Introduction

Koss Statistics: The Koss Corporation operates as one of the oldest American headphone manufacturers, having existed since 1953 to deliver high-fidelity personal audio products in the competitive consumer electronics market, alongside major companies such as Apple, Bose, Sony, and JBL. Koss maintains its ability to adapt and grow its sales channels during worldwide market changes because of its strength, which exists beyond its smaller size when compared to major players in the industry.

The company achieved its success during 2025 because it managed to handle economic challenges, which included tariff restrictions and changes in customer behavior, according to its financial results, which showed revenue growth and operational efficiency.

The article presents essential Koss Statistics and its financial data from 2025, which gives investors, revenue and technology fans a complete understanding of its financial situation.

Editor’s Choice

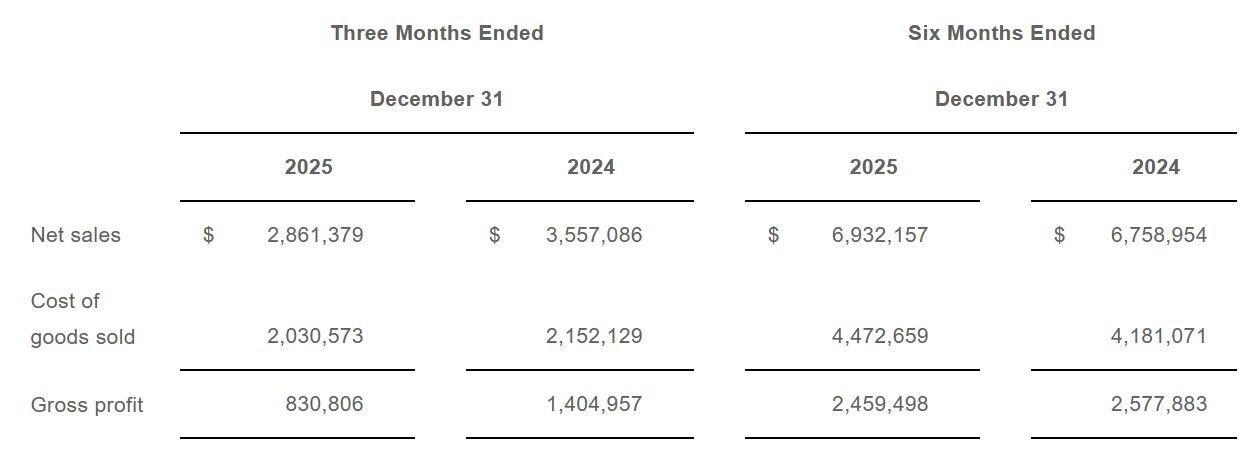

- Koss Quarterly net sales declined 19.6% YoY to USD 2.86 million in Q2 FY2025.

- Koss Quarterly gross profit dropped almost 41% from the previous year to USD 830806, which showed reduced profit margins.

- The six-month period experienced a 2.6% increase in net sales, which reached USD 6.93 million, while the market showed signs of recovery.

- The fiscal year 2025 revenue reached 12.62 million after a 2.93% increase, which followed multiple years of revenue decline.

- The revenue for fiscal year 2023 experienced a 26.01% decline, which demonstrates how the company faced financial instability during that time period.

- The company spent USD 7.67 million on operating expenses, which accounted for a significant proportion of its total revenue during the twelve months leading up to this point.

- The company recorded its operating income at –3.02 million for the trailing twelve months, which showed continuous financial losses.

- The company achieved a net loss of 0.87 million for fiscal year 2025, which represented a significant reduction from its previous year’s net loss of 9.59 million.

- The gross margin for fiscal year 2025 increased by 370 basis points because it reached 37.8% from 34.1% the previous year.

- Koss Total debt remained low at USD 2.54 million, with a D/E ratio of 0.08.

- Koss maintained a strong net cash position of approximately USD 13.95 million.

- The operating cash flow for fiscal year 2025 showed a negative result of USD (214,908).

- Direct-to-Consumer sales grew 16.5% in FY2025 and accounted for up to 22.5% of sales in Q1 FY2026.

Koss Gross Profit

(Source: koss.com)

- According to the company report, the most recent Koss statistics show that margin compression has occurred despite the company achieving strong revenue growth.

- The three-month period that ended on December 31, 2025, saw net sales decrease to USD 2.86 million from the previous year’s total of USD 3.56 million, which resulted in a 19.6% decline when compared to the previous year.

- The gross profit dropped to USD 830,806 from last year’s total of USD 1.40 million, which resulted in a nearly 41% decrease.

- The company experienced increased cost pressures because it could not reduce costs more than it achieved through its cost-of-goods-sold reduction.

- Net sales increased to USD 6.93 million in 2025, which represents a 2.6% increase from the previous year’s total of USD 6.76 million.

- The company reported gross profit of USD 2.46 million, which fell short of last year’s USD 2.58 million total because the company experienced a minor margin decline.

- The Koss statistics show that the company will experience temporary quarterly declines while the main business operations will maintain their half-year performance.

- Koss will depend on its ability to manage costs effectively and its ability to restore customer demand when evaluating future business performance.

Koss Revenue

(Source: simplywall.st)

- According to SimplyWall, the latest Koss statistics show a minor recovery period, which follows three years of sales decline.

- The revenue for the twelve-month period that ended on December 31 2025, reached USD 12.8 million, which represents a 4.13% annual growth rate.

- The fiscal year 2025 ended with revenue of USD 12.62 million, which represents a 2.93% increase from the previous year’s total of USD 12.27 million.

- The historical data reveal a pattern of financial performance that exhibits greater fluctuations than present-day assessments indicate.

- A 6.37% revenue drop during fiscal year 2024 and a 26.01% revenue decline during fiscal year 2023, which followed a 9.42% drop in fiscal year 2022.

- The company reached its highest revenue point of USD 19.55 million during fiscal year 2021 before experiencing a significant revenue decline.

- Koss statistics will continue to deliver positive growth results through product innovation, distribution expansion and enhanced brand positioning according to future business prospects.

Koss Operating Income

(Source: simplywall.st)

- Koss reports continuous operating losses because its operating expenses exceed its revenue growth, according to the newest statistics.

- The operating expenses for the twelve-month period that ended on December 31 2025, reached USD 7.67 million, which shows an increase from USD 7.51 million in FY 2025 and USD 7.0 million in FY 2024.

- The company incurs its major cost through Selling General Administrative SG A expenses, which reached USD 7.46 million TTM, while the company earns between USD 12 million and USD 13 million in yearly revenue.

- Companies spend their Research and Development budgets at a low level because they spend only USD 0.21 million, which shows their Research and Development activities need more funding to match their industry competitors.

- The operating income shows a current value of -3.02 million TTM, which represents a slight progress from the -2.74 million value in FY 2023 but remains in negative territory.

Koss Debt Vs. Equity Structure

(Source: dcfmodeling.com)

- According to DCFmodeling, the current Koss financial report shows that the company uses a highly cautious balance sheet approach, which especially applies to the consumer electronics industry that typically uses debt to drive business expansion.

- Total debt of USD 2.54 million as of June 30 2025, while its net cash position stood at approximately USD 13.95 million.

- The company possesses cash and short-term investments that surpass total debt obligations by more than five times, which establishes a strong liquidity reserve.

- The primary metric measures the Debt-to-Equity (D/E) ratio with a value of 0.08. Koss operates with a debt ratio of 8 cents for each dollar of equity, which stands lower than the industry standard debt ratio of 50 cents for each dollar of equity.

- The gap between Koss and its competitors shows substantial importance because it enables Koss to operate with almost no debt, while its competitors experience high expenses from debt and interest costs, together with their exposure to fluctuating interest rates.

- Koss maintained a USD 5 million secured revolving credit facility with Town Bank, which showed no outstanding loans on June 30, 2025.

- The organization shows low debt because its operational expenses account for most of its debt obligation instead of using bank financing. Koss maintains operational access to funds because it does not need to spend its available financial resources.

- The organization uses retained capital to finance its day-to-day activities, while its Direct-to-Consumer (DTC) segment operations show a 16.5% growth rate for FY2025, which marks a significant achievement in a difficult retail market.

- The use of leverage increases business expansion profits but creates a greater risk of losses during periods when consumer demand decreases, and consumers react to interest rate changes.

- Koss has established its business model to maintain low borrowing expenses while maintaining its ability to adapt financially.

Koss Cash Flow Activity

(Source: dcfmodeling.com)

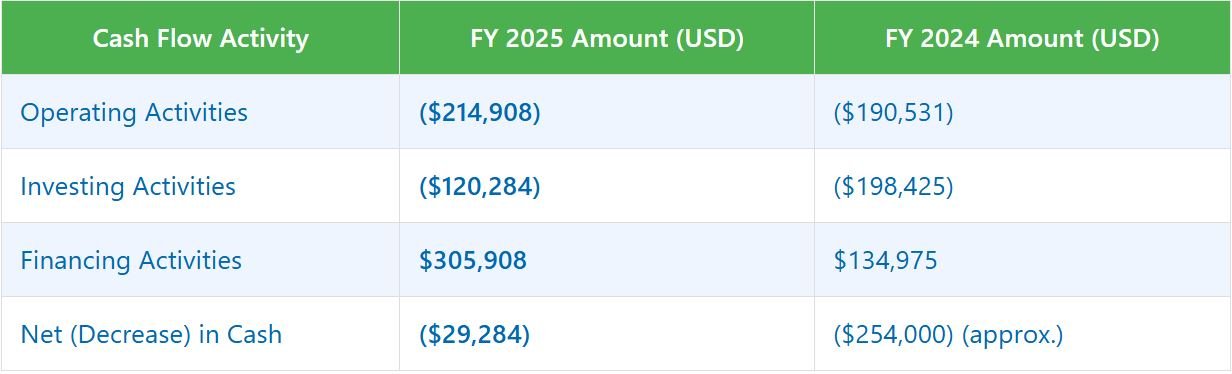

- Koss experienced negative cash flow from operations in FY2025, with a CFO of USD (214,908), because core headphone sales could not generate enough revenue to cover operating costs.

- The company experiences recurring negative CFO, which results in financial capacity declines because the situation needs a solution that has not yet occurred.

- Koss spent USD 120284 on investing activities because of capital expenditures, which represent standard costs needed to keep their business operations active.

- The business spent approximately USD 335192 through operating and investing activities while receiving USD 305908 from financing activities, which created a small cash reduction of USD (29284) for the fiscal year.

- The operations should focus primarily on monitoring sustainable operating cash flow recovery because it represents the most essential metric for assessment.

- Koss needs to establish stable operational cash flow through its future statistics because this will strengthen its ability to maintain a strong balance sheet.

Koss Valuation

(Source: dcfmodeling.com)

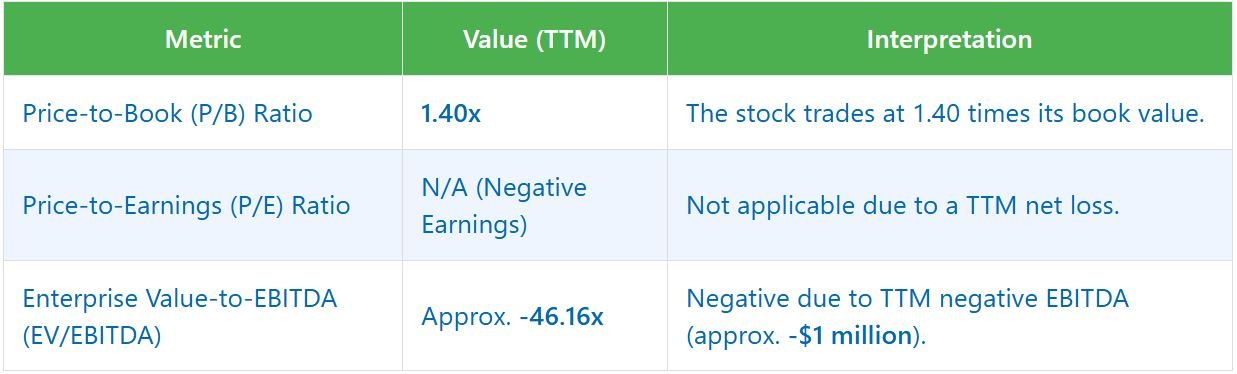

- Koss’s most recent financial data indicate that the company needs special evaluation methods because traditional earnings-based metrics fail to assess it properly.

- Koss experienced its first fiscal year net loss of about USD 0.87 million, which resulted in a negative Price-to-Earnings (P/E) ratio that became unusable.

- Valuation analysis needs to shift from profitability assessment to balance sheet and asset-based assessment because profits are irregular.

- The Price-to-Book (P/B) ratio at 1.40x (TTM, November 2025) serves as the most important financial indicator. The stock trades at 1.4 times its net asset value, which shows that the market holds moderate confidence in the stock without showing any signs of speculative overpricing.

- The P/B ratio between 1.0 and 1.5 that exists for small-cap consumer electronics companies shows that investors value stability more than they expect aggressive growth.

- The current Enterprise Value-to-EBITDA (EV/EBITDA) ratio stands at approximately – 46.16x because the company reports negative EBITDA of about -USD 1 million.

- The negative multiple shows operating difficulties that prevent any useful peer comparisons about value.

- The investment thesis focuses on Koss’s entire statistical data because it depends on cash reserves and book value support rather than earnings growth.

- Koss needs to show permanent profitability through future statistics before its valuation through asset-based multiple expansion can begin.

Koss Share Price Performance And Market Sentiment

- The statistics from Koss show that investors remain cautious about the company, although its operations show some signs of progress.

- The stock closed at USD 4.66 on November 21, 2025, which represents a 33.67% decline from its value one year ago.

- The stock trades between USD 4.00 and USD 8.59, which shows that the asset experiences both significant price fluctuations and an inability to maintain its value during upward price movements.

- The company achieved a small positive earnings per share of USD 0.03 during Q1 2026, but its overall earnings performance shows ongoing volatility.

- The company pays no dividend (0.00% yield), which means that investors can only earn returns through increases in the company’s stock value.

- A market capitalization of approximately USD 45.01 million and an enterprise value of USD 29.93 million, which means that the discount reflects its solid net cash position that previous Koss statistics have demonstrated.

- The stock currently receives a “Hold” rating from analysts who believe its value remains unchanged because there are no immediate drivers for price movement.

- Koss needs to show consistent EBITDA growth through its upcoming financial reports to regain investor trust and obtain better market valuation.

Koss Growth Expansion Outlook

- Koss statistics show that the company is moving from its stabilization phase into a stage of controlled expansion.

- Koss’s non-high-growth technology market position leads to its current benefits from switching to high-margin business operation channels.

- The company achieved USD 12.62 million in revenue for FY2025, which represents a 2.1% annual growth rate, because the business showed better profitability results.

- It reduced its net loss to USD 0.87 million from USD 9.59 million in the previous year, while it achieved a gross margin improvement from 34.1% to 37.8% through better sales mix performance.

- The Direct-to-Consumer (DTC) channel is the standout performer. DTC revenue grew 16.5% in FY2025, and in Q1 FY2026, it accounted for 22.5% of total sales, reflecting structural margin enhancement.

- Export markets further strengthened diversification, with international sales rising 48% year-over-year, including a 67% increase across key European distributors.

- The geographic distribution of our business operations allows us to decrease our dependence on domestic retail partners.

- Product innovation is also translating into commercial traction, particularly in Europe, where new releases fueled a 100% sales increase among top distributors in Q4 FY2025.

- The first quarter of fiscal year 2026 saw revenue growth of 27.1% compared to the previous year, reaching USD 4.7 million, which resulted in net income of USD 243,729, that showed significant improvement.

Koss Risk Factors

- Koss Risk Factors Koss statistics show that operational risk remains high despite the fact that the balance sheet shows stability with net cash close to USD 14 million. The core concern lies not in liquidity, but in structural exposure.

- The total revenue achieved USD 12.62 million in fiscal year 2025 because two major distributors brought approximately 50% of total sales, which resulted in important customer concentration danger.

- The Koss company depends on contract manufacturing in China, which creates tariff risk through potential 145% import duties on products made in China.

- The fiscal year 2025 domestic sales experienced an 8.4% decrease because of distributor inventory corrections and decreased demand for educational products.

- The company spent USD 0.21 million on research and development during the past twelve months, which represents only a small portion of what its larger competitors spend, which restricts its capacity to establish distinct market advantages.

- The net loss reduced to USD 0.87 million, but its operating costs continued to be high at USD 7.51 million, which resulted in decreased profit margins.

- The broader Koss statistics reveal some factors that help reduce the negative impact of existing conditions.

- The Direct-to-Consumer sales channel experienced a 16.5% sales increase during FY2025, which contributed around 19% of total revenue while domestic market challenges continued to impact the business.

- Koss must demonstrate diverse customer base expansion, effective tariff risk management and increased research funding for research development to maintain its competitive advantage during the upcoming years.

Conclusion

The Koss Corporation achieved moderate revenue growth during 2025 while demonstrating strategic resilience against major competitors who controlled the worldwide market. The company achieved operational progress through direct-to-consumer and international export segments and decreased employee productivity, which resulted in smaller net losses throughout the year. Koss has transformed its business operations through digital strategy initiatives and multiple distribution methods, and enhanced expense management systems, which enable it to handle market pressures from tariffs and changing customer needs.

The financial reports, which include quarterly and annual records, show a stable business position that offers future growth opportunities through sustainable market development instead of rapid expansion.

FAQ

The company generated USD 12.62 million in revenue, which represents a 2.1% increase

from the previous year.

The approximate loss amounted to USD 0.87 million.

The company maintains a 0.08 debt-to-equity ratio, which shows extremely low debt usage.

The company holds net cash reserves that are approximately USD 13.95 million.

The company achieved a gross margin of 37.8%, which increased from 34.1% in FY2024.

The stock price dropped by 33.67% and reached USD 4.66 at closing.

The Direct-to-Consumer segment experienced a 16.5% growth rate during FY2025.