Introduction

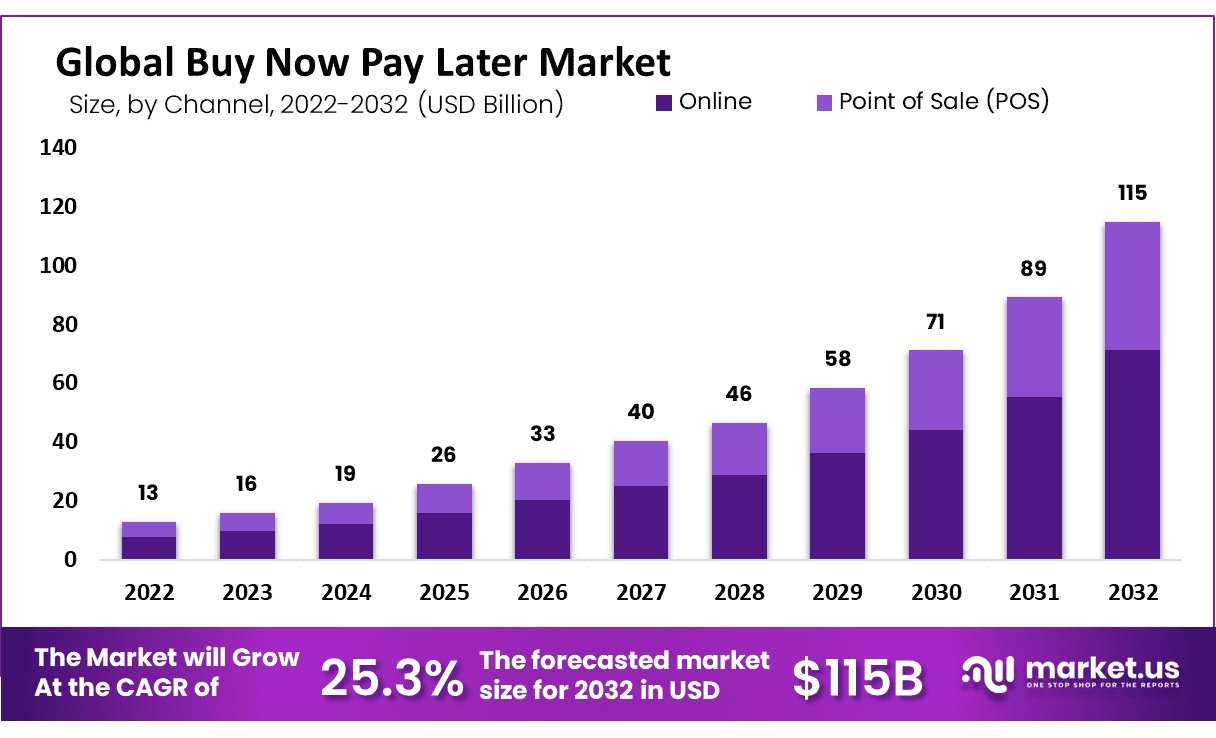

The Global Buy Now Pay Later (BNPL) market is set to grow from about USD 16 billion in 2023 to roughly USD 115 billion by 2032, reflecting a strong CAGR of 25.3% as consumers and merchants embrace flexible, installment-based digital payments across channels and sectors. Buy Now Pay Later is a digital payment option that allows consumers to split purchases into short term installments, often with no interest if payments are made on time. It is widely used in online shopping and is now expanding into physical retail, travel, healthcare, and everyday services. BNPL is positioned between traditional credit cards and debit payments, offering faster approval and simpler user experience. The model is popular among younger consumers who prefer transparent repayment schedules and limited credit exposure compared to revolving credit products.

Several strong factors are driving the growth of this segment. The rise of ecommerce has played a major role, as BNPL is often embedded directly at checkout, reducing cart abandonment. Consumer behavior has shifted toward flexible payments, especially during periods of inflation and higher living costs. Surveys show that a large share of BNPL users choose the option to better manage monthly cash flow rather than for lack of access to credit. Adoption is also supported by mobile app usage, instant approval processes, and higher acceptance among consumers who avoid credit cards due to interest charges and complex terms.

Demand for Buy Now Pay Later continues to expand across both consumer and merchant segments. A significant portion of online shoppers report higher purchase likelihood when BNPL is available, and merchants often see improved conversion rates and larger average order values. Usage is highest among younger age groups, but adoption is steadily increasing among middle income households for electronics, fashion, and essential goods. As digital payments become more embedded in daily spending, BNPL is increasingly viewed as a mainstream payment choice rather than an alternative option, supporting stable and broad based demand growth.

Key Takeaways

- North America leads with over 32% share and about USD 4.6 billion revenue, supported by high e-commerce penetration and advanced payment infrastructure.

- Online channels account for more than 62% of BNPL volume, reflecting strong integration into digital checkouts.

- Large enterprises hold over 61% share by enterprise size, leveraging BNPL to enhance loyalty and conversion at scale.

- Retail end users capture more than 71.3% share, especially in electronics, fashion, and home categories where ticket sizes are higher.

- Surveys show only 9% of Americans mainly use cash, while more than half use cards, and BNPL usage on events like Amazon Prime Day grew about 20% year on year.

- Projections from major institutions suggest the BNPL market could expand by 10-15 times by mid‑decade, with potential uplift to overall credit limits if integrated with cards.

Key Statistics

- According to MarketingLTB, 41% of BNPL users reported paying late on a BNPL loan at least once in the past year, based on findings from a LendingTree survey.

- A large share of BNPL users are aged 35 or younger, indicating strong adoption among younger consumers, supported by data from Empower.

- BNPL is most commonly used across fashion and clothing, electronics, furniture, beauty products, and groceries, reflecting its role in everyday and discretionary spending.

- Several consumer surveys indicate that around 26% of Americans are more likely to complete a purchase when BNPL options are available, highlighting its influence on buying behavior.

- Based on scoop.market.us, Sweden leads the domestic e-commerce market share for Buy Now, Pay Later services with a strong 23%, followed by Germany at 19%, reflecting high BNPL adoption in Northern and Western Europe.

- Norway ranks third with a 15% market share, while Finland and Australia follow with 12% and 10%, respectively, showing solid BNPL penetration in these markets.

- New Zealand shares a similar position with Australia, also recording a 10% share of domestic e-commerce transactions through BNPL services.

- The Netherlands holds a 9% market share, with Denmark close behind at 8%, indicating moderate but growing BNPL usage.

- Belgium ranks ninth with a 7% share, while the United Kingdom completes the top ten with 5%, reflecting steady adoption across these economies.

- France and Japan are tied at the eleventh position, each accounting for 4% of their domestic e-commerce markets through BNPL solutions.

- Countries such as India, Indonesia, Singapore, and the Philippines each record a 3% market share, placing them slightly lower in BNPL adoption rankings.

- Italy, Spain, the United States, and Poland currently show a 2% share each, highlighting relatively early-stage adoption of BNPL in these markets.

- According to ExplodingTopics, an estimated 360 million people worldwide were using Buy Now, Pay Later services in 2022, reflecting rapid global adoption.

- The number of BNPL users is projected to more than double within the next five years, driven by expanding e-commerce usage and flexible payment preferences.

- By 2027, the global BNPL user base is expected to reach 900 million users, representing a 157% increase from 2022 levels.

Key Market Segment

By channel

- Online

- Point of Sale (POS)

By enterprise size

- Large Enterprises

- Small & Medium Enterprises

By end user

- Banking, Financial Services & Insurance (BFSI)

- Consumer Electronics

- Fashion & Garment

- Healthcare

- Leisure & Entertainment

- Retail

- Other End-Users

Top Key Players

- Affirm, Inc.

- Afterpay Pty Ltd

- Atome

- Flipkart Internet Private Limited

- Grab Holdings Inc.

- Hoolah Holdings Pte Ltd.

- Klarna Inc.

- LatitudePay Australia Pty Ltd

- Laybuy Group Holdings Limited.

- Mastercard International Incorporated

- Monzo Bank Limited

- One97 Communications Limited (Paytm)

- Openpay Pty Ltd.

- Payl8r (Social Money Ltd.)

- PayPal Holdings, Inc.

- Perpay Inc.

- Sezzle Inc

- SPLITIT USA INC.

- Zip Co Limited

- Other Key Players

Use Cases

Online shopping checkout

Buy Now Pay Later is widely used at online checkout pages. It allows shoppers to split payments into smaller parts, making higher-value items easier to afford without upfront pressure.

Electronics and gadgets purchases

Consumers often use Buy Now Pay Later for smartphones, laptops, and home electronics. The option supports planned purchases where users prefer flexible payment instead of full payment at once.

Fashion and apparel buying

The model is commonly used for clothing and footwear. Shoppers can try products first and manage payments later, which reduces hesitation and return-related concerns.

Furniture and home improvement

Buy Now Pay Later supports purchases such as furniture, appliances, and home decor. It helps households manage large expenses without affecting monthly cash flow.

Travel and hospitality bookings

The service is used for flight tickets, hotel stays, and holiday packages. It allows customers to plan trips in advance while spreading the cost over time.

Healthcare and wellness services

Some users rely on Buy Now Pay Later for dental care, medical tests, and wellness treatments. This use case supports access to essential services without immediate financial stress.

Education and skill courses

Online courses, professional certifications, and training programs use Buy Now Pay Later to attract learners who prefer flexible payment for career-focused investments.

Everyday retail spending

The model is also used for daily needs such as groceries, personal care, and household items. It supports short-term budgeting and smoother expense management.

Recent Development

- October, 2025, Affirm called for fee caps and credit reporting to improve BNPL reputation.

- March, 2025, Affirm partnered with Experian for better credit transparency on loans.

- December, 2025, Afterpay added more mid-sized merchants to grow its payment network.

Conclusion

The buy now pay later market is becoming a core element of modern consumer payments as it scales rapidly from a relatively small base to a major global volume contributor over the next decade. Strong adoption in retail, especially online, and heavy use by large enterprises show that BNPL is now a mainstream checkout feature rather than a niche option. Regulatory scrutiny, credit‑risk management, and competition with cards and traditional loans remain challenges, but continued e-commerce growth, younger customer demand, and tighter integration with banking and card products position BNPL as a lasting part of the digital credit landscape.

Read More – https://market.us/report/buy-now-pay-later-market/