Fast Retailing’s FY2026 first‑half run‑rate, led by a record FY2026 Q1, shows consolidated revenue above ¥1.0 trillion with double‑digit profit growth, supported by strong UNIQLO Japan and UNIQLO International performance. EPS is not disclosed in the summary; revenue beat internal plans, and the stock reaction is characterized in media as positive, with sentiment reflecting an earnings beat versus expectations and a higher full‑year outlook. After‑hours movement is not explicitly disclosed in the available texts.

About FAST RETAILING CO., LTD.

Fast Retailing Co., Ltd. is a global apparel retailer best known for the UNIQLO and GU brands and is listed on the Tokyo Stock Exchange under ticker 9983. As of early April 2026, the company’s market capitalization is around ¥20 trillion, placing it among Japan’s largest consumer companies. The group is headquartered in Yamaguchi Prefecture, Japan, and operates a network of UNIQLO and other brand stores across Japan, Greater China, South Korea, Southeast Asia, Europe, and North America.

Founded in 1963 (through its predecessor operations) and developed into its current form over subsequent decades, Fast Retailing focuses on functional, affordable clothing, marketed as LifeWear, with an integrated model encompassing product planning, manufacturing, and retail.

The stock currently trades at a P/E ratio in the low‑40s on normalized earnings, reflecting high growth expectations, while its dividend yield is below 1% on a trailing basis. Fast Retailing continues to emphasize capital efficiency and shareholder returns, with FY2026 guidance indicating a planned annual dividend of ¥540 per share, split equally between interim and year‑end payments, representing a year‑on‑year increase.

Top Financial Highlights

- Consolidated revenue for FY2026 Q1 reached ¥1.0277 trillion (up 14.8% year on year), marking Fast Retailing’s first ever trillion‑yen quarter.

- Business profit rose to ¥205.6 billion, an increase of 31.0% year on year, reflecting stronger margins and operational leverage.

- Profit attributable to owners of the Parent reached ¥147.4 billion, up 11.7% year on year.

- Operating profit for the quarter was reported at approximately ¥210.9 billion, up about 33.9% from the prior‑year period, according to external coverage.

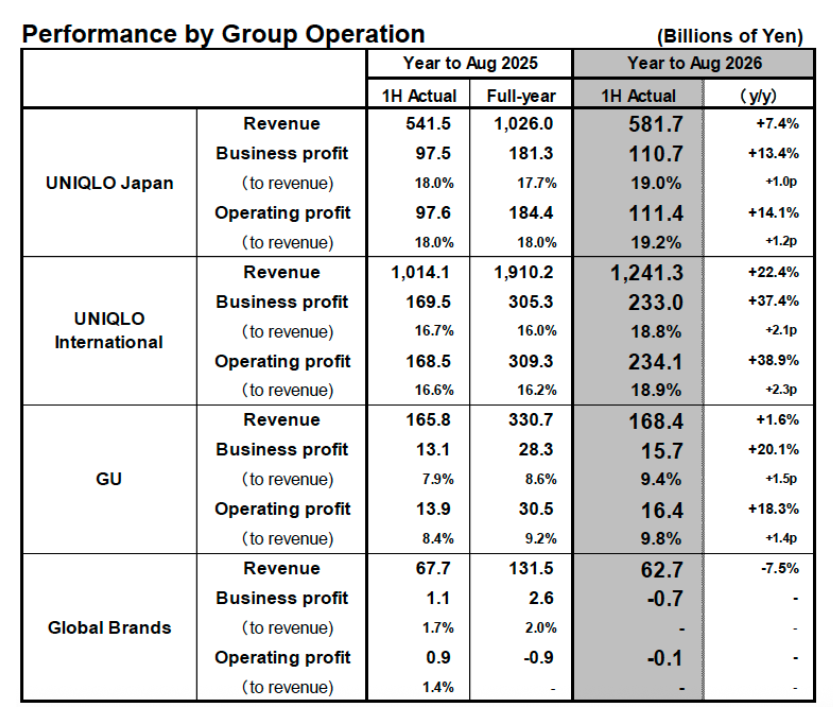

- At the segment level, UNIQLO Japan posted revenue of ¥299.0 billion (up 12.2%) and business profit of ¥62.4 billion (up 20.2%), driven by strong Fall and Winter product sales and improved SG&A ratios.

- UNIQLO International delivered revenue of ¥603.8 billion (up 20.3%) and business profit of ¥117.3 billion (up 38.0%), as store expansion and brand recognition lifted profitability and the business profit margin improved by 2.4 points.

- The GU segment recorded revenue of ¥91.3 billion (up 0.8%) and business profit of ¥11.4 billion (up 20.0%), with margin gains supported by better inventory planning and discount control.

- Global Brands revenue declined to ¥33.0 billion (down 7.6%) with business profit contracting to ¥1.7 billion (down 14.8%), reflecting weaker Theory USA performance and ongoing restructuring at Comptoir des Cotonniers and Princesse tam.tam.

- The Q1 gross profit margin at group level is reported around the mid‑50% range, with the summary citing margin contraction of 0.5 points in UNIQLO Japan and a 2.4‑point margin improvement in UNIQLO International.

- Fast Retailing revised its FY2026 consolidated guidance upward, now targeting revenue of ¥3.8000 trillion (up 11.7% year on year) and business and operating profit of ¥650.0 billion (up 17.9% and 15.2%, respectively).

- Full‑year profit attributable to owners of the Parent is now forecast at ¥450.0 billion, up 3.9% year on year, along with an annual dividend forecast of ¥540 per share, increased by ¥40 versus FY2025.

- Management highlights particularly strong growth in Greater China, South Korea, Southeast Asia/India/Australia, Europe, and North America, all delivering double‑digit revenue and profit increases within UNIQLO International.

- While GU’s revenue growth was modest and same‑store sales slightly negative, the segment’s improved gross margin, aided by narrower assortment and focused inventory on winning products, drove a large increase in profit.

- Global Brands is expected to contribute only modestly near term, but restructuring measures and cost‑structure improvements are beginning to reduce losses in the Comptoir des Cotonniers and Princesse tam.tam businesses.

Beat or Miss?

Fast Retailing’s FY2026 Q1 results meaningfully exceeded market expectations on profit, and the company raised its full‑year operating profit forecast, signaling management confidence in sustained growth. Consensus estimates are not disclosed in the company release, but external sources report that operating profit beat LSEG’s consensus by a wide margin. The table below summarizes reported headline figures against available reference points.

| Metric | Reported (FY2026 Q1) | Difference or analysis |

| Revenue | ¥1.0277 trillion | Above prior‑year ¥895.2 billion, representing +14.8% year on year; record level. |

| Operating profit | ≈¥210.9 billion | Up 33.9% vs prior year and well above LSEG consensus of about ¥177 billion. |

| Business profit | ¥205.6 billion | Surged 31.0% year on year, benefiting from stronger margins and scale. |

| Profit attributable to owners | ¥147.4 billion | Rose 11.7% year on year; consensus comparison not disclosed (treated as N/A). |

| EPS | N/A in summary | Not provided in the available summary; analyst EPS consensus not cited (N/A). |

| FY2026 revenue guidance | ¥3.8000 trillion | Raised by ¥50.0 billion versus initial guidance, implying continued top‑line strength. |

| FY2026 operating profit guidance | ¥650.0 billion | Increased by ¥40.0 billion, reflecting confidence after Q1 beat. |

What leadership is saying?

“UNIQLO business in all regions performed strongly, reporting revenue and profit gains across the board. High‑quality store openings and strategic information dissemination contributed considerably to our branding, while better organization of inter‑season business enabled Fall products and year‑round products to drive sales throughout the quarter.”

Chief Financial Officer Takeshi Okazaki said, “In the first quarter, we managed to absorb the additional tariffs imposed in the U.S. and exceeded our projections for business profit margins, supporting our decision to raise the full‑year operating profit forecast to ¥650 billion.”

Historical Performance

For the FY2026 first‑half run‑rate, the best available comparison is between FY2026 Q1 and the same quarter in FY2025. Consolidated first‑half FY2025 data are also available, indicating the trajectory of revenue and profit into FY2026. Operating expenses are approximated using operating profit where necessary, as detailed in the table.

Fast Retailing Q1 year‑on‑year comparison

| Category | Q1 FY2026 | Q1 FY2025 (approx.) | Change (%) |

| Revenue | ¥1.0277 trillion | ≈¥0.8952 trillion | About +14.8%, as reported. |

| Profit attributable to owners | ¥147.4 billion | ≈¥132.0–140.3 billion | Reported +11.7% YoY vs prior‑year figure. |

| Operating profit | ≈¥210.9 billion | ≈¥157.6 billion | Around +33.9% YoY, reflecting strong margin gains. |

FY2025 first‑half baseline

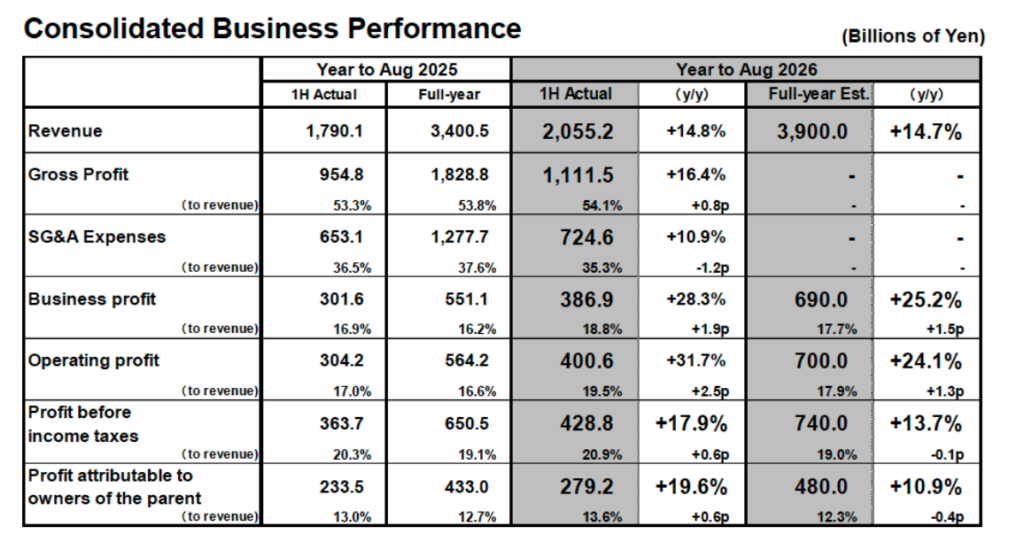

Fast Retailing reported 1H FY2025 revenue of ¥1.7901 trillion, with operating profit of ¥304.2 billion and profit attributable to owners of ¥233.5 billion, representing double‑digit growth at that time. While FY2026 1H results are not yet disclosed, current Q1 performance and upgraded guidance imply the company is tracking ahead of this baseline in both revenue and profitability on a full‑year view.

Key Competitors (YoY)

To contextualize Fast Retailing’s performance, the table below compares its most recently reported full‑year results to those of a major global apparel competitor, Inditex (owner of Zara), on a year‑on‑year basis. This illustrates how Fast Retailing’s growth profile fits within the broader fast‑fashion and specialty apparel landscape

| Category | Fast Retailing FY2025 | Fast Retailing FY2024 (approx.) | Change (%) | Inditex FY2025 | Inditex FY2024 | Change (%) |

| Revenue | ¥3.4005 trillion | ≈¥3.103 trillion | About +9.6% YoY. | €39.9 billion | €38.6 billion | +3.2% YoY. |

| Net income | ¥433.0 billion | ≈¥372.0 billion | +16.4% YoY. | €6.2 billion | €5.8 billion | +6.0% YoY. |

| Operating expenses (proxy) | Implied from operating profit of ¥564.2 billion | Prior‑year implied ≈¥501.0 billion | Improved margin with operating profit up 12.6%. | Not fully disclosed in summary | Not fully disclosed | N/A in brief summary. |

How the market reacted?

Following the FY2026 Q1 results announcement on 8 January 2026, external reports indicate that Fast Retailing’s shares traded positively as investors responded to the earnings beat and higher full‑year guidance. Reuters notes that operating profit significantly exceeded LSEG consensus, which typically supports a favorable near‑term share price reaction.

As of early April 2026, the stock trades around the mid‑¥60,000 range, implying the market continues to price in robust growth with a premium valuation multiple. Overall sentiment appears bullish, with investors focusing on strong UNIQLO International momentum and upgraded FY2026 forecasts, while remaining attentive to currency effects and the slower GU and Global Brands segments.