Introduction

Just Eat Statistics: The act of ordering food has become a multi-billion-dollar industry operating across the world. People used digital meal ordering as a simple way to order food. Still, now this service has become a powerful economic driver that transforms how consumers buy products throughout the globe. Just Eat Takeaway.com functions as the main driver of this transformation because it operates a worldwide food delivery service that connects restaurants with millions of customers. Just Eat must make a critical decision about its future because its current business path faces disruption from market consolidation, new business strategies, changing customer needs, and its objectives for making profits.

The article investigates current Just Eat statistics through which it assesses the performance by analyzing revenue, transaction amounts, customer data, and corporate developments.

Editor’s Choice

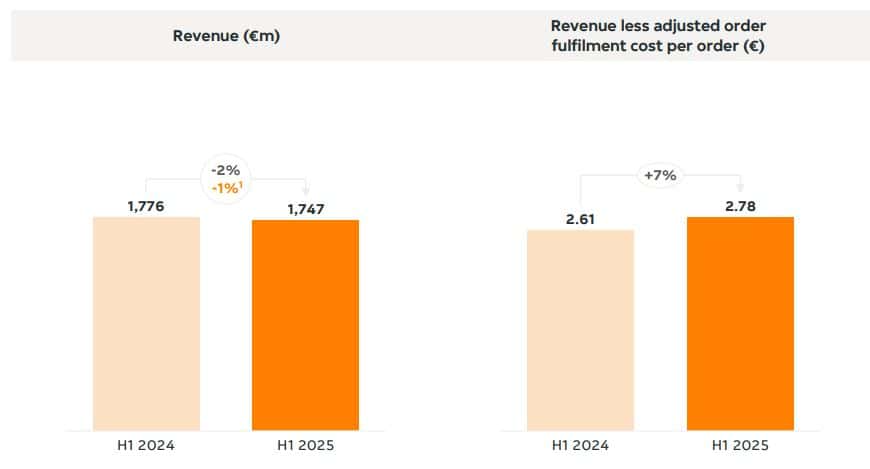

- Just Eat H1 2025 revenue declined 2% YoY to €1,747m from €1,776m.

- Revenue less adjusted fulfilment cost per order rose 7% to €2.78, reflecting stronger unit economics.

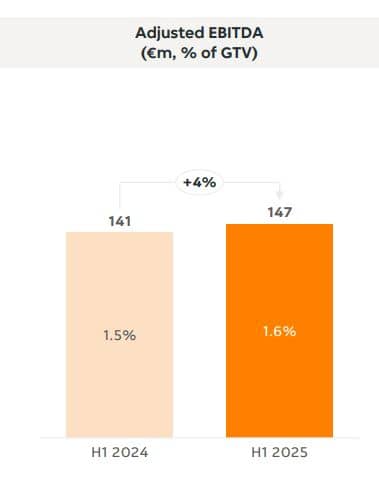

- The adjusted EBITDA experienced a year-on-year growth of 4%, which reached €147 million, while the margin expanded to 1.6%.

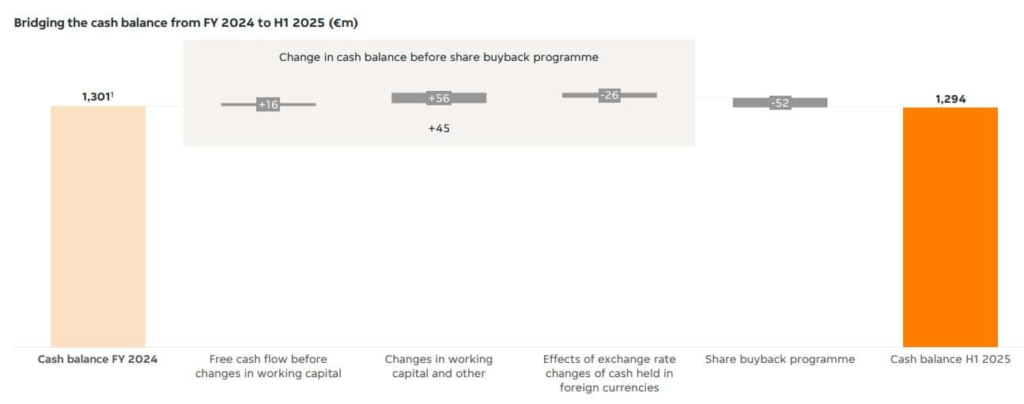

- The free cash flow before working capital reached €16 million, which showed that the company generated cash at a stable rate.

- The company maintained a strong cash balance of €1,294 million even after spending €52 million on share buybacks.

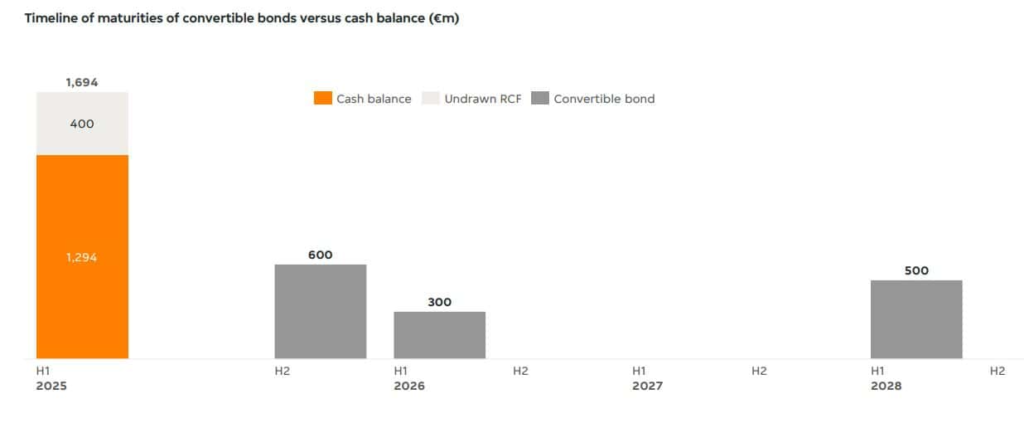

- The company had total available liquidity of €1,694 million, which enabled it to handle upcoming debt obligations at a ratio of approximately 1.9 times.

- The number of partners expanded to 362,000 during the year, which represents an increase from 342,000 partners in the previous year, and this development has improved the density of the marketplace.

- Active consumers decreased to 60 million from 62 million, which shows that demand has decreased.

- The percentage of returning active consumers remained constant at 70%, which shows that customers maintained their loyalty to the brand.

- The average monthly order frequency decreased slightly from 2.7 orders to 2.6 orders.

- The total number of orders decreased to 308 million in H1 2025, which represents a 6.7% year-on-year decline.

- Group GTV maintained its value at €9.4 billion because the company achieved strong pricing results.

- The Average Transaction Value increased by 6.9% year on year, reaching €30.37, which proves that the company has the ability to set its prices.

- UK & Ireland EBITDA surged 32% YoY to €121m, driving profitability gains.

Just Eat Revenue

(Source: q4cdn.com)

- Just Eat’s current operational results demonstrate the company is dealing with a revenue decline while achieving greater operational efficiency.

- The company recorded a revenue decrease from €1,776m in H1 2024 to €1,747m in H1 2025, which resulted in a 2% annual decline.

- The order volume decrease resulted from two factors, which included increased competition and decreased customer demand.

- Profitability metrics display strong performance results. The revenue increase from adjusted order fulfillment cost per order reached 7% growth, which brought the total to €2.78 from €2.61.

- The company’s unit economics improvement originates from better logistics operations combined with enhanced commission structures and increased pricing discipline.

- Just Eat Takeaway.com appears to be prioritizing margin quality over aggressive growth.

- The company needs to track revenue decline, which now shows better progress as per-order contribution increases.

- Just Eat’s statistics demonstrate a movement toward sustainable profitability, which the company achieves through operational expansion instead of pursuing volume growth.

Just Eat Adjusted EBITDA

(Source: q4cdn.com)

- Just Eat shows profitable business growth during the initial six months of 2025.

- The company experienced a 4% annual increase in adjusted EBITDA, which grew from 141 in H1 2024 to 147 in H1 2025.

- Food delivery companies face competitive challenges, but their operational efficiency improves through margin growth from 1.5% to 1.6%.

- The 10 basis-point increase demonstrates that the company achieves savings through effective management of expenses and operational growth.

- The Just Eat data indicates that the company maintains strong earnings performance while its core marketplace business model develops further.

- Although the company experiences slow growth, its positive EBITDA development builds trust in its ability to maintain profit margins while establishing a cautiously positive outlook for the future.

Just Eat Cash Flow

(Source: q4cdn.com)

- Just Eat’s cash bridge reflects disciplined capital management despite shareholder returns.

- The company started FY 2024 with cash reserves of €1,301m.

- Operationally, the company produced €16m in free cash flow before accounting for working capital variations and other financial factors, which contributed an additional €56m.

- The foreign exchange impacts resulted in a cash reduction of €26 million.

- The net cash increased by €45 million before the share buyback program began.

- The company spent €52 million on share buybacks, which decreased its available cash until the H1 2025 balance reached €1,294 million.

- The Just Eat data shows that the company maintains strong cash flow because it has over €1.2 billion in stable liquidity, and it maintains equal weight on all capital spending areas, which supports its overall financial strategy.

Just Eat Debt Maturity Profile And Liquidity Coverage

(Source: q4cdn.com)

- Just Eat established a liquidity buffer that protects its financial needs for upcoming convertible bond repayments.

- The company possesses €1,294 million in cash and €400 million in unused RCF capacity, which together create a total liquidity reserve of €1,694 million as of H1 2025.

- Just Eat covers immediate financial obligations, which include a €600 million debt repayment scheduled for H2 2025 and a €300 million debt payment scheduled for H1 2026.

- The company must repay €500 million in H1 2028, while 2027 lacks any significant debt repayments, which gives the company time to organize its refinancing and repayment strategies.

- The current liquidity position of the organization enables it to cover the upcoming maturity needs of €900 million because it provides almost two times more financial resources.

- The treasury management of Just Eat shows responsible practices because its debt repayment schedule reduces the danger of needing to refinance.

- The company’s strong cash position generates multiple options for credit, which include either repaying debts early, refinancing at better rates, or investing in business growth, which builds trust in Just Eat’s future liquidity sustainability.

Platform Expansion Amid Moderating Consumer Activity

(Source: cloudfront.net)

- Just Eat’s current statistics show that the platform has successfully expanded its supplier network, yet it faces challenges because consumer demand is currently decreasing.

- The partner numbers reached 362000 on June 30, 2025, which represented a 20000 partner increase from the 342000 partners active in June 2024 and the 327000 partners active in December 2023.

- The growth of the service area delivers two benefits for the company: it strengthens existing network operations and establishes better competitive advantages.

- The active user count dropped to 60 million in June 2025 after reaching 62 million the previous year and 63 million in December 2023.

- The rate of returning active users stayed constant at 70%, which represents a small decrease from the 71% historical rate.

- The Just Eat statistics show that the company will focus its efforts on developing a better supply system while it keeps its current user engagement metrics.

Just Eat Total Orders

(Source: cloudfront.net)

- The total dropped to 308 million in H1 2025 after reaching 330 million in H1 2024, which resulted in a decrease of 6.7% compared to the previous year.

- The wider contraction started with 689 million in 2023 and ended with 653 million in 2024, which shows that multiple periods have achieved standardization.

- Europe achieved 149 million orders in H1 2025, while the previous year recorded 155 million orders, which shows a gradual decrease in business activity.

- UK & Ireland generated 114 million orders, down from 120 million, showing that customers visited the main market less often because they spent less time at shops.

- The most substantial drop originated from the Rest of World, where orders decreased from 55 million to 46 million, which showed the effects of portfolio streamlining and planned market withdrawals.

Just Eat Total GTV

(Source: q4cdn.com)

- The full-year period showed GTV growth when it moved from €18.6 billion in 2023 to €18.9 billion in 2024, which confirmed the company’s capacity to maintain its long-term value.

- The H1 2025 financial results showed Europe generating €4.6 billion, which represented an increase from €4.5 billion.

- The UK and Ireland market Expansion resulted in a revenue increase to €3.6 billion from €3.4 billion, which showed that customers were making larger purchases than before.

- The Rest of the world market showed a revenue decrease to €1.2 billion because of market exits and strategic consolidation.

- The Just Eat statistics show that analysts believe the company needs to adjust its operational priorities toward higher profit margins.

- The business demonstrates operational maturity because its GTV stays at the same level while order numbers decrease, and customers maintain their purchasing behavior through established pricing methods.

- The company developed its operational practices to achieve stable financial results, which focus on growing profits instead of attempting to achieve high sales volumes.

Just Eat Total ATV

(Source: cloudfront.net)

- The Just Eat statistics demonstrate a significant increase in their ability to set prices and their customers’ spending behavior.

- The Group Average Transaction Value (ATV) for H1 2025 reached €30.37, which shows a 6.9% increase from the H1 2024 value of €28.42.

- The value increased from €27.06 in 2023 to €28.88 in 2024, which demonstrates that the system is developing better permanent results than temporary changes.

- The ATV in Europe increased from €28.98 to €30.72, while the UK & Ireland experienced the largest increase to €31.48 from €28.55, which demonstrates successful pricing methods and better customer spending.

- The Rest of World region maintained its price range at €26.47, which represents a decrease from the previous year’s price of €26.55 because customers in that area tend to be more price-conscious.

- The Just Eat statistics reveal to analysts that the company has changed its business approach to prioritize value creation.

- The company achieved better revenue results and profit margins through its operational efficiency after customers started to spend more per order, even when order volumes decreased.

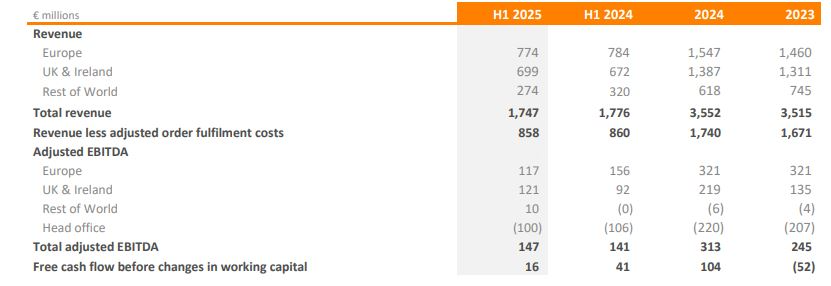

Just Eat Geographical Financial Performance

(Source: cloudfront.net)

- The data from Just Eat statistics show that the company is achieving better profits while experiencing slight revenue losses.

- H1 2025 total revenue reached €1,747 million, which fell short ofH1 2024 total revenue of €1,776 million, showing a 1.6% year-on-year decrease.

- The core markets maintained their stability through Europe revenue of €774 million and UK & Ireland revenue of €699 million.

- The Rest of the world revenue decreased from €320 m illion to €274 million, which showed the company chose to reduce its portfolio.

- Total adjusted EBITDA saw a positive development because it reached €147 million from €141 million, which was backed by higher EBITDA growth from UK & Ireland operations that reached €121 million with a 32% year-on-year increase.

- European operations achieved EBITDA of €117 million while the Head Office experienced a slight decrease in financial losses.

- The company maintained its revenue at €858 million, which eliminated expenses for delivery services through effective management of essential business functions.

- The Just Eat statistics demonstrate that the company has implemented strategies to enhance its profit margins through cost management, which will generate sustainable growth for the business rather than pursuing aggressive revenue growth.

Conclusion

Just Eat Statistics: Just Eat reaches a major turning point in its business operations as of 2025. The platform maintains its worldwide delivery service presence according to its statistical data. The company experiences slower growth now than during the pandemic, but its strategic business changes show that it plans to achieve permanent success through its new operation channels, its focus on making profits, and its acquisition by Prosus.

The company’s 2025 statistics show its current situation to investors, users, and industry observers because they show the company’s upcoming developments in the food delivery industry.

FAQ

Just Eat Takeaway.com reported total revenue of €1,747 million during the first half of 2025, which represented a 2% decrease from the previous year’s total of €1,776 million.

The Adjusted EBITDA for the company reached €147 million, which showed a 4% increase over the previous year’s total of €141 million during H1 2024.

The total orders for the company decreased to 308 million, which represented a 6.7% decline compared to the 330 million orders received in H1 2024.

The total GTV for the company remained at €9.4 billion during the first half of 2025, which matched the previous year’s GTV from H1 2024.

The platform reached 60 million active consumers in June 2025, which represented a slight decline from its previous count of 62 million active users one year earlier.

The partner numbers increased to 362000, which represented growth from 342000 partners during June 2024.