Keenova Therapeutics reported Q4 2025 net sales of $543.0 million, smashing prior-year figures by 104% as Acthar Gel surged 48% YoY to $205.6 million and newly merged XIAFLEX contributed $156.5 million. EPS was not separately disclosed; the company reported a net loss of approximately $173.4 million, driven largely by merger-related non-cash charges. No public stock movement data is available as Keenova has not yet completed its planned NYSE listing – after-hours movement not applicable.

About Keenova

Keenova Therapeutics plc (ticker: MNK, traded OTC; NYSE listing targeted for H2 2026) is a leading U.S. focused branded therapeutics company headquartered in Dublin, Ireland. Formerly known as Mallinckrodt plc, the company rebranded after completing its merger with Endo LP on July 31, 2025, and subsequently spinning off its Par Health generics division on November 10, 2025. Keenova focuses on helping patients with rare or unaddressed medical conditions across therapeutic areas including rheumatology, ophthalmology, nephrology, neurology, pulmonology, orthopedics, urology, and neonatal respiratory critical care.

The company employs approximately 1,600 to 2,687 team members and maintains a robust U.S. manufacturing presence across facilities in Louisiana, New Jersey, New York, Pennsylvania, and Wisconsin. Its flagship products include Acthar Gel (repository corticotropin injection) for chronic or acute inflammatory and autoimmune conditions, XIAFLEX (collagenase clostridium histolyticum) for Dupuytren’s contracture and Peyronie’s disease, INOmax (nitric oxide) for neonatal respiratory, Terlivaz (terlipressin) for hepatorenal syndrome, and Amitiza. The company had pro-forma combined 2024 revenue of $1.7 billion prior to the merger.

Top Financial Highlights

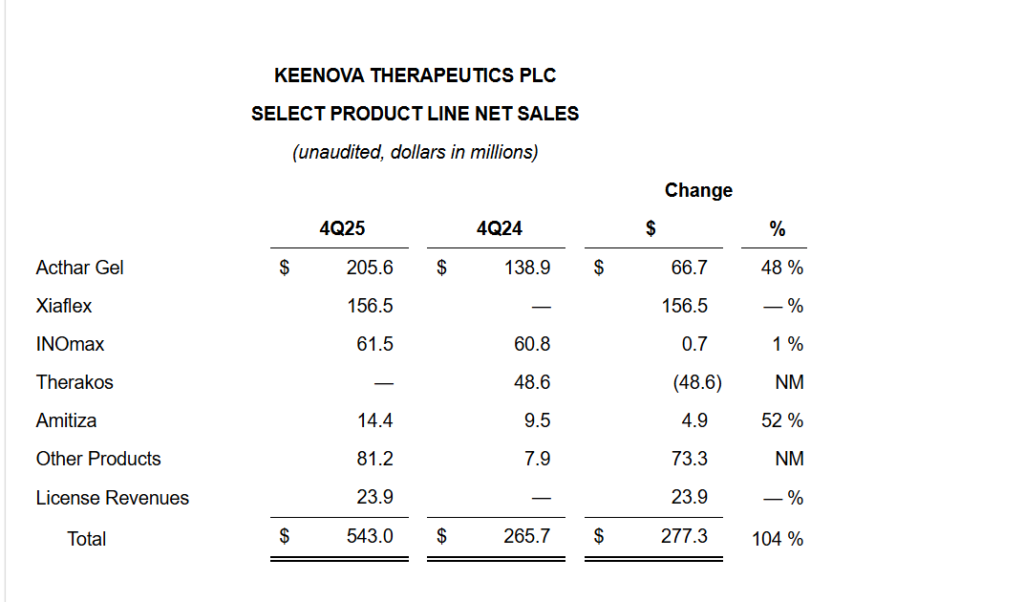

- Net sales from continuing operations in Q4 2025 were $543.0 million, up 104% from $265.7 million in Q4 2024.

- Acthar Gel net sales were $205.6 million, an increase of 48% versus $138.9 million a year earlier, driven by higher demand and SelfJect uptake.

- XIAFLEX net sales reached $156.5 million in Q4 2025 (no comparable sales in Q4 2024 within Keenova), reflecting the post-merger inclusion of this franchise.

- INOmax delivered $61.5 million in net sales versus $60.8 million in Q4 2024, essentially flat year over year.

- Amitiza net sales were $14.4 million, up from $9.5 million, a 52% increase.

- Other Products contributed $81.2 million, sharply higher than $7.9 million in Q4 2024, reflecting portfolio changes and post-merger mix; license revenues added $23.9 million versus zero a year earlier.

- Loss from continuing operations is expected between $105.0 million and $115.0 million for Q4 2025, versus $566.4 million of income from continuing operations in Q4 2024, largely due to non-cash fair value adjustments and the absence of a $754 million Therakos gain recognized last year.

- Net loss (total company) is estimated at $173.4 million for Q4 2025, including results from discontinued operations.

- Adjusted EBITDA from continuing operations is estimated at approximately $215.0 million, up from $67.9 million in Q4 2024, reflecting strong growth in Acthar Gel and XIAFLEX plus initial merger synergies.

- Merger synergies realized in Q4 2025 were $13 million pre-tax; Keenova expects about $100 million in pre-tax merger synergies in 2026 and a $150 million annual run-rate by year three post-merger.

- 2026 guidance: Net sales between $1.94 billion and $2.00 billion, with Adjusted EBITDA of $730–$760 million, excluding potential acquisitions or divestitures such as the prospective sale of the PERCOCET business (~$65 million net sales and $64 million Adjusted EBITDA in 2026).

- XIAFLEX pipeline advanced: a hammer toe proof-of-concept trial met primary safety and key efficacy endpoints, enabling progression to Phase 3, while a Phase 3 study in plantar fibromatosis completed enrollment with topline results expected in Q3 2026.

- Capital allocation will prioritize organic growth in Acthar Gel and XIAFLEX, targeted R&D, and selective portfolio moves, including possible divestiture of PERCOCET.

- NYSE listing: Keenova is preparing to pursue a New York Stock Exchange listing in H2 2026 via a public offering of its ordinary shares, subject to board approval and market conditions.

Beat or Miss?

| Metric | Reported / Indicated | Difference / Analysis |

| Revenue (Net sales, continuing ops) | $543.0 million | Above prior company guidance of $485–$505 million, effectively a top-line beat. |

| Adjusted EBITDA (continuing ops) | ~$215.0 million midpoint | Above prior guidance of $155–$165 million, indicating stronger operating leverage. |

| EPS / GAAP diluted EPS | N/A in release | Only a loss from continuing operations range ($105–$115 million) is provided; no per-share figure. |

| Consensus analyst expectations | N/A | Not cited; press release references performance “above our expectations,” not Street consensus. |

What Leadership Is Saying?

“2025 was a transformational year for Keenova. We completed our evolution into a purpose-driven branded therapeutics company and delivered financial results above our expectations. We also began executing on our synergy plans and remain on track to meet our targets. Our performance underscores the positive momentum in the business and our team’s disciplined execution. We have now delivered two consecutive years of double-digit growth in Acthar Gel, fueled by increasing patient demand and continued uptake of SelfJect. XIAFLEX also performed well in the fourth quarter, and today we announced a significant milestone in our hammer toe clinical program.” – Siggi Olafsson, President and Chief Executive Officer

“Q4 net sales were $542 million and Adjusted EBITDA was $215 million, attributable primarily to the growth in Acthar Gel and the inclusion of XIAFLEX net sales, together with the realization of initial merger-related synergies.” – George Stamoulis, Chief Financial Officer

Historical Performance

Year-over-Year (Keenova, Q4 2025 vs. Q4 2024)

| Category | Q4 2025 (Current) | Q4 2024 (Previous Year) | Change (%) |

| Revenue (Net sales, continuing ops) | $543.0 million | $265.7 million | +104% (driven by Acthar, XIAFLEX, other) |

| Net income (total company) | $(173.4) million net loss | $612.8 million net income (incl. Therakos gain) | Large negative swing, mainly loss of $754 million Therakos gain and higher non-cash charges. |

| Income / (loss) from continuing ops before taxes | Approx. $(110.0) million midpoint | $566.4 million income | Reflects merger-related costs, inventory/intangibles fair value adjustments, and prior-year divestiture gain. |

| Adjusted EBITDA (continuing ops) | $215.0 million (midpoint) | $67.9 million | Strong improvement as branded therapeutics mix and synergies ramp. |

Year-over-Year Competitor Context (Illustrative)

| Category | Keenova Q4 2025 | Key Competitor Q4 2025 | Change (%) vs Competitor YoY |

| Revenue | $543.0 million | N/A in provided texts | N/A — competitor revenue not disclosed. |

| Net income | $(173.4) million | N/A | N/A — competitor profits not provided. |

| Operating expenses / key margin proxy (Adj. EBITDA) | $215.0 million Adjusted EBITDA | N/A | N/A — no comparable competitor margin data in sources. |

How the Market Reacted?

The earnings press release and related materials do not mention intraday or after-hours share price movement following the Q4 2025 announcement. However, the tone of the release is clearly bullish: management highlights revenue and Adjusted EBITDA results ahead of expectations, strong growth in Acthar Gel, successful integration of XIAFLEX, and visible merger synergies.

Forward guidance for 2026 calls for meaningful top-line and EBITDA expansion, supported by pipeline milestones and a prospective NYSE listing in the second half of 2026. Overall, despite GAAP losses driven by non-cash and transactional items, the operational narrative is one of improving fundamentals and increasing scale in branded therapeutics.