Tiny Ltd. posted FY2025 total revenue of $203.8M (up 5% YoY), with a basic loss per share of -$1.24 (improved from -$2.12). Adjusted EBITDA surged 22% to $37.9M. After-hours stock movement showed a decline of approximately 2.44%, with shares closing near $5.19 on the TSX on March 30, 2026.

About Tiny Ltd.

Tiny Ltd. (TSX: TINY) is a Canadian technology holding company headquartered in Victoria, British Columbia, founded in 2007. The company operates with a founder-friendly acquisition strategy, focusing on technology businesses with unique competitive advantages, recurring or predictable revenue streams, and strong free cash flow generation. It currently operates through three principal reporting segments: Digital Services, Software and Apps, and Creative Platform.

As of March 30, 2026, Tiny carries a market capitalization of approximately CAD $152 million, with trailing twelve-month revenue of roughly CAD $199.65 million. The company’s portfolio spans global design services (Metalab), DJ software (Serato), e-commerce apps (WeCommerce), and designer communities (Dribbble, Creative Market), among others. Tiny does not pay a dividend and has approximately 29.31 million shares outstanding following an 8:1 share consolidation completed in October 2025. The stock’s 52-week range sits between $5.02 and $10.96, reflecting a period of significant valuation compression.

Top Financial Highlights

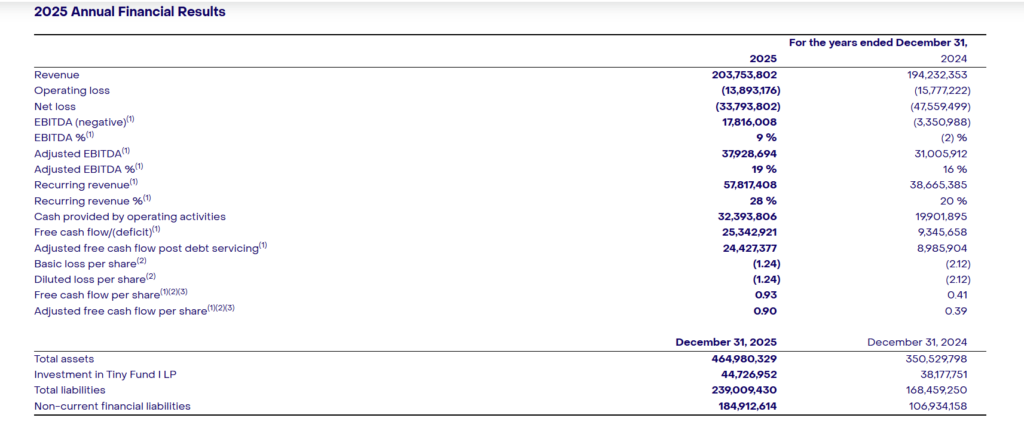

- FY2025 total revenue reached $203.8 million, a 5% increase year-over-year from $194.2 million in FY2024

- Excluding strategic divestitures (WeWorkRemotely, Frosty Studio, 8020 Design), pro-forma FY2025 revenue growth was 12%

- Q4 2025 revenue was $51.7 million, up $4.1 million or 9% compared to Q4 2024

- Recurring revenue in FY2025 was $57.8 million, a 50% increase year-over-year from $38.7 million, now representing 28% of total revenue (vs. 20% in FY2024)

- Adjusted EBITDA for FY2025 was $37.9 million, a 22% increase from $31.0 million in FY2024, with an Adjusted EBITDA margin of 19% (up from 16%)

- Q4 2025 Adjusted EBITDA was $9.8 million, essentially flat versus $10.1 million in Q4 2024 (a 2% decrease)

- Net loss for FY2025 was $33.8 million, a 29% improvement from a net loss of $47.6 million in FY2024

- Basic and diluted loss per share for FY2025 was -$1.24, compared to -$2.12 in FY2024

- Free Cash Flow for FY2025 was $25.3 million, a 171% increase from $9.3 million in FY2024; free cash flow per share was $0.93

- Cash from operating activities for FY2025 was $32.4 million, up from $19.9 million in FY2024

- Cash on hand at December 31, 2025 was $29.3 million, up from $22.9 million at end of FY2024

- Total senior debt (excluding convertible debentures) reduced from $116.9 million to $98.7 million, with $34.1 million in total debt repaid during FY2025

- Net Debt to Adjusted EBITDA improved to 2.4x from 3.0x in Q4 2024, within the company’s stated target range of 2.0 to 2.5x

- Tiny Fund I NAV increased 17% to $44.7 million (USD$32.6 million); Letterboxd reached 26.1 million users, up 47% from Q4 2024

- Company repurchased 113,488 Common Shares under its Normal Course Issuer Bid (NCIB) at prices between $6.67 and $10.00 per share

Beat or Miss?

| Metric | Reported (FY2025) | Prior Year (FY2024) | Difference / Analysis |

| Total Revenue | $203.8M | $194.2M | +5% YoY; in line with growth trajectory |

| Q4 Revenue | $51.7M | $47.6M | +9% YoY; accelerated quarterly growth |

| Adjusted EBITDA | $37.9M | $31.0M | +22% YoY; exceeded prior year significantly |

| Adjusted EBITDA Margin | 19% | 16% | +300bps expansion |

| Recurring Revenue | $57.8M | $38.7M | +50% YoY; well ahead of trend |

| Net Loss | -$33.8M | -$47.6M | Improved 29% YoY |

| Basic LPS | ($1.24) | ($2.12) | Significant per-share improvement |

| Free Cash Flow | $25.3M | $9.3M | +171% YoY; transformational improvement |

| Net Debt / Adj. EBITDA | 2.4x | 3.0x | Within 2.0-2.5x target range |

| Cash on Hand | $29.3M | $22.9M | +$6.4M YoY |

What Leadership Is Saying?

CEO Jordan Taub on strategy and the Serato acquisition:

“Serato was transformational for our recurring revenue profile in 2025, leading to a 50% increase year-over-year. As a company, we will continue to focus on both organic and acquisition-related opportunities to enhance this recurring revenue base.”

The CEO also highlighted the portfolio’s momentum, noting that Letterboxd and Metalab were recently recognized among the most innovative companies in the world by Fast Company, and pointed to Dribbble’s services marketplace showing continued GMV growth as a future revenue driver.

CFO Mike McKenna on financials and leverage:

“Our net debt to Adjusted EBITDA ratio of 2.4 sits within our target range of 2-2.5 times, and the trend line shows a consistent, deliberate deleveraging story even when factoring in financing for the Serato acquisition.”

McKenna further noted that free cash flow of CAD $25.3 million for the full year “represents a 171% increase over 2024″ and called it “the clearest signal of how much stronger the business has become,” while acknowledging that Q4 free cash flow was softer at $1.3 million due to working capital timing and semi-annual interest payments on the convertible debentures.

Historical Performance

Year-Over-Year Comparison (FY2025 vs FY2024)

| Category | FY2025 | FY2024 | Change (%) |

| Total Revenue | $203.8M | $194.2M | 5% |

| Recurring Revenue | $57.8M | $38.7M | 50% |

| Adjusted EBITDA | $37.9M | $31.0M | 22% |

| Net Loss | -$33.8M | -$47.6M | -29% (improved) |

| Free Cash Flow | $25.3M | $9.3M | 171% |

| Operating Cash Flow | $32.4M | $19.9M | 63% |

| Basic LPS | ($1.24) | ($2.12) | +41% (improved) |

| Cash on Hand | $29.3M | $22.9M | 28% |

| Net Debt / Adj. EBITDA | 2.4x | 3.0x | -0.6x |

| Total Assets | $465.0M | $350.5M | 33% |

Quarterly Comparison (Q4 2025 vs Q4 2024)

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Revenue | $51.7M | $47.6M | 9% |

| Adjusted EBITDA | $9.8M | $10.1M | -2% |

| Net Loss | -$40.9M | -$27.4M | Worsened (impairment) |

| Net Debt / Adj. EBITDA | 2.4x | 3.0x | -0.6x |

| Free Cash Flow (Q4) | $1.3M | ~$11.3M | Softer (timing/interest) |

Competitor Comparison (YoY)

Tiny operates in the Canadian technology holding company space, with Constellation Software (TSX: CSU) being the most commonly cited comparable due to its vertical market software acquisition model. The table below compares key metrics across peers for the most recent full year.

| Category | Tiny Ltd. (TINY) FY2025 | Tiny Ltd. (TINY) FY2024 | Change (%) |

| Revenue | $203.8M CAD | $194.2M CAD | 5% |

| Adj. EBITDA | $37.9M CAD | $31.0M CAD | 22% |

| Net Income / Loss | -$33.8M CAD | -$47.6M CAD | -29% loss (improved) |

| Market Cap (approx.) | ~$152M CAD | ~$240M CAD | -37% decline |

| Recurring Revenue % | 28% | 20% | +8pp |

Constellation Software (TSX: CSU) Context: Constellation Software reported revenues of approximately CAD $10.74 billion with a net income of CAD $453.54 million and a market cap that towers over Tiny’s. While both firms follow an acquire-and-hold strategy, Constellation operates at a significantly larger scale across hundreds of vertical market software businesses globally. Tiny is often described informally as a smaller-cap analog to Constellation, particularly given its focus on founder-friendly acquisitions and long-term holding periods.

Lightspeed Commerce (TSX: LSPD) and Shopify (TSX: SHOP) also operate in overlapping segments of Canadian technology, particularly in e-commerce software, where Tiny’s WeCommerce and Software and Apps businesses compete. Shopify reported revenues exceeding CAD $10 billion, operating in a far larger scale, while Tiny remains focused on niche platform acquisitions.

How the Market Reacted?

Tiny Ltd. shares declined approximately 2.44% on March 30, 2026, the day of the earnings release, closing at approximately $5.19 CAD on the TSX, down from the prior close of $5.30. The stock has been under significant pressure, sitting near its 52-week low of $5.02, well off its 52-week high of $10.96, and reflecting a one-year decline of approximately 48%.

The RSI indicator sits at an oversold reading of 23.45, suggesting prolonged selling pressure despite the operationally positive results. The market reaction appears to reflect investor concern over the company’s persistent net losses, significant non-cash goodwill impairment charges of $37.0 million recorded in Q4 2025, and softer Q4 free cash flow of only $1.3 million, which overshadowed the otherwise strong full-year adjusted EBITDA growth, free cash flow improvement of 171%, and the company’s successful deleveraging trajectory.