Introduction

Hino Motors Statistics: Hino Motors, a key subsidiary of Toyota Motor Corporation, is navigating a critical recovery phase from 2025 to 2026 because of regulatory challenges and market volatility. The company operates in the global commercial vehicle segment, which includes its operations with trucks and buses and diesel engine systems. The business period shows Hino’s performance through two opposing results of decreasing revenue and unit sales but rising profitability, which comes from cost reduction and corporate restructuring.

Hino plans to restore its market credibility through its increasing investments in electric vehicle technology and regulatory compliance initiatives. The article provides thorough statistical data along with financial information and a research-based examination of Hino Motors’ current business development.

Editor’s Choice

- Hino Motors’ FY2025 net sales increased 11.9% YoY to ¥1.70 trillion, indicating demand recovery.

- Operating income improved to ¥57.49B from a ¥8.10B loss, signalling operational turnaround.

- The ordinary income stayed below zero, with an ordinary income of -¥39.31 billion, because of financial cost pressures.

- The company reported a net loss of -¥217.75 billion, which resulted from exceptional expenses that outweighed its previous profit of ¥17.09 billion.

- The EPS metric dropped to -379.34, which showed a large decline in shareholder value from its previous value of 29.77.

- The return on equity decreased to -76.3% because the company established capital utilization methods that proved unproductive.

- The operating margin grew from -0.5% to 3.4% because the company achieved initial success in its expense management program.

- The total asset value of the company increased to ¥1.48 trillion, which represented a 0.9% growth from the previous period.

- The value of net assets decreased to ¥251.02 billion, which represented a 45.8% decrease because of equity losses.

- The equity ratio experienced a rapid decrease from 26.8% to 12.1%, which made the company more vulnerable to financial risks.

- The operating cash flow showed positive results with an operating cash flow of ¥1.13 billion after recovering from a previous loss of -¥110.41 billion.

- The cash reserves of the company rose to ¥88.42 billion, which represented a 30.6% increase and enhanced the company’s ability to manage short-term financial obligations.

- The domestic sales revenue experienced a 24.8% increase because of strong customer demand in the Japanese market.

- FY2026 revenue is projected to decline 11.6% to ¥1.5T amid a global slowdown.

- ARCHION merger will combine 165,000+ vehicle volumes and €16B+ revenue scale.

Hino Motors Revenue Growth

(Source: hino-global.com)

- Hino Motors’ FY 2025 financial results showcase a typical business situation where revenue growth failed to produce better profit results because the enterprise struggled with its fundamental cost operations, efficiency, and ability to recover profit margins.

- The company achieved net sales of ¥1,697,229 million, which represented an 11.9% year-on-year (YoY) increase from its previous year’s sales of ¥1,516,255 million in FY 2024 because customers started buying its main commercial vehicle products again.

- The operating income reached ¥57,490 million after recovering from a previous operating loss of ¥8,103 million that the company reported in FY 2024 because the business improved its capacity to generate revenue while implementing successful cost-cutting methods.

- The company sustained a negative ordinary income of ¥39,310 million, which improved from a previous year’s loss of ¥9,233 million,n but showed that non-operating expenses and financing costs still affected operations.

- The profit that belongs to the parent company shareholders decreased to a loss of ¥217,753 million, which showed an extreme shift from the previous year’s profit of ¥17,087 million.

- The dramatic financial transformation shows how extraordinary expenses, restructuring expenses, and potential compliance expenses affect core business operations, which determine how investors view the company.

- The company experienced a decrease in total comprehensive income, which reached -¥206,726 million, because it faced pressures that affected its overall financial valuation and balance sheet situation.

- The company needs to solve its profit sustainability problem, cost control issue, and financial restructuring needs in order to bring back shareholder value over the long term.

Hino Motors’ Operational and Profitability Trends

(Source: hino-global.com)

- Hino Motors’ recent financial results demonstrate a complete performance turnaround, which shows the company faces growing challenges to maintain its business operations and generate profits.

- The fiscal year 2025 found the company losing 379.34 yen per share because earnings per share dropped from the previous year’s 29.77 yen to this figure, which resulted in a major decrease in shareholder wealth.

- The downward earnings trend receives additional support from diluted EPS, which shows the company faced major financial losses, demonstrating that its actual profits remained highly restricted even after all shares were accounted for.

- The return on equity (ROE) dropped sharply to –76.3%, compared to a strong 45.5% in the prior year. The capital efficiency of the company suffers from decreased net income, which generates negative effects on shareholder equity.

- The company achieved a return on assets (ROA) of 2.7%, which improved from –0.7%, showing that the business managed its assets more efficiently but failed to achieve strong profitability results.

- The company achieved an operational improvement through its operating margin, which increased from -0.5% to 3.4% by showing initial success in cost management and operational improvements, which worked toward recovery, although the organization still experienced financial losses.

Hino Motors Balance Sheet Dynamics

(Source: hino-global.com)

- The latest balance sheet of Hino Motors shows that the company has increased its assets while its financial stability has decreased.

- The total assets for FY 2025 reached ¥1,478,180 million, which represents a small increase from the previous fiscal year’s total of ¥1,464,375 million because the company expanded its operations and maintained its investment efforts.

- The growth of the company shows positive results, yet its net assets suffered a major decrease from ¥463,420 million to ¥251,020 million, which indicates a major loss of equity.

- The equity ratio serves as a vital financial strength indicator, which shows the company’s ability to meet its obligations, but it experienced a sharp decrease from 26.8% to 12.1%, which demonstrates that the company now depends more on its debt obligations while facing increased risks of financial instability.

- The current situation shows that the company has lost its capacity to handle financial emergencies because its balance sheet protection has diminished.

- The trend shows that net assets per share have dropped to ¥310.90, which represents a value that has decreased by almost 50% from ¥682.98, which shows that the company has destroyed most of its value for shareholders.

- The company experienced a decrease in working capital, which dropped from ¥392,049 million in FY2024 to ¥343,435 million in FY2025, because the company faced increasing challenges with its cash flow situation.

Hino Motors Cash Flow Trends

(Source: hino-global.com)

- The consolidated cash flow statement of Hino Motors shows that the company faces two opposing financial forces, which create business operational problems and depend on outside funding to maintain cash flow.

- The company showed a positive operating cash flow of ¥1,128 million for FY2025, which represents a major turnaround from its operating cash flow loss of –¥110,410 million during FY2024.

- The organization shows signs of stabilizing its main business functions because it has achieved better management of working capital and current cost control systems, which act as vital signs of upcoming operational progress.

- The company recorded negative cash flow from its investment operations, which reached –¥4,600 million, because it continued its spending on capital projects while making essential investments.

- The organization spent less money than it used to in previous years, but the company maintained its dedication to building permanent assets and revamping its operations.

- The main source of liquidity for the company comes from its cash flow, which decreased from ¥55,638 million to ¥29,738 million through its financing operations, although this decrease shows the company still depends on financial support from external sources.

- The organization shows higher financial leverage through its increased capital requirements, which creates operational risk because its cash flow needs to generate higher amounts before it can succeed.

- The organization improved its short-term liquidity position through cash and cash equivalents, which increased to ¥88,420 million from a previous amount of ¥67,733 million.

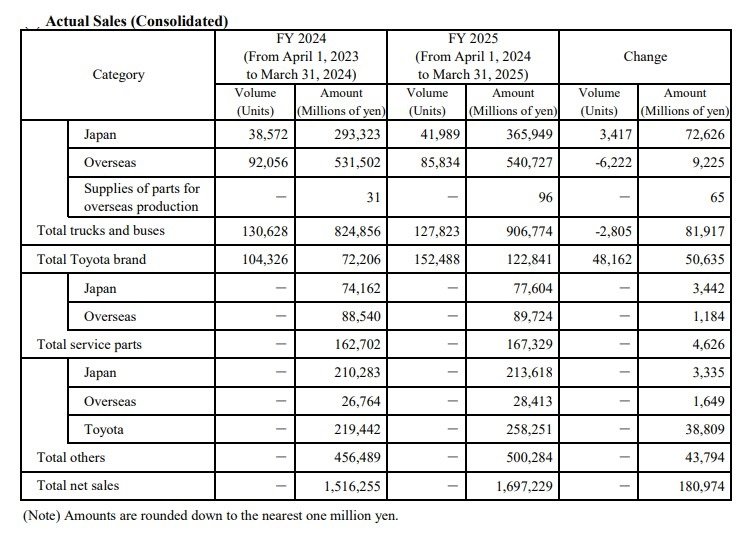

Hino Motors Sales Performance Review

(Source: hino-global.com)

- The consolidated sales data of Hino Motors shows revenue growth and changes in volume and market distribution for the period from FY2024 to FY2025.

- Total net sales reached ¥1,697,229 million, which represented an 11.9% increase of ¥180,974 million and demonstrated strong market recovery with rising demand for commercial vehicles.

- The company achieved a higher revenue of ¥81,917 million through its pricing methods and product selection, although truck and bus sales decreased by 2,805 units.

- The Japanese market showed strong performance with volume growth of 3,417 units and revenue increase of 24.8%, which demonstrated strong local demand and market resilience.

- The company experienced an overseas sales volume decline of 6,222 units, but its revenue grew by ¥9,225 million, which showed better profit margins and higher-value exports.

- The Toyota brand segment emerged as a key growth driver for the company, which achieved a revenue increase of over 70% that resulted in £122,841 million.

- The aftermarket segments, which include service parts and other products, sustained their growth through maintenance operations, which generated more than ¥48 billion in total revenue while showing how essential these revenue sources are for maintaining customer loyalty.

- Hino Motors uses value-driven growth methods to optimize profits while managing weight changes between production capacity and commercial vehicle space, which enables the company to compete in the global commercial vehicle market.

Hino Motors Outlook 2026

- Hino Motors’ forward-looking guidance for FY 2026 signifies a period of earnings normalization, albeit under sustained pressure from, driven by overseas market slowdown and yen appreciation, two critical macroeconomic headwinds impacting the commercial vehicle industry.

- The company forecasts net sales of ¥1.5 trillion, representing a decline of approximately -11.6% from FY 2025 levels, indicating weakening global demand dynamics and export competitiveness.

- Profitability is also expected to soften, with operating income projected at ¥40 billion and ordinary income at ¥35 billion, reflecting margin compression and cost pressures.

- However, a notable recovery is anticipated at the bottom line, with profit attributable to owners of parent estimated at ¥20 billion, marking a return to positive net earnings after the significant losses reported in FY 2025. This suggests that ongoing financial restructuring and cost optimization efforts are beginning to stabilize performance.

- Japan truck and bus sales are expected to be 37,000 units, while overseas sales reach 78,000 units, highlighting continued reliance on international markets despite near-term weakness.

- Additionally, Toyota brand vehicle sales are projected at 165,200 units, reinforcing strategic alignment within the broader Toyota Group ecosystem.

- On capital allocation, Hino’s dividend policy remains cautious, targeting a 30% payout ratio, yet no dividend is announced due to negative retained earnings and compliance-related losses.

- Overall, the outlook reflects a recovery phase focused on financial stability, governance rebuilding, and sustainable profitability.

ARCHION Merger Strategy

- Hino Motors’ forecast for FY 2026 predicts a period when their earnings will return to normal levels, but their operations will still face challenges from two main macroeconomic factors, which include international market downturns and Japanese yen strength.

- The company projects net sales of ¥1.5 trillion, which represents an 11.6% decrease from FY 2025 levels because of declining worldwide customer demand and decreased ability to export products.

- The company will experience lower profitability because it expects operating income to reach ¥40 billion and ordinary income to reach ¥35 billion, which results from declining profit margins and increasing operational costs.

- The bottom line will experience a major comeback because the profit, which belongs to the parent company’s owners, will reach ¥20 billion, which shows the company has regained positive net earnings after suffering large financial losses in FY 2025. This evidence shows that the company has achieved performance stability through its ongoing efforts to restructure finances and optimize costs.

- Japan expects 37,000 trucks and buses to be sold, while international markets will account for 78,000 unit sales, which demonstrates the company still depends on foreign markets despite experiencing short-term sales drops.

- The Toyota Group ecosystem will benefit from Toyota brand vehicle sales, which are expected to reach 165,200 units, according to projected sales.

- Hino maintains a conservative dividend policy, which sets a 30% payout target for capital allocation, but the company did not declare any dividend because it has negative retained earnings and compliance-related losses.

- The current outlook shows the company is entering a recovery period, which will establish financial stability together with improved governance and enduring profit generation.

Hino Motors’ Multi-Pathway Decarbonization Strategy

- Hino Motors’ decarbonization strategy represents one of the most pragmatic and diversified approaches in the global commercial vehicle industry, balancing battery electric vehicles (BEVs), hydrogen fuel cell vehicles (FCEVs), and low-carbon fuels within a single roadmap.

- Anchored by the Hino Environmental Challenge 2050, the company is targeting carbon neutrality across its entire value chain, with interim milestones under its 2030 framework—highlighting a structured, data-driven transition.

- The Blue Ribbon Z EV operates as Hino’s electric bus solution, which uses its 242 kWh battery to achieve a 360 km distance, thereby establishing Hino as a strong competitor in the electrification of public transport systems, which currently experiences worldwide double-digit expansion.

- The Hino Profia Z FCV, which operates as Japan’s first hydrogen fuel cell truck for mass production, offers 650 kilometres of driving range and requires 15 to 30 minutes for refuelling to achieve diesel-equivalent operational efficiency while producing zero emissions.

- The vehicle achieves its operational capability through its 25-ton gross vehicle weight and 11.6-ton cargo weight, which allows it to operate without compromising environmental impacts or operational efficiency.

- The partnership between Hino and Toyota Motor Corporation establishes Hino as a key player in the hydrogen ecosystem because Japan plans to increase its hydrogen production capacity from 3 million tonnes in 2030 to 20 million tonnes by 2050.

- The hydrogen truck market will expand from its current valuation of USD 4.3 billion in 2024 to reach a value of USD 15.1 billion by 2030, with a compound annual growth rate exceeding 28%, which establishes FCEVs as a rapidly expanding business sector.

- Hino has already achieved a 60% reduction in factory CO₂ emissions through its sustainability operations, which have now surpassed its 2030 target of 40% reduction.

- Hino’s investments in battery electric vehicles acquire additional urgency because the global electric truck market will grow to USD 32.1 billion by 2032 with a 29.5% compound annual growth rate.

- Hino’s decarbonization strategy for multiple pathways leads the company to maintain its market position through battery electric vehicle expansion, hydrogen technology development, and reduction of emissions across product life cycles.

Conclusion

The current recovery process of Hino Motors shows complex challenges because the company achieves high revenue growth yet encounters major issues with its profitability. The company shows operational enhancements that reduce expenses; however, its financial position remains weak because it incurs substantial losses while its net assets decline. The company will achieve its 2026 projection through its current restructuring activities and its new business alliance with ARCHION.

Hino establishes a strong position for future market changes through its multiple decarbonization initiatives, which include electric and hydrogen technology development. The company needs to achieve three objectives before its recovery can proceed, which require it to attain profitability,d build financial strength, and manage its worldwide transformation during changing market conditions and new regulatory requirements.

FAQ

Hino recorded a ¥21775B loss, which resulted from restructuring expenses, regulatory compliance problems and special one-time costs.

The company shows signs of recovery because its operating income became positive and its cash flow showed improvement.

The revenue will drop to approximately ¥1.5 trillion because global demand has decreased.

The joint venture between Hino and Mitsubishi Fuso aims to create a business that will generate more than €16B in revenue while achieving operational cost savings.

Hino focuses its decarbonization efforts on developing electric vehicles, hydrogen fuel cells and low-carbon fuels.