Introduction

Rivian Statistics: Rivian Automotive has become one of the most closely monitored electric vehicle companies in the world, while it competes against established market leaders and tries to secure funding for its expansion plans. The period between 2025 and 2026 marks a transitional phase for Rivian that shows its operational capacity through increasing profit indicators and variable vehicle shipment numbers, and its rapid growth in software-based revenue streams. The company achieved its first annual gross profit in 2025, but still faces major financial losses, along with difficulties in attracting customers to its premium electric vehicle products.

This article presents a detailed research-based statistical evaluation of Rivian’s financial performance, along with production patterns and future predictions, which use important numeric data and revenue information.

Editor’s Choice

- Rivian Automotive’s total revenue declined ~25.8% YoY, from USD 1.734B (Dec 2024 peak) to USD 1.286B by Dec 2025.

- The automotive revenue range shows demand changes with annual revenues between USD 922 million and USD 1.52 billion.

- The software and services revenue increased by 108.9% from USD 214 million to USD 447 million.

- The total software revenue for 2025 reached USD 1.56 billion, which shows a 222% growth compared to the previous year.

- The company achieved its first positive gross profit with USD 144 million in 2025 after experiencing a USD 1.2 billion loss during 2024.

- The gross margin decreased to -16% during June 2025 but later improved to 9% by the end of the year.

- The company achieved a revenue cost reduction of 25.4%, which brought expenses down to USD 1.166 billion through achieving partial expenditure savings.

- The adjusted EBITDA showed negative results, which reached a low point of -USD 667 million before showing improvements to -USD 465 million.

- The company experienced a 21.2% increase in operating expenses, which reached its highest point at USD 1.007 billion.

- The company spends USD 453 million on research and development, which demonstrates its commitment to developing new products.

- The company maintains cash reserves of USD 6.08 billion, which provide financial security despite a 21% decrease in cash during the period.

- The company delivered 42,247 vehicles in 2025, which represents a 15.7% decrease compared to the previous year.

- 2026 delivery guidance is 62,000–67,000 units, implying ~47–59% growth.

- The R2 platform is expected to add 20,000–25,000 units to 2026 production.

- Loss per vehicle is projected to decline from ~USD 47,000 (2025) to ~USD 30,000 (2026), a 36% improvement.

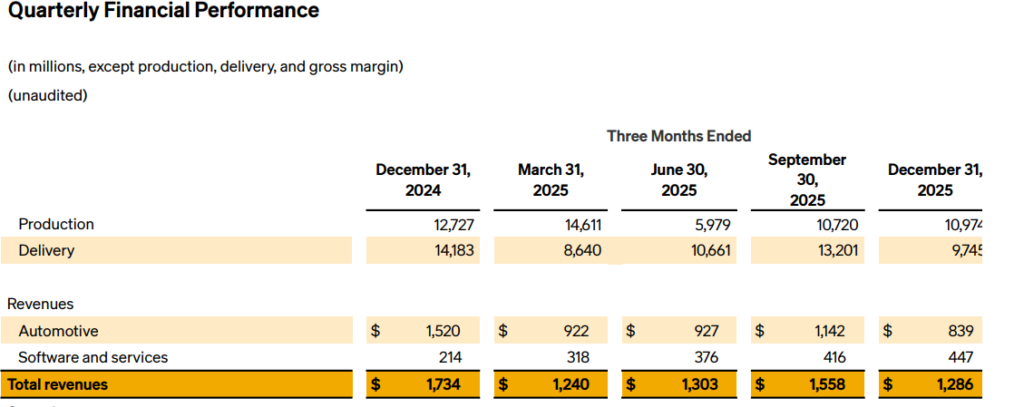

Rivian Total Revenue

(Source: rivian.com)

- The financial performance of Rivian from 2024 to 2025 shows both positive and negative aspects, which provide valuable insights.

- The data displays irregularities in production and delivery operations, which reached their highest point of 14,611 units in March 2025 before experiencing a steep decline to 5,979 units in June, which represents a 59.1% quarterly decrease, and then the output stabilized around 10.7K units.

- Deliveries, which serve as the main source of revenue, show inconsistent patterns because they decreased from 14,183 units in December 2024 to 8,640 units in March 2025, which represents a 39.1% decrease, and then they increased to 13,201 units in September, which shows a 52.8% growth.

- The revenue distribution shows Automotive revenue as the primary source of income, which experiences major revenue changes between USD 922M and USD 1.52B.

- December 2025 reports USD 839M because it shows a 45% decrease from December 2024, which indicates that demand has returned to normal or that pricing pressures exist.

- Software and Services revenue shows consistent development because it increased from USD 214M to USD 447M, which represents a 108.9% growth for Rivian’s business strategy that focuses on building high-profit recurring income sources.

- The total revenue patterns support this story because the revenue reached USD 1.734B in December 2024 before dropping to USD 1.240B in March 2025, which then increased to USD 1.558B in September before concluding at USD 1.286B for the year. The pattern displays cyclical expansion, which results in an annual reduction of 25.8%.

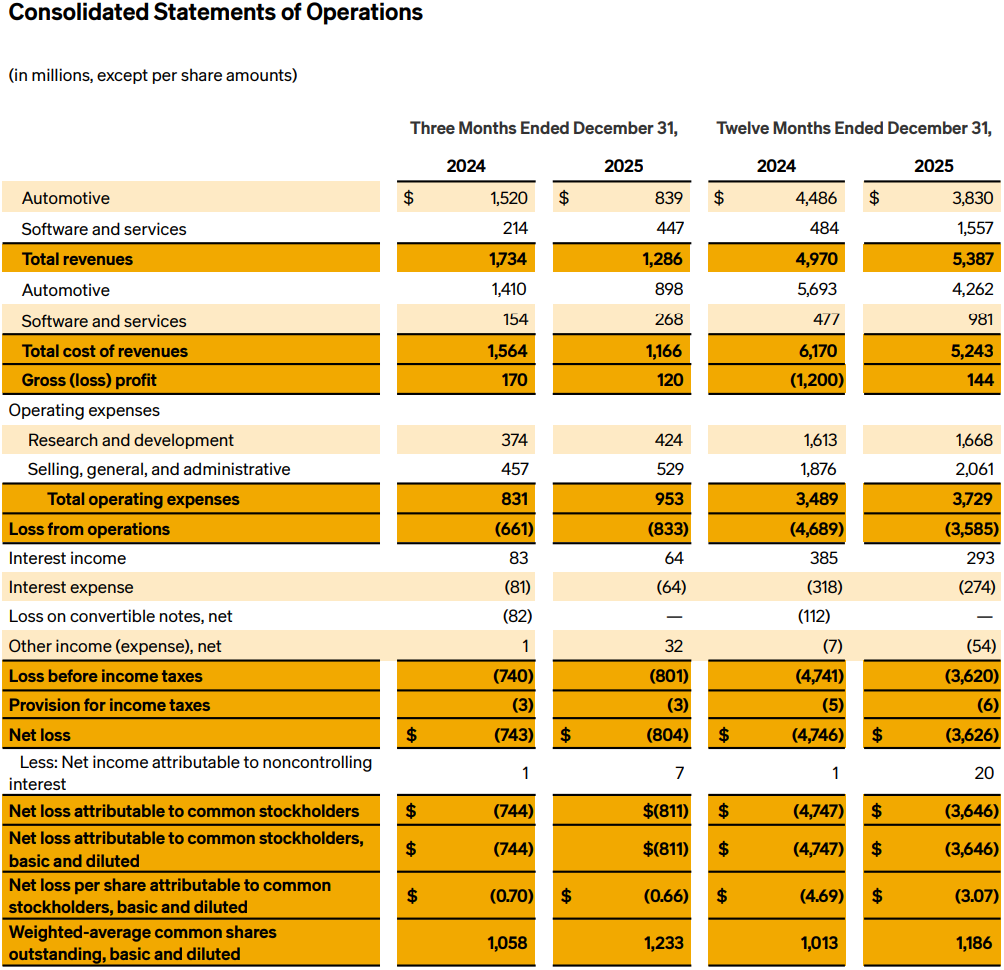

Rivian’s Cost Structure and Profitability Trends

(Source: rivian.com)

- Rivian encounters difficulties in achieving profitability while expanding its operational capabilities.

- The company incurs high costs for its produced goods, which reached their highest point of USD 1.564B in December 2024 and then declined to USD 1.166B in December 2025, showing a reduction of 25.4%.

- The revenue decrease led to cost savings, which resulted in a revenue decline that caused the company to suffer financial losses.

- The company showed extreme fluctuations in gross profit, which rose to USD 206M in March 2025 before dropping to −USD 206M in June, resulting in a negative gross margin of −16%, which indicates serious problems with unit economics.

- The company achieved recovery during September and December through its 2% and 9% margin performance, yet its overall financial performance remained unstable.

- The company experiences consistent budget growth, which causes its total operating expenses to rise from USD 831M to a maximum of USD 1.007B before decreasing.

- The company invests USD 453M in research and development, which demonstrates Rivian’s commitment to developing new technologies and advancing its electric vehicle market position, while SG&A costs stay at high levels because the company needs to manage operational growth.

- The company reports substantial negative adjusted EBITDA, which reaches its lowest point of −USD 667M in June before showing a 30.3% recovery to −USD 465M by the end of the year.

- The company demonstrates a strong liquidity position, which shows through its cash holdings of USD 6.08B, despite experiencing a cash reduction of 21%.

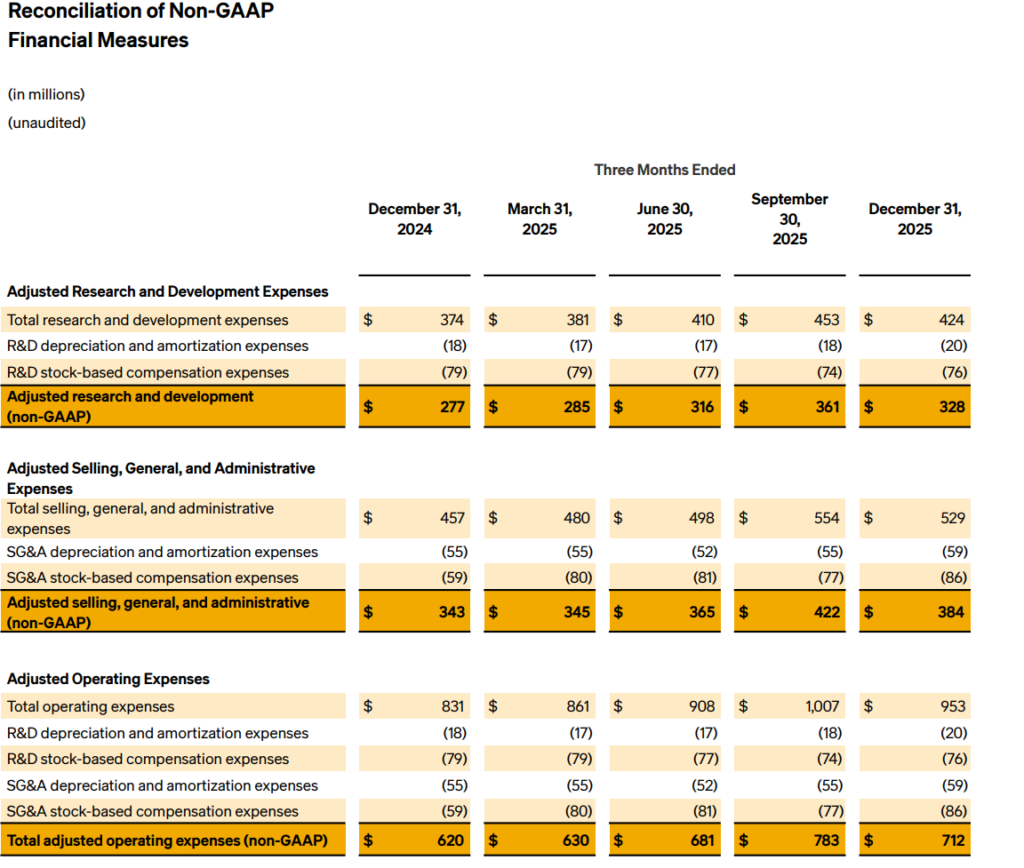

Rivian’s R&D, SG&A Efficiency, and Cost Optimization Trends

(Source: rivian.com)

- Rivian engages in a systematic process that requires substantial financial resources to achieve its goals of expanding operations and establishing itself as a leader in innovative solutions.

- The company’s adjusted R&D expenses (non-GAAP) trend upward from USD 277M in December 2024 to a peak of USD 361M in September 2025 (+30.3%), before moderating to USD 328M by year-end.

- The company maintains its research and development expenses because it views these expenses as essential for developing electric vehicle technology and platform improvements and software development, which constitute the major revenue growth drivers in the market for electric vehicles.

- The adjustment of SG&A expenses shows an increase from USD 343M to USD 422M, which represents a 23% increase that results from the company expanding its business operations, developing new sales channels, and increasing administrative expenses.

- The company demonstrates growth through this situation, which shows that its operational efficiency remains unproductive because expenses grow faster than its sales revenue reaches stable levels during specific periods.

- The total adjusted operating expenses non-GAAP grow from USD 620 million to reach a peak of USD 783 million, resulting in a 26.3 % rise before the total costs decrease to USD 712 million.

- The evidence displays initial steps toward achieving better cost management and efficiency improvements, which started to take shape during the final months of 2025.

- The company spends between USD 75 million and USD 86 million per quarter on stock-based compensation, which creates a major expense that reduces short-term earnings but helps the company keep its employees while building future innovation capabilities.

- The analysis through statistical methods reveals that companies face ongoing financial strain because their operating costs reach more than half of their total revenue.

- The Q4 results show a small decrease, which indicates that the organization has made progress in developing better methods to manage its expenses.

Rivian’s R2 Launch and AI Ecosystem Strategy

- Rivian has reached a crucial operational stage, which combines its product development, artificial intelligence research, and facility development efforts to establish its electric vehicle market competition standing.

- The company expects to begin customer deliveries in Q2 2026 after completing manufacturing validation builds at its Illinois facility in early 2026.

- The introduction of a Dual-Motor AWD system will enable the company to achieve better performance results at lower costs while expanding its operations beyond premium markets.

- The achievement of this milestone establishes production capabilities and operational performance, which are essential for increasing production capacity.

- Rivian is increasing its investment in autonomous technology and artificial intelligence to create unique technological advantages.

- The combination of its third-generation autonomous driving system and its exclusive RAP1 chip technology enables Rivian to achieve major improvements in computing power and sensor system design.

- The development of “eyes-off” technology, together with Level 4 autonomy, will enable Rivian to enter the next phase of software-driven vehicles, which will generate revenue through artificial intelligence capabilities.

- The Universal Hands-Free (UHF) system launch enabled assisted driving capabilities across 3.5 million miles throughout North America. Post-launch usage doubled because of strong consumer adoption of advanced driver assistance systems (ADAS).

- The upcoming Rivian Assistant (2026), together with Rivian Unified Intelligence, represents a new direction that creates personalized artificial intelligence-driven platforms that offer voice-activated contextual control and calendar synchronization functionalities.

- Operationally, Rivian is strengthening its service and distribution network, now comprising 36 retail spaces, 97 service locations, and ~700 mobile service vehicles, enabling scalable customer support and brand accessibility.

Rivian’s 2025 Software Monetization

- Rivian achieved its first complete fiscal year profitability by generating USD 144 million in gross earnings for 2025, which created a financial turnaround that brought its total losses from USD 1.2 billion to USD 1.3 billion.

- The company reached its first profitability level through software monetization, which operates as the main driver of its business model that combines hardware with software commercial activities.

- The USD 5.8 billion joint venture with Volkswagen Group serves as the primary element that enables Rivian to create its new financial system structure.

- The JV, Rivian Volkswagen Technologies, combines Rivian’s zonal architecture, software stack, and electrical systems with Volkswagen’s global scale, enabling deployment across brands like Volkswagen, Audi, and Porsche. The deal’s milestone-based funding—USD 1B convertible note (2024), USD 1B equity (2025), and ~USD 2B expected in 2026—ensures liquidity support while incentivizing operational execution.

- The software and services segment shows its highest financial impact because it achieved USD 1.56 billion in revenue during 2025, which represents a 222% year-over-year growth from its USD 484 million figure in 2024.

- The company achieved a gross profit of USD 576 million, which substantiated its total profits for the business.

- The software revenue for Q4 reached USD 447 million, while the company obtained about USD 179 million in gross profit, which produced profit margins of about 40%.

- The software-defined vehicle (SDV) thesis demonstrates that high-margin recurring revenue streams work together with low-margin hardware sales to support business operations.

- The implementation of Rivian’s zonal architecture system enables automotive digital transformation through its two main advantages, which decrease wiring requirements by almost half and provide over-the-air updates together with paid feature access.

- According to industry forecasts, automotive software will generate approximately 30 % of total industry profits by 2035, which demonstrates the enduring value of Rivian’s platform-based licensing approach.

- The company experienced a 15.7 % reduction in vehicle deliveries, which brought its total to 42,247 units. Their revenue decreased to USD 3.83 billion, which represented a 15 % drop.

- The business experienced a revenue decline because of reduced sales volume, combined with a loss of money on each unit sold.

- The company needs to reduce its vehicle production costs, which currently stand at approximately USD 100,900.

- The R2 platform will achieve production costs below USD 60,000, which serves as an essential requirement for businesses to reach mass market success and generate profits.

- The R2 launch, which will occur in Q2 2026, marks the point where Rivian unites its hardware and software development methods to create a product that demonstrates its self-driving vehicle system.

- The company expands its software monetization system through its Autonomy+ packages, which require a USD 2,500 initial payment or a USD 49.99 monthly fee. This system builds continuous income streams that depend on the vehicle base that the company continues to expand.

- The company expects to deliver between 62,000 and 67,000 units in 2026. This delivery growth will boost the company’s installed base, which will lead to increased software revenue.

2026 Outlook – The R2 Production Ramp and “Inflection Point.”

- The year 2026 marks a critical moment for Rivian because the company needs to change its business model from producing high-end electric vehicles in limited quantities to establishing an operational framework that supports multiple vehicle models.

- The R2 platform serves as the main aspect for this evolution because it will introduce a compact electric SUV with a starting price of USD 45,000.

- The R2 platform will enable widespread market access, which will result in increased production volumes for the company.

- The company expects to deliver between 62000 and 67000 units during 2026, which represents a major increase of 47 to 59 % when compared to the 42247 vehicles delivered in 2025.

- The company will primarily expand through R2, which is projected to deliver between 20000 and 25000 additional units.

- The R1T and R1S vehicles, together with commercial vans, will maintain their existing sales volume of approximately 42000 units, which establishes Rivan’s business expansion path as entirely dependent on R2’s successful implementation.

- The R2 Performance, with a price tag of USD 57990, and the Premium model, which costs USD 53990, will start their launch process before the Standard Long Range model debuts in 2027 with a price point of USD 48490.

- The company develops its product sequence to achieve maximum revenue during the initial production period, when output volumes will remain limited.

- R2 establishes itself as a strong competitor in the mid-size electric SUV market through its performance specifications, which include 656 horsepower and a 0-60 mph acceleration time of 3.6 seconds and approximately 345-mile driving distance capacity.

- The expansion of Rivian’s Normal, Illinois, plant demonstrates its approach to capital-efficient operations.

- The facility will expand by 1.1 million square feet, resulting in a total building area of 5.4 million square feet.

- The facility will operate at a yearly capacity of 215000 units, which includes 155000 R2 and 60000 R1 and commercial vehicles.

- The decision to move R2 production from Georgia to Illinois will save the company approximately USD 2.25 billion in capital expenditures, which will help the company maintain its financial resources during a time of increased spending.

- The 2026 CapEx guidance of USD 1.95–USD 2.05 billion is Rivian’s largest annual investment, with approximately USD 1–1.2 billion directed toward R2 tooling and production infrastructure.

- The company holds 6.08 billion in liquid assets, which enables it to operate without depending on outside funding for the foreseeable future.

- The company expects adjusted EBITDA losses to reach between USD 1.8 billion and USD 2.1 billion.

- The loss per vehicle will drop from about USD 47000 in 2025 to around USD 30000 in 2026, which represents a 36% improvement that results from the growth of software revenue and the operational effectiveness and R2 projects.

- H1 2026 will see lower quarterly volumes (9,000–11,000 units) due to production ramp constraints, with profitability improvement expected in H2 as throughput scales and software milestone revenues materialize.

- The strategic path that Rivian follows currently shows alignment with the main developments that affect the entire automotive sector.

- The transition from 40,000 to 80,000 units is widely recognized as the threshold for fixed-cost absorption in software-defined vehicle platforms, which can cut software expenses by half.

- The R2 product functions as a dual-purpose asset that creates sales growth while driving profitability improvements for all of Rivian’s business operations.

Conclusion

Rivian Automotive is undergoing a critical transition from a niche premium EV manufacturer to a scalable, technology-driven mobility company. The company reached its first annual gross profit milestone in 2025, yet it continues to face operational difficulties due to active net losses and decreased deliveries. The fast expansion of software and services revenue changes Rivian’s financial structure because it delivers higher-profit income sources, which counterbalance the company’s low automotive profitability.

The R,2 platform launch, which will occur in 2026, operates as a major turning point because it will enable both large production growth and significant cost savings. The success of Rivian depends on three factors, which include operational performance, production growth, and effective software ecosystem monetization.

FAQ

Rivian reported its first full-year gross profit of USD 144 million but still recorded net losses.

Automotive revenue showed variable results because vehicle delivery numbers changed and price challenges emerged.

Software revenue grew 222% Year Over Year to USD 1.56 billion, which became a vital revenue source that boosted profits for the company.

Rivian expects to deliver 62,000–67,000 vehicles in 2026.

The R2 is a mass-market EV expected to drive volume growth, reduce costs, and improve profitability.