Adidas delivered a record-breaking fiscal year 2025 with revenues of EUR 24.8 billion, up 13% currency-neutral for the adidas brand. EPS surged 76% to EUR 7.46 from continuing operations. Operating profit jumped 54% to EUR 2.056 billion. However, shares fell roughly 7-8% after the company issued a 2026 operating profit outlook of EUR 2.3 billion, missing the Visible Alpha consensus of EUR 2.72 billion.

About Adidas AG

Adidas AG (Ticker: ADS on Frankfurt/Xetra; ADDYY OTC in the U.S.) is the largest sportswear manufacturer in Europe and the second-largest globally, behind Nike. Founded on August 18, 1949, by Adolf “Adi” Dassler in Herzogenaurach, Bavaria, Germany, the company designs and manufactures footwear, apparel, and accessories across Performance and Lifestyle categories. Its headquarters, called “World of Sports,” remains in Herzogenaurach.

As of early March 2026, adidas carries a market capitalization of approximately EUR 25.2 billion on the Frankfurt exchange (around $29.3 billion for the OTC-traded ADRs). The trailing P/E ratio stands at 18.84 with a forward P/E of 14.86. Return on equity is 22.96%, and the company employs roughly 64,000 people across 180 nationalities, as noted by CEO Bjorn Gulden during the FY 2025 earnings call. The proposed dividend yield for 2026 is approximately 2.76%.

Top Financial Highlights

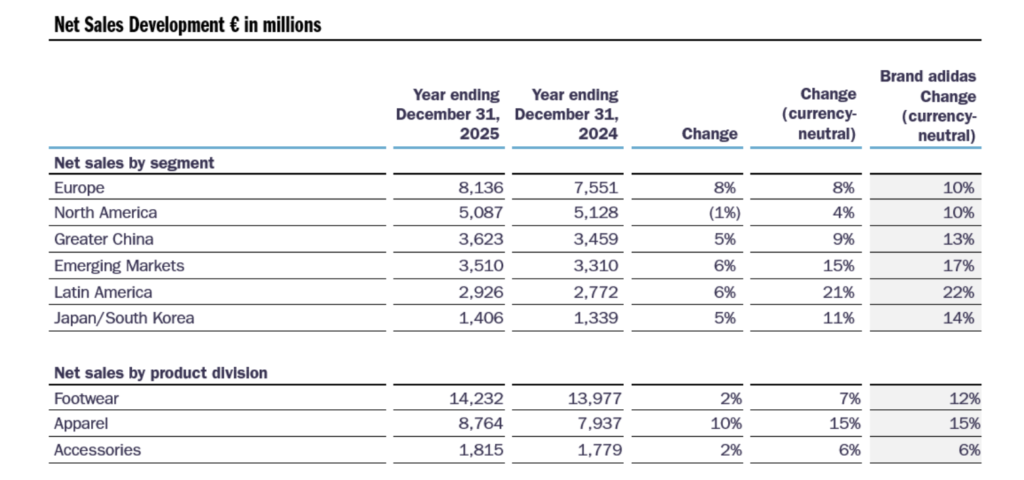

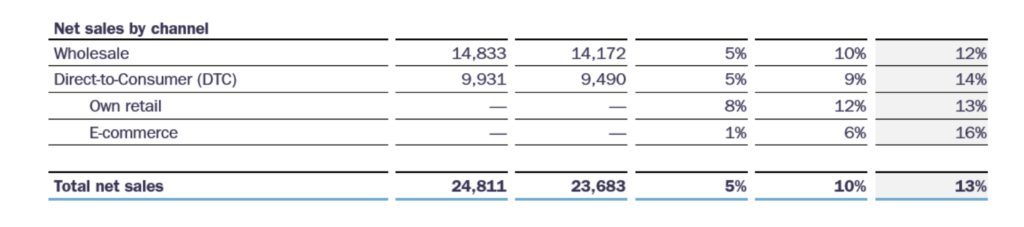

- Total revenue reached a record EUR 24,811 million, up 5% reported and 13% currency-neutral for the adidas brand

- Gross profit grew 6% to EUR 12,804 million, with gross margin improving 0.8% points to 51.6%

- Operating profit surged 54% to EUR 2,056 million, lifting the operating margin 2.6 percentage points to 8.3%

- Net income from continuing operations increased 67% to EUR 1,377 million

- Basic and diluted EPS from continuing operations climbed 76% to EUR 7.46 (2024: EUR 4.24)

- Double-digit currency-neutral growth across all markets: Europe (+10%), North America (+10%), Greater China (+13%), Latin America (+22%), Emerging Markets (+17%), Japan/South Korea (+14%)

- Footwear revenue for the adidas brand grew 12% c.n., apparel grew 15%, accessories grew 6%

- Other operating expenses declined 1% to EUR 10,871 million; operating overhead expenses fell 4% to EUR 7,792 million

- Marketing and point-of-sale expenses increased 8% to EUR 3,079 million (12.4% of sales)

- Cash on hand / Net borrowings: Adjusted net borrowings stood at EUR 4,331 million with leverage at 1.4x EBITDA

- Capital expenditure of EUR 477 million, down from EUR 540 million in 2024

- Inventories rose 17% to EUR 5,832 million, reflecting planned top-line growth and early FIFA World Cup 2026 purchases

- Proposed dividend of EUR 2.80 per share, a 40% increase, plus a share buyback of up to EUR 1 billion in 2026

- 2026 guidance: Currency-neutral revenue growth at a high-single-digit rate (adding ~EUR 2 billion), operating profit to reach ~EUR 2.3 billion despite ~EUR 400 million in tariff and FX headwinds

Beat or Miss?

| Metric | Reported | Analyst Estimate / Consensus | Difference |

| FY 2025 Revenue | EUR 24,811M | ~EUR 25,700M (26-analyst consensus) | Missed by ~EUR 889M (partly due to EUR 1B FX drag) |

| FY 2025 EPS (continuing ops) | EUR 7.46 | ~EUR 7.51 (consensus) | Slight miss of EUR 0.05 |

| Q4 2025 EPS (OTC-reported) | $0.24 | $0.26 (expected) | Missed by ~$0.017 |

| FY 2025 Operating Profit | EUR 2,056M | ~EUR 2,000M (company’s own raised guidance) | Beat own guidance by EUR 56M |

| FY 2026 Operating Profit Outlook | ~EUR 2,300M | EUR 2,720M (Visible Alpha consensus) | Missed consensus by ~EUR 420M |

What Leadership Is Saying?

CEO Bjorn Gulden:

“I am again very proud of what our people have achieved. Driving double-digit growth in the fourth quarter despite all the external turbulence, and more than doubling our operating profit in the quarter made the year end very well and made 2025 much better than we had planned and expected when the year started.

The double-digit growth in all markets and all channels is of course very pleasing, but even more important is that this is quality growth. Our markets have been very good at managing that the right product in the right amount has been sold in their markets and that we have managed to keep full-price sell-throughs high and discounts under control. The gross margin of 51.6% (without Yeezy) is historically high and underlines this performance and the strength of our brand.”

CFO Harm Ohlmeyer:

“The most important one is the 13% currency-neutral growth for the adidas brand. The total company grew currency-neutral, including the YEEZY impact, 10% and reported 5%. So there is a 5% point difference between currency-neutral and reported. That is around EUR 1 billion. We are translating the 54% growth in operating profit to a 67% net income growth. We have remained very disciplined on pricing and discounting. There has been tremendous leverage on the operating overheads, coming from 34.2% to 31.4%, so 280 basis points improvement.”

Historical Performance

FY 2025 vs FY 2024

| Category | FY 2025 | FY 2024 | Change (%) |

| Net Sales | EUR 24,811M | EUR 23,683M | 4.80% |

| Gross Profit | EUR 12,804M | EUR 12,026M | 6.50% |

| Gross Margin | 51.6% | 50.80% | +0.8pp |

| Operating Profit (EBIT) | EUR 2,056M | EUR 1,337M | 53.80% |

| Operating Margin | 8.3% | 5.60% | +2.6pp |

| Net Income (continuing ops) | EUR 1,377M | EUR 824M | 67.10% |

| EPS (basic/diluted) | EUR 7.46 | EUR 4.24 | 76.00% |

| Other Operating Expenses | EUR 10,871M | EUR 10,945M | -0.70% |

| Marketing & POS Expenses | EUR 3,079M | EUR 2,841M | 8.40% |

| Operating Overhead Expenses | EUR 7,792M | EUR 8,103M | -3.80% |

| Tax Rate | 24.3% | 26.50% | -2.2pp |

Competitor Performance

| Category | adidas (FY 2025) | Nike (FY 2025, ending May 2025) | Puma (FY 2025) |

| Revenue | EUR 24,811M (+5% reported) | $46,309M / ~EUR 42,760M (-9.8%) | EUR 7,296M (-13.1% reported) |

| Net Income | EUR 1,377M (+67%) | $3,219M / ~EUR 2,972M (-43.5%) | EUR -645.5M (vs +EUR 281.6M in 2024) |

| Gross Margin | 51.6% (+0.8pp) | 42.7% (-1.9pp) | 45.0% (-2.6pp) |

| Operating Margin | 8.3% (+2.6pp) | ~8.0% (-3.8pp) | -4.9% (reported, vs +6.5%) |

| Revenue Trend | Record high, 13% c.n. brand growth | 10% decline, inventory liquidation | 8.1% c.a. decline, strategic reset |

adidas clearly outperformed both Nike and Puma in FY 2025. Nike reported a 9.8% revenue decline and a 43.5% net income drop as it underwent its “Win Now” turnaround amid excess inventory and weaker digital demand. Puma posted an even steeper decline, with a 13.1% reported sales decrease and a net loss of EUR 645.5 million, driven by its strategic reset initiative that involved scaling back undesirable wholesale operations and clearing excess channel inventory.

How the Market Reacted?

Despite the strong FY 2025 results, adidas shares tumbled approximately 7-8% on March 4, 2026, the day of the earnings release. The sell-off was not a reaction to the backward-looking 2025 numbers but rather to the forward-looking 2026 profit guidance. The operating profit outlook of approximately EUR 2.3 billion fell short of the Visible Alpha consensus estimate of EUR 2.72 billion, with management pointing to roughly EUR 400 million in combined headwinds from higher U.S. tariffs and unfavorable currency movements.

CNBC reported that shares fell as much as 8%, while analysts at RBC Capital Markets noted the guidance “implies a 15% consensus earnings downgrade at face value”. However, some analysts viewed the sell-off as overdone, noting that adidas’ mid-term outlook guiding for high-single-digit topline growth and mid-teens EBIT CAGR through 2028 should “largely soften the blow,” with the stock trading at approximately 13x 2026 earnings. The stock’s 52-week price change stood at approximately -40% as of early March 2026.