IonQ delivered a blockbuster Q4 2025, with revenue of $61.9 million (versus the $40.4M consensus), adjusted EPS of -$0.20 (beating the -$0.48 estimate by 58%), and full-year 2025 revenue of $130 million, up 202% year-over-year. The stock surged over 12% in after-hours trading following the release.

About IonQ

IonQ, Inc. (NYSE: IONQ) is the world’s leading quantum platform company, specializing in trapped-ion quantum computing systems, quantum networking, sensing, and security. Founded in 2015 by Dr. Christopher Monroe and Dr. Jungsang Kim as an offshoot of over 25 years of academic quantum research at the University of Maryland and Duke University, IonQ is headquartered in College Park, Maryland. The company went public via SPAC in October 2021 and trades on the New York Stock Exchange.

As of early March 2026, IonQ carries a market capitalization of approximately $14.1 billion. The company employs roughly 1,130 people, a 178% increase year-over-year, reflecting its rapid scaling. IonQ does not currently pay a dividend. Its trailing twelve-month basic EPS stands at -$2.25, and revenue per employee is approximately $115K. IonQ’s quantum computers are accessible through Amazon Web Services, Microsoft Azure, and Google Cloud, alongside the company’s own cloud service. Under CEO Niccolo de Masi and CFO/COO Inder Singh, IonQ has positioned itself as the first quantum company to surpass $100 million in annual GAAP revenue.

Top Financial Highlights

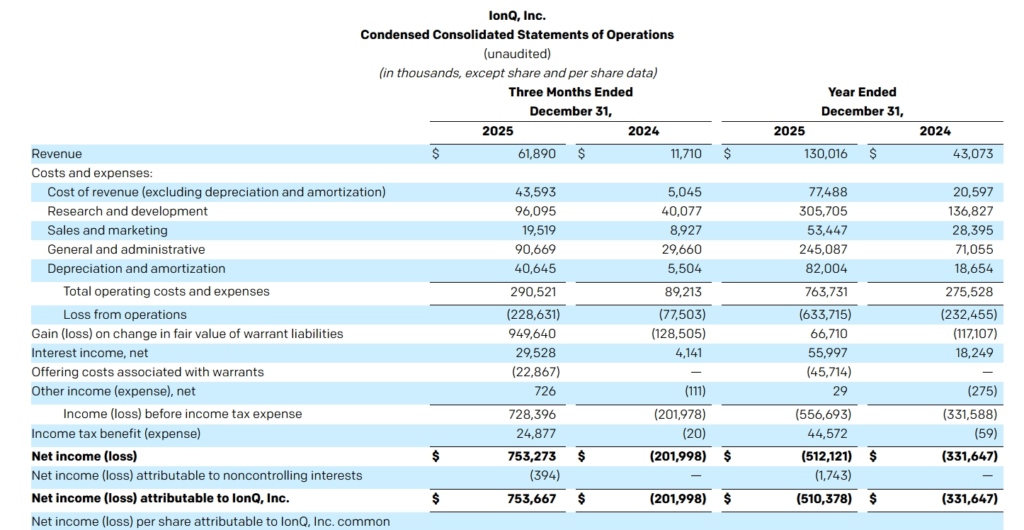

- Q4 2025 revenue reached $61.9 million, reflecting 429% year-over-year growth from $11.7 million and exceeding the guidance midpoint by 55%.

- Full-year 2025 revenue totaled $130.0 million, representing a 202% increase from $43.1 million in 2024 and surpassing guidance expectations by 20%.

- Q4 GAAP net income was $753.7 million, primarily driven by a $949.6 million non-cash gain related to the change in fair value of warrant liabilities.

- Q4 GAAP EPS stood at $2.13 (basic) and $1.93 (diluted).

- Q4 adjusted EPS (non-GAAP) was -$0.20, compared with -$0.15 in Q4 2024.

- Full-year net loss amounted to -$510.4 million, with GAAP EPS of -$1.82.

- Full-year adjusted EPS improved to -$0.60, significantly better than the consensus estimate of -$5.15.

- Q4 gross profit increased to $18.3 million, up 174.5% year-over-year, although adjusted gross margin moderated to 29.6%.

- Q4 adjusted EBITDA loss was –$67.4 million, while the full-year adjusted EBITDA loss totaled -$186.8 million.

- Cash, cash equivalents, and investments rose to $3.3 billion as of December 31, 2025, compared with $363.8 million at the end of the prior year.

- More than 60% of 2025 revenue was generated from commercial customers, and international markets contributed over 30% of total revenue.

- Organic revenue growth approached 80% year-over-year within the overall 202% total growth rate.

- 2026 revenue guidance is projected between $225 million and $245 million, with a midpoint of $235 million. Q1 2026 revenue guidance ranges from $48 million to $51 million.

- 2026 adjusted EBITDA loss is expected between –$330 million and -$310 million.

- Q4 operating loss widened to -$188 million, compared with –$72 million in Q4 2024, reflecting increased investment in research and development and general and administrative expenses.

Beat or Miss?

| Metric | Reported | Analyst Estimate | Difference |

| Q4 Revenue | $61.9M | $40.4M | Beat by 53% |

| Q4 Adjusted EPS | ($0.20) | -$0.48 | Beat by 58% |

| FY 2025 Revenue | $130.0M | Guidance midpoint ~$108M | Beat by 20% |

| FY 2025 Adjusted EPS | ($0.60) | -$5.15 (Zacks) | Significant beat |

| Q4 GAAP EPS (Diluted) | $1.93 | -$0.33 (consensus) | Massive beat (non-cash warrant gain) |

IonQ beat Wall Street expectations across the board. Q4 revenue exceeded consensus by more than 50%, making it one of the largest positive revenue surprises in the quantum computing sector. The adjusted EPS beat was similarly decisive, with the company losing 20 cents versus the nearly 50-cent loss analysts had projected. The GAAP EPS figure of $1.93 was driven almost entirely by a $949.6 million non-cash gain from warrant liability revaluation and should not be interpreted as operating profitability.

What Leadership Is Saying?

“I am pleased to share that IonQ has once again significantly outperformed our revenue guidance range, exceeding the midpoint by 55% for the fourth quarter and 20% for the full year by delivering $61.9 million and $130.0 million respectively. Our strategic evolution into the world’s only full-stack quantum platform company, and strong organic growth, positions us with continued momentum to achieve $235 million in revenue for 2026, at our current guidance midpoint.”-– Niccolo de Masi, Chairman and CEO

“2025 represented historic growth for the company, and our results exceeded our own expectations for both top line and bottom line, as well as consensus estimates. In our 2025 revenues of $130.0 million, more than 60% came from commercial customers, demonstrating that quantum is resonating with the commercial sector. In addition, international sales comprised more than 30% of revenue, demonstrating that our quantum platform is more global. Importantly, our 2025 results included nearly 80% year-over-year organic growth, and in our 2026 guidance, we expect organic growth to be even higher.”— Inder Singh, CFO and COO

Historical Performance

IonQ Q4 2025 vs. Q4 2024

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Revenue | $61.9M | $11.7M | 429% |

| Gross Profit | $18.3M | $6.7M | 174.50% |

| Operating Loss | -$188.0M | -$72.0M | +161% (wider) |

| Net Income (Loss) | $753.7M | -$202.0M | N/M (warrant gain) |

| Adjusted EBITDA Loss | -$67.4M | -$32.8M | +105% (wider) |

| Adjusted EPS | -$0.20 | -$0.15 | -33% (wider loss) |

| R&D Expenses | $96.1M | $40.1M | 139.80% |

| G&A Expenses | $90.7M | $29.7M | 205.70% |

| S&M Expenses | $19.5M | $8.9M | 118.60% |

| Cash and Investments | $3.3B | $363.8M | 807% |

Revenue exploded 429% year-over-year, driven by major quantum system sales (including a fifth-generation, 100-qubit system to KISTI in South Korea) and an expanded QuantumBasel agreement worth over $60 million. However, operating expenses grew substantially as IonQ invested heavily in R&D (up 140%), expanded its G&A infrastructure (up 206%), and scaled sales efforts (up 119%). The GAAP net income of $753.7 million was almost entirely attributable to a non-cash warrant liability revaluation gain of $949.6 million and does not reflect operating profitability.

Historical Performance

Full Year 2025 vs. Full Year 2024

| Category | FY 2025 | FY 2024 | Change (%) |

| Revenue | $130.0M | $43.1M | 202% |

| Net Loss | -$510.4M | -$331.6M | +54% (wider) |

| Adjusted EBITDA Loss | -$186.8M | -$107.2M | +74% (wider) |

| Adjusted EPS | -$0.60 | -$0.50 | -20% (wider loss) |

| Cash and Investments (Year-End) | $3.3B | $363.8M | 807% |

Competitor Comparison

Quantum Computing Sector (FY 2025)

| Category | IonQ (IONQ) | D-Wave (QBTS) | Rigetti (RGTI)* |

| FY 2025 Revenue | $130.0M | $24.6M | ~$7.4M (9-month annualized) |

| FY Revenue Growth (YoY) | +202% | +179% | Revenue declining |

| Q4 2025 Revenue | $61.9M | $2.75M | Est. ~$2.3M |

| FY Gross Margin | ~29.6% (Q4 adj.) | 82.6% | 21% (Q3) |

| FY Net Loss | -$510.4M | -$355.1M | -$201M (Q3 alone) |

| Cash Position | $3.3B | $884.5M | ~$600M |

| Technology | Trapped-ion | Quantum annealing | Superconducting |

| 2026 Revenue Guidance | $225M-$245M | – | – |

IonQ has emerged as the clear revenue leader among pure-play quantum computing companies, with FY 2025 revenue exceeding the combined expected revenue of D-Wave and Rigetti. D-Wave, while posting strong 179% growth, operates at a much smaller scale ($24.6M annually) and missed Q4 revenue estimates.

Rigetti’s revenue has actually declined year-over-year in recent quarters, with Q3 2025 revenue of just $1.9 million, down 20.6% from Q3 2024. IonQ’s $3.3 billion cash position also dwarfs its competitors, providing a significant runway for continued R&D investment, the pending SkyWater Technology acquisition, and international expansion.

How the Market Reacted

IonQ shares surged approximately 12.1% in after-hours trading on February 25, 2026, immediately following the earnings release, with the stock moving from its $33.59 closing price. Pre-market trading the following day saw gains expand to 14-17%, reflecting widespread enthusiasm among institutional and retail investors.

Analyst sentiment remains broadly bullish, with seven firms carrying buy-equivalent ratings and a median price target of $72.50, suggesting significant upside from current levels. However, some analysts caution that the stock remains richly valued at a trailing price-to-sales ratio of approximately 106x, and the widening adjusted EBITDA losses (guided to -$310M to -$330M for 2026) signal that profitability remains distant despite the accelerating top line.