6 weeks, while Li Auto used this advantage to eliminate order backlogs.

- The company produced more than 80000 Li i6 units by March 2026, which shows their success in manufacturing expansion since their launch in August 2025.

- Li Auto has established a strong infrastructure foundation by building 517 retail stores and 552 service centers, together with more than 4000 supercharging stations, which have 22400 charging stalls. This system development decreases range anxiety while improving customer service, which serves as a critical factor in the electric vehicle adoption process.

- The MindVLA autonomous driving model and 3D Vision Transformer (ViT) Encoder, which NVIDIA GTC 2026 introduced, show that current research efforts are beginning to develop AI-based transportation systems and software-controlled automobiles, which will enhance the company’s business success.

- Li Auto can achieve 400000 yearly shipments in 2026 because they now have monthly sales rates that exceed 40000 units, and they will maintain their current product supply and market demand.

Cash Reserve and Liquidity Analysis

- Li Auto enters 2026 with a formidable liquidity advantage, which positions the company as one of the most financially resilient players in China’s new energy vehicle NEV market.

- Li Auto controls a cash reserve that exceeds 1012 billion RMB because the company holds cash and cash equivalents and short-term investments, which total that amount.

- The substantial cash buffer that the company maintains will enable operations for multiple years, even as free cash flow remains negative, which establishes liquidity as a vital element of Li Auto’s 2026 business forecast.

- Nio’s operating cash outflow reached RMB 15.9 billion during Q1 2025, which indicates that the company follows an aggressive cash burn path that extends back to 2016 because Nio has accumulated more than RMB 80 billion in losses through 2024.

- Li Auto maintains a stronger financial position, which includes a better balance sheet and capital structure, because the company operates in a period of high capital expenditures while it still needs to develop its business operations.

- The XPeng company shows financial improvement through its positive free cash flow, which will reach approximately RMB 5 billion in 2025 despite its limited cash reserves.

- XPeng generates cash through its operations, while Li Auto and Nio continue their projects, which require substantial funding and produce net financial losses.

- For Li Auto, the RMB 101.2 billion liquidity reserve effectively acts as a strategic “option value”, enabling aggressive investments in battery electric vehicles (BEVs), AI-driven mobility, autonomous driving platforms, and charging infrastructure.

- The company can use its flexible operating model to improve its supplier negotiations and maintain its pricing strategies while developing innovative products for its electric vehicle business.

- The combination of promotional incentives and margin pressures in a competitive market will lead to increased capital expenditures.

- Li Auto can sustain its operations for several years with its current financial reserves, but the company needs to establish stable profit margins and increase its revenue to maintain this advantage over time.

Conclusion

Li Auto Statistics: The 2025 performance of Li Auto demonstrates difficulties in its operational transition because the company experienced decreasing delivery volumes and reduced income, and diminishing profit margins while competing in the Chinese electric vehicle market. Current operational results show negative impacts from the company’s dedication to BEVs and its ongoing efforts in research, development, and artificial intelligence-based transportation technologies.

The first quarter of 2026 shows signs of recovery, which developed through strong delivery performance and better supply chain operations, because the company shows operational strength. Li Auto uses its large cash reserves of RMB 101.2 billion to handle unpredictable market conditions while the company continues to develop new products and pursue opportunities for future business expansion in the new energy vehicle market.

FAQ

Li Auto delivered 406,343 vehicles in 202,5 which represented an 18.8% decrease from the previous year.

Revenue fell 23% because of decreased deliveries and pricing pressure, and the highly competitive conditions in the electric vehicle market.

The company experienced an operating loss of RMB 521 million and a significant decrease in net income, which resulted in its unprofitable operation.

The company maintained RMB 101.2 billion in cash, which created substantial liquidity even though it experienced negative cash flow.

The company achieved Q1 2026 deliveries of 95,142 units, which exceeded market expectations and demonstrated its recovery progress.