HUYA Inc. reported Q1 2026 revenue of $250.6 million (RMB 1.73 billion), up 14.6% year-over-year, driven by explosive 69.4% growth in game-related services and advertising revenue to $91.0 million, though the company posted a net loss of $0.6 million compared to net income of $0.9 million in Q1 2025. The company’s non-GAAP net income was $3.1 million, down from $3.5 million in the prior-year quarter.

About HUYA Inc.

HUYA Inc. (NYSE: HUYA) is a leading game-related entertainment and services provider headquartered in Guangzhou, China, founded in 2016 as an independent entity. The company operates with a market capitalization of approximately $674.68 million and employs 1,251 people.

HUYA delivers dynamic live streaming and video content through platforms including Huya Live in China and Nimo TV internationally, while also providing game-related services such as game distribution, in-game item sales, and advertising. The company trades at a P/E ratio of 31.15 with a price-to-sales ratio of 0.84, and is a subsidiary of Tencent, which holds 67% equity stake and 95% voting power.

Top Financial Highlights

- Total Net Revenues reached RMB 1,728.4 million ($250.6 million), up 14.6% year-over-year from RMB 1,508.6 million in Q1 2025

- Live Streaming Revenues declined to RMB 1,101.0 million ($159.6 million) from RMB 1,138.2 million, reflecting challenging industry conditions

- Game-Related Services, Advertising and Other Revenues surged 69.4% to RMB 627.4 million ($91.0 million) from RMB 370.4 million, representing 36.3% of total revenues

- Gross Profit increased 34.3% to RMB 253.2 million ($36.7 million) from RMB 188.5 million in Q1 2025

- Gross Margin expanded to 14.6% from 12.5% in the prior-year quarter, driven by higher-margin revenue mix

- Operating Loss narrowed to RMB 28.8 million ($4.2 million) from RMB 59.6 million in Q1 2025

- Non-GAAP Operating Loss improved to RMB 2.7 million ($0.4 million) from RMB 35.6 million year-over-year

- Net Loss Attributable to HUYA was RMB 4.1 million ($0.6 million) versus net income of RMB 0.9 million in Q1 2025

- Non-GAAP Net Income totaled RMB 21.1 million ($3.1 million), down from RMB 24.0 million in the prior-year period

- EPS (Non-GAAP) was RMB 0.09 ($0.01) per ADS, compared to RMB 0.10 in Q1 2025

- Cost of Revenues increased 11.8% to RMB 1,475.2 million ($213.9 million) from RMB 1,320.1 million

- Sales and Marketing Expenses jumped 45.1% to RMB 88.1 million ($12.8 million) due to Goose Goose Duck mobile launch promotions

- Research and Development Expenses rose 1.7% to RMB 131.7 million ($19.1 million) from RMB 129.5 million

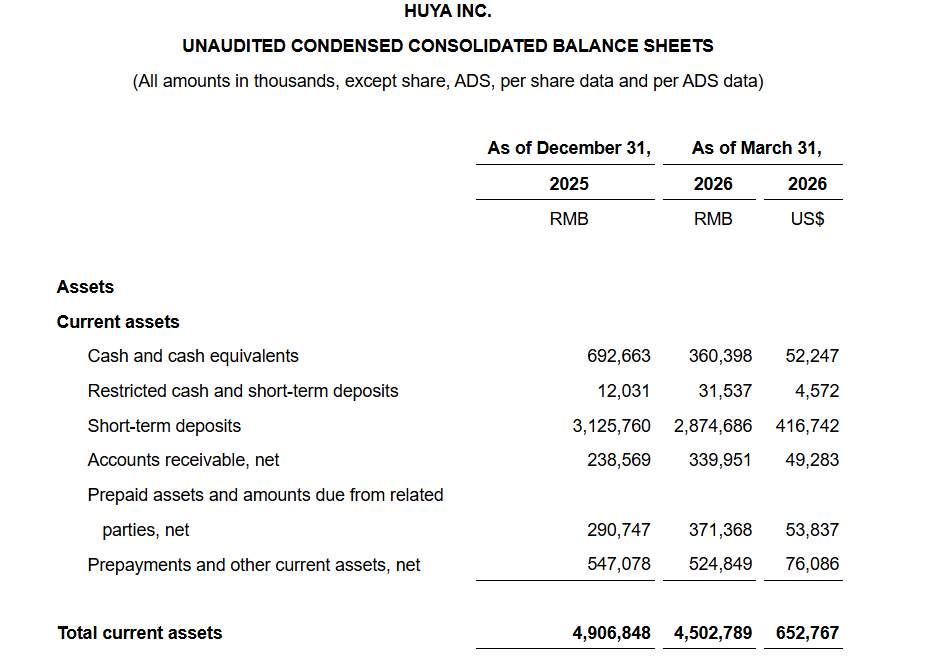

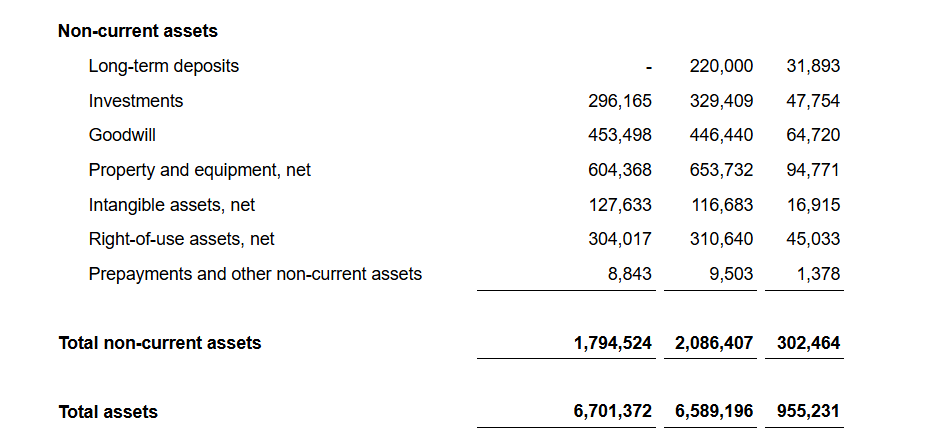

- Cash, Cash Equivalents, and Deposits stood at RMB 3,455.1 million ($500.9 million) as of March 31, 2026, down from RMB 3,818.4 million at year-end 2025

- Interest Income declined to RMB 30.3 million ($4.4 million) from RMB 64.9 million, reflecting lower time deposit balances after special dividend payments

Beat or Miss?

| Metric | Reported | Difference/Analysis |

| Total Net Revenues | RMB 1,728.4M ($250.6M) | Analyst estimates not disclosed in earnings release |

| EPS (Non-GAAP) per ADS | RMB 0.09 ($0.01) | Consensus estimates not provided; Q4 2025 estimate was $0.02 but actual was -$0.01 |

| Game-Related Services Revenue | RMB 627.4M ($91.0M) | Exceeded internal expectations with record 36.3% of total revenue mix |

| Operating Loss | RMB 28.8M ($4.2M) | Improved 51.7% vs Q1 2025 loss of RMB 59.6M |

What Leadership Is Saying?

“Huya continued to deliver solid results in the first quarter of 2026, underpinned by our ongoing transformation into a comprehensive game-related services provider. Total net revenues reached RMB1.73 billion, up 14.6% year-over-year, while game-related services, advertising, and other revenues grew 69.4% year-over-year to RMB627.4 million, representing a record 36.3% of total net revenues. Goose Goose Duck mobile continued to gain traction in the Chinese mainland, reaching as high as Top 5 on the local Apple App Store top-grossing games chart in April, demonstrating the game’s promising monetization potential.” – Mr. Junhong Huang, Acting Chief Executive Officer

“This quarter’s steady top line growth and the continued improvement in both our revenue mix and operating performance underscore the earnings potential of our diversification efforts. The increased revenue contribution from businesses with higher gross margins led to a year-over-year and sequential gross margin expansion to 14.6% this quarter. Looking ahead, we remain focused on prudently pursuing growth opportunities while preserving earnings quality and delivering long-term value to our shareholders.” – Mr. Raymond Peng Lei, Chief Financial Officer

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue | RMB 1,728.4M ($250.6M) | RMB 1,508.6M | 14.60% |

| Live Streaming Revenue | RMB 1,101.0M ($159.6M) | RMB 1,138.2M | -3.30% |

| Game Services Revenue | RMB 627.4M ($91.0M) | RMB 370.4M | 69.40% |

| Gross Profit | RMB 253.2M ($36.7M) | RMB 188.5M | 34.30% |

| Gross Margin | 14.60% | 12.50% | +2.1 pp |

| Operating Loss | RMB 28.8M ($4.2M) | RMB 59.6M | -51.70% |

| Net Income (Loss) | RMB -4.1M ($-0.6M) | RMB 0.9M | N/A |

| Non-GAAP Net Income | RMB 21.1M ($3.1M) | RMB 24.0M | -12.10% |

Competitor Performance Comparison

| Category | DouYu Q1 2026 | Bilibili Q1 2026 | HUYA Q1 2026 | Analysis |

| Revenue | Data not yet released | RMB 7.0B (approx) | RMB 1,728.4M ($250.6M) | Bilibili operates at significantly larger scale in broader entertainment streaming |

| Net Income | Not available | Positive earnings of RMB 0.85 EPS | RMB -4.1M loss (RMB 21.1M non-GAAP) | HUYA’s profitability challenged by transformation costs |

| Operating Focus | Game-centric live streaming | Broader entertainment and gaming content | Game services transformation | HUYA diversifying beyond pure live streaming into game publishing and services |

Market Reaction

The earnings announcement was released on May 12, 2026, before U.S. market open, with management hosting a webinar at 6:00 a.m. ET to discuss results. Specific stock price movement following the release was not disclosed in the earnings report. The company’s strategic shift toward higher-margin game-related services demonstrated progress with 69.4% revenue growth in this segment, though the overall net loss of $0.6 million compared to prior-year net income suggests the transformation remains in progress. The 51.7% improvement in operating loss and gross margin expansion to 14.6% from 12.5% signal positive operational momentum despite live streaming revenue headwinds.