VNET Group (Nasdaq: VNET) posted Q4 2025 total net revenues of $384.2 million (RMB 2.69 billion), up 19.6% year-over-year, beating consensus. Adjusted EPS came in at break-even ($0.00), missing the $0.04 estimate by 100%. Full-year 2025 revenues and adjusted EBITDA both exceeded guidance. Shares traded down approximately 9.28% on the earnings date amid an EPS miss.

About VNET Group

VNET Group, Inc. (Nasdaq: VNET) is a leading carrier- and cloud-neutral internet data center (IDC) services provider headquartered in Beijing, China. The company was founded in 1996 and operates over 50 data centers across more than 30 cities in China, serving a diversified base of over 7,000 enterprise customers. Its core services include managed hosting (wholesale and retail IDC), cloud services, and business VPN solutions.

As of March 2026, VNET Group carries a market capitalization of approximately $2.51 billion and employs roughly 2,600 to 3,290 people. The company reported trailing twelve-month revenue of $1.42 billion (RMB 9.95 billion), reflecting 20.5% year-over-year growth. The stock has no current dividend yield and trades at a forward P/E of approximately 257.53, reflecting high growth expectations embedded in the price. Analysts rate the stock a “Strong Buy” with a consensus price target of $12.60, implying around 35% upside from current levels.

Top Financial Highlights

- Total Q4 Net Revenue reached RMB 2.69 billion (US$384.2 million), up 19.6% year-over-year

- Wholesale IDC Revenue surged 47.1% year-over-year to RMB 978.1 million (US$139.9 million)

- Retail IDC Revenue grew 7.6% year-over-year to RMB 1.04 billion (US$148.5 million)

- Non-IDC Business Revenue (cloud and VPN) increased 8.8% to RMB 670.8 million (US$95.9 million)

- Gross Profit in Q4 was RMB 540.4 million (US$77.3 million), up 7.0% year-over-year

- Gross Margin in Q4 was 20.1%, down from 22.5% in Q4 2024

- Adjusted EBITDA (non-GAAP) grew 11.6% to RMB 805.1 million (US$115.1 million); margin at 30.0% vs. 32.1% a year ago

- Net Income attributable to VNET in Q4 was RMB 304.7 million (US$43.6 million), swinging from a net loss of RMB 11.1 million in Q4 2024 – aided by a RMB 469.8 million gain on deconsolidation of a subsidiary

- Diluted EPS was essentially break-even at RMB 0.001 (US$0.00) per share, or US$0.00 per ADS

- Full Year 2025 Revenue reached RMB 9.95 billion (US$1.42 billion), up 20.5% year-over-year, exceeding guidance

- Full Year Adjusted EBITDA grew 22.6% to RMB 2.98 billion (US$425.9 million), also beating guidance

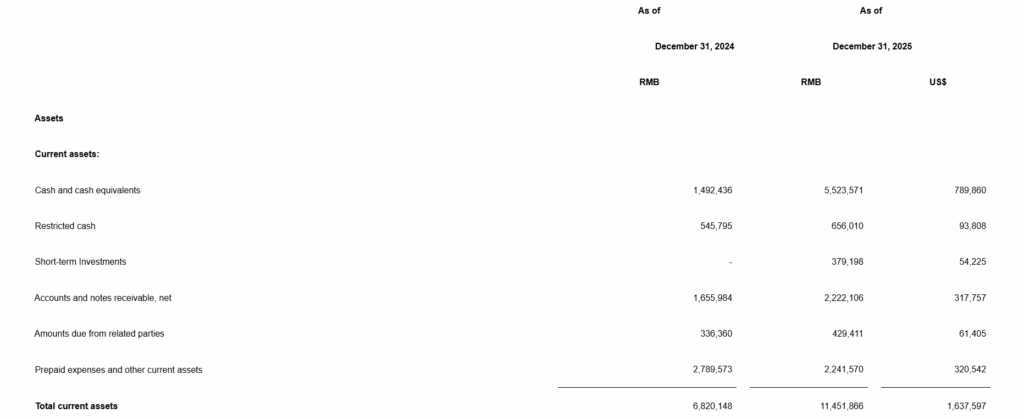

- Cash and Liquidity as of December 31, 2025 totaled RMB 6.58 billion (US$941.1 million) in aggregate cash, restricted cash, and short-term investments

- Operating Cash Flow (Q4) was RMB 546.4 million (US$78.1 million), down slightly from RMB 572.2 million in Q4 2024

- 2026 Full Year Guidance targets total net revenues of RMB 11.5 billion to RMB 11.8 billion (15.6% to 18.6% growth) and adjusted EBITDA of RMB 3.55 billion to RMB 3.75 billion (19.2% to 25.9% growth)

CONSOLIDATED Report

Beat or Miss?

| Metric | Reported | Estimated | Difference / Analysis |

| Q4 Total Revenue | US$384.25 million | US$368.64 million (consensus) | Beat by +2.27% |

| Adjusted EPS | $0.00 (break-even) | $0.04 (consensus) | Missed by -100% |

| Full Year Revenue | RMB 9.95 billion | RMB 9.55–9.87 billion (guidance range) | Exceeded full-year guidance |

| Full Year Adjusted EBITDA | RMB 2.98 billion | RMB 2.9–2.945 billion (guidance range) | Exceeded full-year guidance |

| Adjusted EBITDA (Q4) | US$115.1 million | US$0.18 per share (consensus) | Missed adjusted EPS by wide margin |

What Leadership Is Saying?

“We closed 2025 with strong full-year results, successfully achieving our 2025 delivery plan with a record 404MW delivered and exceeding guidance on both revenues and adjusted EBITDA. Our wholesale IDC business maintained exceptional momentum, driven by strong customer demand and our proven ability to scale capacity rapidly and efficiently. Our order momentum remained robust, with a total of 135MW of new wholesale orders secured in the fourth quarter of 2025. Moving forward, we will further advance our Hyperscale 2.0 framework to achieve sustainable, high-quality growth and create long-term value for all stakeholders.” – Josh Sheng Chen, Founder, Executive Chairperson and Interim CEO, VNET Group

“In the fourth quarter of 2025, we continued to achieve high-quality growth amid strong AI-driven demand. Total net revenues increased 19.6% year-over-year to RMB 2.69 billion, led by 47.1% year-over-year growth in wholesale revenues. Adjusted EBITDA increased 11.6% year-over-year to RMB 805.1 million. For the full year, total net revenues increased 20.5% year-over-year to RMB 9.95 billion, and adjusted EBITDA grew 22.6% to RMB 2.98 billion, both exceeding our 2025 full year guidance. We remain committed to disciplined capital allocation, advancing capital recycling and other strategic initiatives to reinforce our financial foundation and support long-term sustainable growth.” – Peter Zhihua Zhang, Senior Vice President of Operational Finance, VNET Group

Historical Performance

Q4 2025 vs Q4 2024 (Year-over-Year Comparison)

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Total Net Revenue | RMB 2.69 billion (US$384.2M) | RMB 2.25 billion | +19.6% |

| Wholesale IDC Revenue | RMB 978.1 million (US$139.9M) | RMB 665.2 million | +47.1% |

| Retail IDC Revenue | RMB 1.04 billion (US$148.5M) | RMB 964.8 million | +7.6% |

| Non-IDC Revenue | RMB 670.8 million (US$95.9M) | RMB 616.5 million | +8.8% |

| Gross Profit | RMB 540.4 million (US$77.3M) | RMB 504.9 million | +7.0% |

| Gross Margin | 20.10% | 22.50% | -2.4 ppts |

| Adjusted EBITDA | RMB 805.1 million (US$115.1M) | RMB 721.3 million | +11.6% |

| Adjusted EBITDA Margin | 30.00% | 32.10% | -2.1 ppts |

| Total Operating Expenses | RMB 387.4 million | RMB 267.9 million | +44.6% |

| Net Income (Loss) to VNET | RMB 304.7 million (US$43.6M) | RMB -11.1 million | Swing to profit |

| Operating Cash Flow | RMB 546.4 million | RMB 572.2 million | -4.50% |

Competitor Comparison

VNET’s closest listed peer in China’s IDC and data center market is GDS Holdings (Nasdaq: GDS; HKEX: 9698). Both companies reported Q4 and full-year 2025 results around the same time, providing a direct industry benchmark.

VNET vs GDS Holdings – Q4 2025 and Full Year 2025

| Category | VNET Q4 2025 | VNET FY2025 Change | GDS Q4 2025 | GDS FY2025 Change |

| Net Revenue | RMB 2.69 billion (US$384.2M) | +20.5% (FY) | RMB 2.92 billion (US$417.8M) | +10.8% |

| Gross Profit | RMB 540.4 million (US$77.3M) | +19.7% (FY) | RMB 612.4 million | +5.9% |

| Gross Margin | 20.10% | 22.0% (FY) | 21.00% | N/A |

| Adjusted EBITDA | RMB 805.1 million (US$115.1M) | +22.6% (FY) | US$195.3 million | +5.2% |

| Net Income (Loss) | RMB 304.7M profit (Q4 VNET) | Net loss RMB 251.8M (FY) | Net loss US$66.2M (Q4) | Net income US$137.2M (FY) |

| Revenue Growth Rate | +19.6% YoY (Q4) | +20.5% (FY) | +8.6% YoY (Q4) | +10.8% (FY) |

VNET’s wholesale IDC segment, fueled by AI-driven demand, is growing significantly faster than GDS on a percentage basis. GDS, however, carries a larger absolute revenue base and reported full-year net income of US$137.2 million in 2025 versus VNET’s full-year net loss of US$36 million. Both companies are expanding capacity aggressively, with GDS noting record gross new bookings and move-ins in 2025.

How the Market Reacted?

VNET shares fell approximately 9.28% intraday on March 16, 2026, the day Q4 results were announced, despite the revenue beat. The sell-off was largely attributed to the adjusted EPS miss – coming in at break-even $0.00 against a consensus of $0.04 and the 44.6% jump in total operating expenses. Analysts and market observers had flagged the risk of a “sell the news” reaction after the stock had already surged 14.71% in the week leading up to the release, as investors priced in high expectations ahead of the report.

For year-to-date context, VNET shares had still gained approximately 24.2% since January 1, 2026, significantly outperforming the S&P 500’s 3.1% decline over the same period. The 2026 guidance of 15.6% to 18.6% revenue growth and adjusted EBITDA expansion of 19.2% to 25.9% provides a constructive forward outlook, though capital expenditure of RMB 10 billion to RMB 12 billion signals continued heavy investment ahead.