LEIFRAS (Nasdaq: LFS) delivered fiscal year 2025 earnings with record revenue of $74.8 million (+13.5% YoY) and operating income of $4.0 million (+20.7% YoY). Basic EPS came in at $0.11. The stock declined approximately 9.32% in the session following the April 8, 2026 announcement, despite the record results.

About LEIFRAS Co., Ltd.

LEIFRAS Co., Ltd. (Nasdaq: LFS) is a Tokyo-headquartered sports and social business company dedicated to youth sports education and community engagement. Founded on August 28, 2001, the company primarily organizes and operates children’s sports schools and sports events across Japan, offering 13 sports programs – including soccer, basketball, baseball, and dance – under the teaching principle of “acknowledge, praise, encourage, and motivate.”

As of December 31, 2025, LEIFRAS ranked No. 1 in Japan for four consecutive years in membership and number of schools in children’s sports schools without company-owned facilities, and No. 1 for two consecutive years in the number of schools where it manages club activities, according to Tokyo Shoko Research.

The company’s market capitalization stands at approximately $54–$65 million, classifying it as a micro-cap stock. LEIFRAS employs 1,055 people and trades with a normalized P/E ratio of approximately 22.6x and zero dividend yield. With 70,688 sports school members and 381 social business school contracts, the company has established a dominant footprint in Japan’s children’s sports instruction services market.

Top Financial Highlights

- Total revenue was JPY 11.7 billion ($74.8 million), an increase of 13.5% from JPY 10.3 billion in fiscal year 2024.

- Income from operations reached JPY 627.4 million ($4.0 million), up 20.7% year over year from JPY 519.8 million.

- Adjusted income from operations was JPY 692.3 million ($4.4 million), representing a 41.8% increase from JPY 488.2 million in fiscal year 2024 (excludes one-time listing-related and transformational expenses).

- Net income was JPY 438.5 million ($2.8 million), an increase of 4.7% from JPY 418.6 million in fiscal year 2024.

- Basic and diluted EPS was JPY 17.41 ($0.11), compared to basic EPS of JPY 16.81 and diluted EPS of JPY 15.78 in fiscal year 2024.

- Gross profit reached JPY 3.47 billion ($22.1 million), up from JPY 2.95 billion in fiscal year 2024, implying a gross margin of approximately 29.5%.

- Operating cash flow was JPY 468.3 million ($3.0 million), more than double the JPY 207.1 million reported in fiscal year 2024.

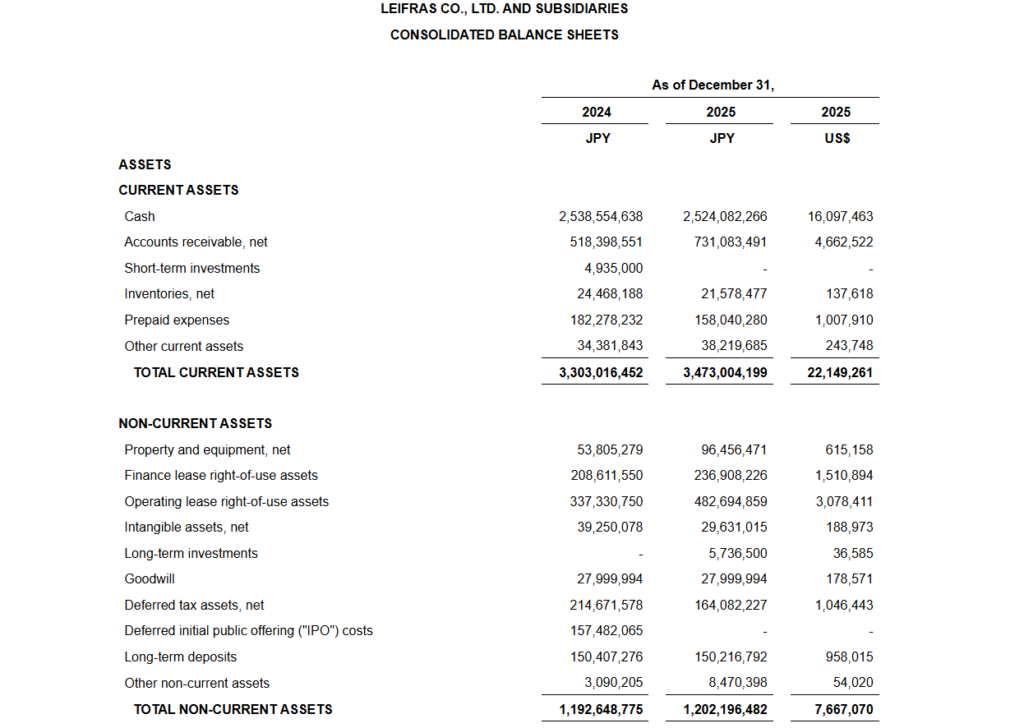

- Cash on hand was JPY 2.52 billion ($16.1 million) as of December 31, 2025.

- Sports school business revenue was JPY 8,560 million ($54.6 million), up 7.8% YoY; membership reached 70,688 members.

- Social business revenue was JPY 3,168 million ($20.2 million), up 32.8% YoY; number of contracted schools grew to 381, up 9.8%.

- FY2026 revenue guidance is set between $82.9 million and $95.7 million, implying growth of 10.8% to 27.9% from FY2025 levels.

- FY2026 operating income guidance is between $4.5 million and $5.4 million, a projected increase of 13.2% to 33.9%.

Beat or Miss?

Analyst consensus estimates for LEIFRAS are not widely published due to its micro-cap size and limited sell-side coverage. The company does not report formal EPS beats or misses against tracked consensus. The table below compares reported results against the company’s own prior-year actuals and internal guidance metrics.

| Metric | Reported (FY2025) | Expected / Prior Guidance | Difference / Analysis |

| Total Revenue | $74.8M (JPY 11.7B) | FY2024: $65.9M (JPY 10.3B) | +13.5% YoY; above the company’s initial FY2025 12–15% growth range |

| Income from Operations | $4.0M (JPY 627.4M) | FY2024: $3.3M (JPY 519.8M) | +20.7% YoY; outperformed revenue growth rate |

| Adjusted Operating Income | $4.4M (JPY 692.3M) | FY2024: $3.1M (JPY 488.2M) | +41.8% YoY; highlights strengthening core profitability |

| Net Income | $2.8M (JPY 438.5M) | FY2024: $2.7M (JPY 418.6M) | +4.7% YoY; lagged operating income growth due to higher taxes |

| Basic EPS | $0.11 (JPY 17.41) | FY2024: $0.11 (JPY 16.81) | Modest improvement; diluted EPS slightly higher than prior year’s $0.10 |

| Operating Cash Flow | $3.0M (JPY 468.3M) | FY2024: $1.3M (JPY 207.1M) | +126.1% YoY; significant improvement in cash generation |

| Analyst Estimates | N/A | N/A | Limited sell-side coverage; no formal consensus tracked |

What Leadership Is Saying?

“For the full fiscal year ended December 2025, we achieved record highs in revenue, income from operations, and adjusted income from operations. Revenue in the sports school business increased by 7.8% compared to the same period last year, and revenue in the social business increased by 32.8% compared to the same period last year… The Japanese government’s club activity reforms will transfer the management of school-based club activities to local communities and the private sector, with the ‘reform implementation period’ from 2026 to 2031 marking the full-scale transition from school-based to local communities and the private sector. This national policy is a powerful tailwind for our company and paves the way for medium- to long-term growth.”

– Kiyotaka Ito, Representative Director and Chief Executive Officer, LEIFRAS Co., Ltd.

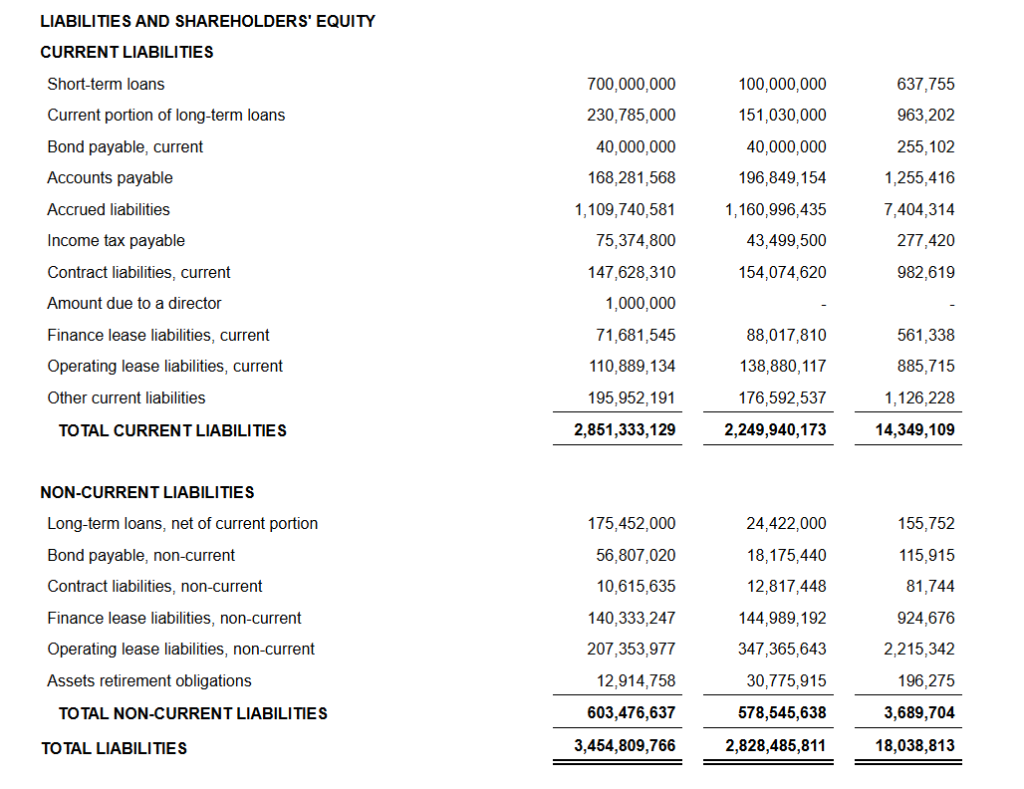

Operating cash flow was JPY 468.3 million ($3.0 million) for fiscal year 2025, compared to JPY 207.1 million for fiscal year 2024, while net cash used in financing activities was JPY 437.0 million ($2.8 million). The company maintains JPY 2.52 billion ($16.1 million) in cash and cash equivalents as of December 31, 2025, and shareholders’ equity expanded to $11.8 million, supported by retained earnings of $4.8 million. The guidance assumes no business acquisitions, restructuring activities, or legal settlements during fiscal year 2026.

– LEIFRAS Investor Relations, representing CFO-level financial commentary

Historical Performance

LEIFRAS YoY Performance: FY2025 vs FY2024

| Category | FY2025 | FY2024 | Change (%) |

| Total Revenue | JPY 11,728M ($74.8M) | JPY 10,330M ($65.9M) | 13.50% |

| Net Income | JPY 438.5M ($2.8M) | JPY 418.6M ($2.7M) | 4.70% |

| Income from Operations | JPY 627.4M ($4.0M) | JPY 519.8M ($3.3M) | 20.70% |

| Adjusted Operating Income | JPY 692.3M ($4.4M) | JPY 488.2M ($3.1M) | 41.80% |

| Gross Profit | JPY 3,465.6M ($22.1M) | JPY 2,947.7M ($18.8M) | 17.60% |

| Operating Cash Flow | JPY 468.3M ($3.0M) | JPY 207.1M ($1.3M) | 126.20% |

| Sports School Revenue | JPY 8,560M ($54.6M) | JPY 7,944M ($50.7M) | 7.80% |

| Social Business Revenue | JPY 3,168M ($20.2M) | JPY 2,385M ($15.2M) | 32.80% |

| Basic EPS | JPY 17.41 ($0.11) | JPY 16.81 ($0.11) | 3.60% |

Competitor Comparison

LEIFRAS operates primarily in Japan’s children’s sports school and club activity management market. Its closest publicly tracked competitor in Japan’s broader child-raising support and youth services sector is JP Holdings, Inc. (TSE: 2749), which operates nursery schools, school clubs, and children’s houses nationwide.

JP Holdings is a significantly larger company, with the highest net sales, operating income margin, and market capitalization among Japanese childcare support peers. Note: JP Holdings’ fiscal year ends in March; figures below reflect the FY ending March 2025 vs March 2024 for comparability to LEIFRAS’s calendar-year FY2025 report.

| Category | JP Holdings FY3/25 | JP Holdings FY3/24 | Change (%) |

| Net Sales | JPY 41,147M (~$270M) | JPY 37,856M (~$248M) | 8.70% |

| Operating Income | JPY 5,809M (~$38M) | JPY 4,584M (~$30M) | 26.70% |

| Net Income | JPY 3,920M (~$26M) | JPY 2,929M (~$19M) | 33.90% |

| Operating Income Margin | 14.10% | 12.10% | +2.0 pts |

| Operating Cash Flow | JPY 4,205M (~$28M) | JPY 5,598M (~$37M) | -24.90% |

| Total Facilities | 345 | ~300 | ~+15% |

While both companies serve children’s educational and community-based service markets in Japan, their business models differ. LEIFRAS focuses on sports instruction via asset-light school operations (no owned facilities), while JP Holdings operates licensed nursery schools and after-school care facilities that rely heavily on government subsidies. JP Holdings is roughly 3.5x larger by revenue, but LEIFRAS’s social business is growing considerably faster (32.8% YoY) and stands to benefit more directly from Japan’s 2026-2031 club activity reform policy.

How the Market Reacted?

Despite reporting record highs in revenue and operating income, LEIFRAS shares declined 9.32% on the day the earnings were announced (April 8, 2026), removing approximately $6 million from the company’s market capitalization and bringing it to roughly $57.8 million. The negative reaction is consistent with the company’s historical earnings pattern, where past earnings-related moves averaged approximately -5.91% in the trading session following results.

Investors appear to have focused on the relatively modest net income growth of only 4.7%, which lagged the headline revenue and operating income figures, as well as potential execution risks tied to the aggressive FY2026 guidance range of $82.9 million to $95.7 million in revenue. Prior to the announcement, the stock was trading around $2.52, well below its 52-week high of $12.49 and closer to its 52-week low of $1.58, reflecting the broader caution around this micro-cap name.