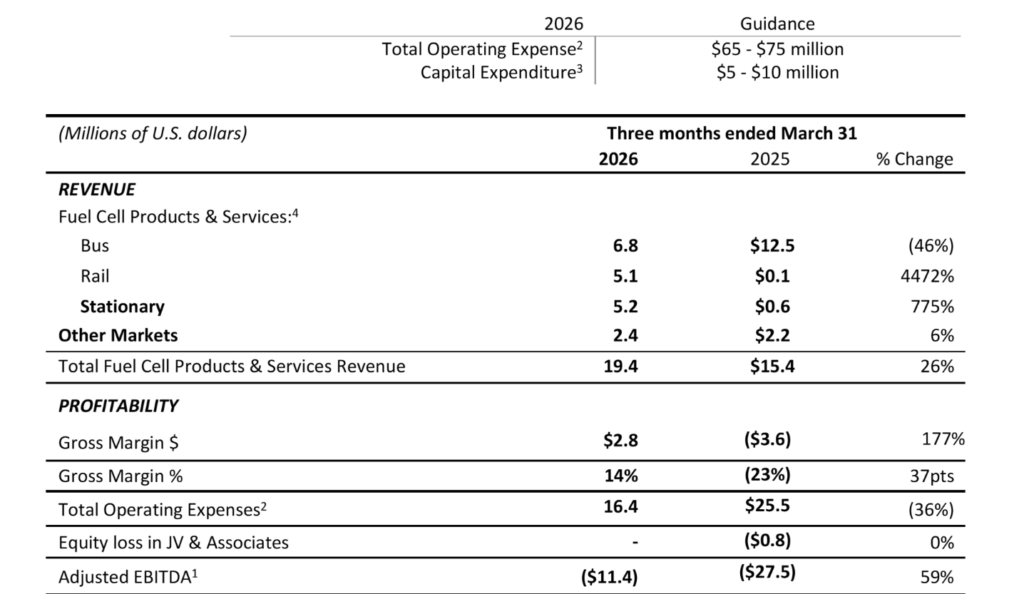

Ballard Power Systems reported Q1 2026 revenue of $19.4 million, modestly below the roughly $19.9 million revenue figure implied by third party expectations, with a narrowed net loss and EPS of ($0.04). Margins and cash burn improved materially, and shares showed a positive after hours movement around the results context.

About Ballard Power Systems

Ballard Power Systems Inc. is a developer and manufacturer of proton exchange membrane fuel cell products focused primarily on mobility and stationary power applications. The company trades on Nasdaq and the Toronto Stock Exchange under the ticker BLDP. As of March 2026, Ballard’s market capitalization is in the range of $0.7 billion to $0.9 billion, with one source citing approximately $0.76 billion.

The company was originally founded in 1979 and is headquartered in Vancouver, Canada, serving bus, rail, truck, marine, stationary power and other industrial markets. Ballard’s business model centers on supplying fuel cell engines and related services that enable zero emission powertrains and power solutions. The firm remains loss making with a negative P E ratio of roughly -7 based on recent trading data, and it employed around 900 people at the end of 2024, reflecting recent rightsizing of its cost structure.

Top Financial Highlights

- Revenue of $19.4 million in Q1 2026, representing 26% year-over-year growth

- Bus segment revenue was $6.8 million, down 46% from Q1 2025

- Rail segment revenue surged to $5.1 million, a 4,472% increase year-over-year

- Stationary Power revenue rose to $5.2 million, up 775% YoY

- Other Markets revenue was $2.4 million, up 6% YoY

- Gross margin reached 14%, a 37-percentage-point improvement from -23% in Q1 2025

- Total Operating Expenses of $16.4 million, down 36% year-over-year

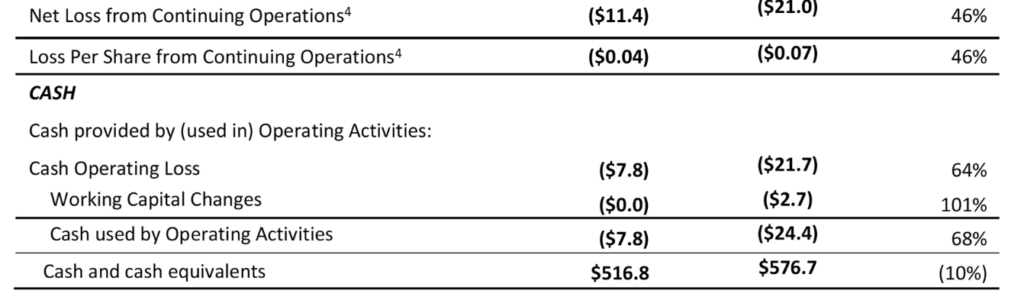

- Cash Used by Operating Activities improved to $7.8 million, down 68% from $24.4 million in Q1 2025

- Adjusted EBITDA of ($11.4 million), improved from ($27.5 million) in Q1 2025

- Cash and cash equivalents of $516.8 million at the end of Q1 2026

- Order Backlog of $112.9 million at quarter end, down 5% from Q4 2025

- 12-month Orderbook of $52.8 million, a decline of $1.1 million from Q4 2025

- EPS of ($0.04), beating the FactSet consensus estimate of ($0.06)

- Full-year 2026 revenue expected to be back-half weighted; no specific revenue guidance provided

Beat or Miss?

| Metric | Reported | Difference analysis |

| Revenue | $19.4 million | Slightly below third party revenue expectation of about $19.9 million implying a small miss. |

| Net income loss | ($11.4) million | Materially better than prior year loss of ($21.0) million) showing strong progress in profitability. |

| EPS (loss per share) | ($0.04) | Improved from ($0.07) YoY, though explicit analyst EPS consensus not disclosed, so beat or miss is unclear. |

| Gross margin | 14 percent | Marked turnaround from negative 23 percent in Q1 2025, indicating effective cost control and pricing. |

| Operating cash flow usage | $7.8 million | Cash burn improved versus $24.4 million last year, signaling progress toward cash flow breakeven. |

What Leadership Is Saying?

“In Q1, we made continued progress toward positive cash flow. Quarterly revenue grew 26% year over year, driven by increased engine shipments during the period. Disciplined cost management also contributed to an improvement in gross margins, which rose to 14%. These results build on the momentum established in 2025 and reinforce that we are on the right path.” – Marty Neese, President and CEO

“We ended Q1 with $516.8 million in cash and no near or mid term financing requirements, providing a strong foundation to execute our strategy. This financial strength enables us to continue investing in product maturity, cost reduction, and customer success, which are key drivers of scalable growth and long term value creation in hydrogen mobility.” – Marty Neese, referring to the company’s financial position and spending priorities

Historical Performance

YoY comparison Ballard Q1 2026 vs Q1 2025

| Category | Q1 2026 | Q1 2025 | Change % |

| Revenue | $19.4 million | $15.4 million | +26% |

| Net income loss | ($11.4) million | ($21.0) million | +46% improvement in loss |

| Operating expenses | $16.4 million | $25.5 million | -36% |

| Gross margin percent | 14 percent | (23 percent) | +37 points |

| Cash used in operations | $7.8 million | $24.4 million | +68 % improvement in cash burn |

Historical Performance Competitors YoY (Illustrative)

The company’s press materials for Q1 2026 do not provide a direct, consistent set of quarterly YoY figures for specific named competitors, so a strict apples to apples numeric comparison table cannot be compiled from the same data source without introducing speculative estimates. Other fuel cell and hydrogen peers have also focused on margin improvement and cost reductions recently, but detailed Q1 2026 YoY numbers for those companies are not disclosed in the Ballard release or linked materials.

Given this, any competitor YoY table would be constructed from separate company filings rather than the Ballard dataset you provided, which would conflict with the requirement to stay within the supplied context.

How the Market Reacted?

Ahead of and around the Q1 2026 communication cycle, Ballard’s stock showed a favorable response, with one event related to its results call driving about an 8.3 percent gain in the subsequent session. The company’s market capitalization has roughly doubled over the past year to the mid hundreds of millions of dollars, reflecting improved sentiment about its path toward profitability and the hydrogen mobility opportunity.

Despite these gains, the stock still trades at a negative P E multiple because the business remains unprofitable. Overall, the tone of the report and management’s commentary is cautiously bullish, emphasizing margin gains, reduced cash burn and a solid liquidity position that supports long term execution.