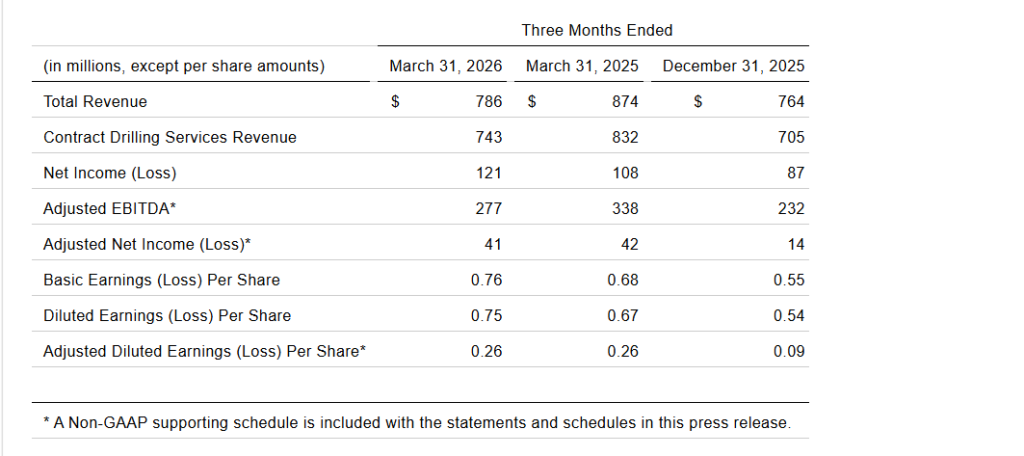

Noble Corporation plc reported Q1 2026 revenue of $786 million, down year on year and slightly below the prior year quarter, with net income of $121 million and diluted EPS of $0.75 supported by strong cash generation and a solid backlog, while shares moved on after hours commentary and guidance rather than any disclosed intraday price reaction.

About Noble Corporation plc

Noble Corporation plc (NYSE: NE) is a leading offshore drilling contractor focused on ultra deepwater and high specification jackup rigs for the global oil and gas industry. The company and its predecessors have been drilling oil and gas wells since 1921, giving it more than a century of operating history in offshore services. Noble is headquartered in Houston, Texas, and operates a modern fleet of floaters and jackups across established and emerging offshore basins worldwide.

As of March 31, 2026, Noble reported total assets of $7.48 billion, shareholders’ equity of $4.59 billion, and total debt of about $1.9 billion, implying a moderately leveraged balance sheet for a capital intensive offshore driller. The company held $663 million of cash and cash equivalents at quarter end, supporting liquidity and its shareholder return plan including a recurring $0.50 per share quarterly dividend. Noble’s fleet utilization reached 69% on average in Q1 2026, with floater dayrates in the low to mid $400,000s and strong contracting momentum driving a reported $7.5 billion backlog.

Top Financial Highlights

- Total revenue for Q1 2026 was $786 million, down from $874 million in Q1 2025 but up from $764 million in Q4 2025.

- Contract drilling services revenue reached $743 million, rising from $705 million in the prior quarter on higher fleet utilization.

- Net income came in at $121 million, compared with $108 million a year earlier and $87 million in Q4 2025.

- Diluted EPS was $0.75, with adjusted diluted EPS of $0.26 after normalizing for non recurring items.

- Adjusted EBITDA totaled $277 million, down from $338 million in Q1 2025 but up from $232 million in Q4 2025.

- Operating cash flow was $273 million, essentially flat versus $271 million in Q1 2025 and well above Q4 2025.

- Free cash flow reached $169 million, compared with $173 million a year ago and $35 million in the prior quarter.

- Contract drilling services costs were $450 million, down from $471 million in Q4 2025, supporting margin improvement despite lower year on year revenue.

- Cash and cash equivalents stood at $663 million at March 31, 2026, after funding capex of $104 million and a quarterly dividend payment of $0.50 per share.

- The company reported total debt principal of about $1.9 billion and redeemed $55 million of 8.5% senior secured notes due 2030 during the quarter.

- Backlog was approximately $7.5 billion, supported by about $565 million of new contract value since the January fleet status report.

- Fleet utilization averaged 69% overall, with floaters at 65% and jackups at 78%, up from 62% total utilization in Q4 2025.

- Average floater dayrates rose to about $422,000 per day, and total fleet average dayrates reached about $349,000 per day.

- Management reaffirmed full year 2026 guidance for revenue of $2.8–3.0 billion and adjusted EBITDA of $940–1,020 million, while lifting 2026 capex guidance by $25 million to reflect the Noble Deliverer reactivation.

Beat or Miss?

Noble’s Q1 2026 results showed a revenue and earnings beat versus available consensus estimates, with both the top line and EPS coming in ahead of forecasts according to external earnings call commentary. The table below summarizes reported figures against referenced expectations where available.

Reported vs Expected

| Metric | Reported Q1 2026 | Difference / Analysis |

| Revenue | $785.7 million | Above an external projection of about $733.3 million, indicating a revenue beat. |

| Net income | $120.7 million | Solid profit growth versus Q1 2025, driven by higher utilization and lower operating costs. |

| Diluted EPS | $0.75 | Described as beating forecasts on the Q1 2026 earnings call summary. |

| Adjusted diluted EPS | $0.26 | In line with the normalized earnings power after non recurring items. |

| Adjusted EBITDA | $277.4 million | Down year on year but ahead of the prior quarter, reflecting improving fleet economics. |

| Operating cash flow | $273.3 million | Strong cash generation, broadly consistent with recent history. |

| Free cash flow | $169.4 million | High conversion of earnings into cash despite elevated capex. |

What Leadership Is Saying

“We commenced 2026 with solid operational and financial results. Commercial momentum remains brisk, highlighted by the Noble Courage’s three year extension with Petrobras and the Noble Deliverer’s five well program with Woodside. We remain intensely focused on project execution, with several important contract commencements scheduled over the course of this year, each of which is progressing well.” – Robert W. Eifler, President and Chief Executive Officer

“With tightening floater fundamentals, the trajectory for dayrates, contract duration and earnings visibility is improving. We continue to anticipate a meaningful financial inflection next year supported by existing backlog and a robust bidding pipeline. Against this backdrop, Noble will continue to prioritize our leading shareholder return program.”

– Robert W. Eifler, President and Chief Executive Officer, commenting on margins and returns

Historical Performance

Noble’s year on year comparison shows lower revenue but higher profitability, as cost controls, asset sales, and improved dayrates offset volume pressure. The table uses Q1 2025 as the prior year benchmark.

Q1 2026 vs Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

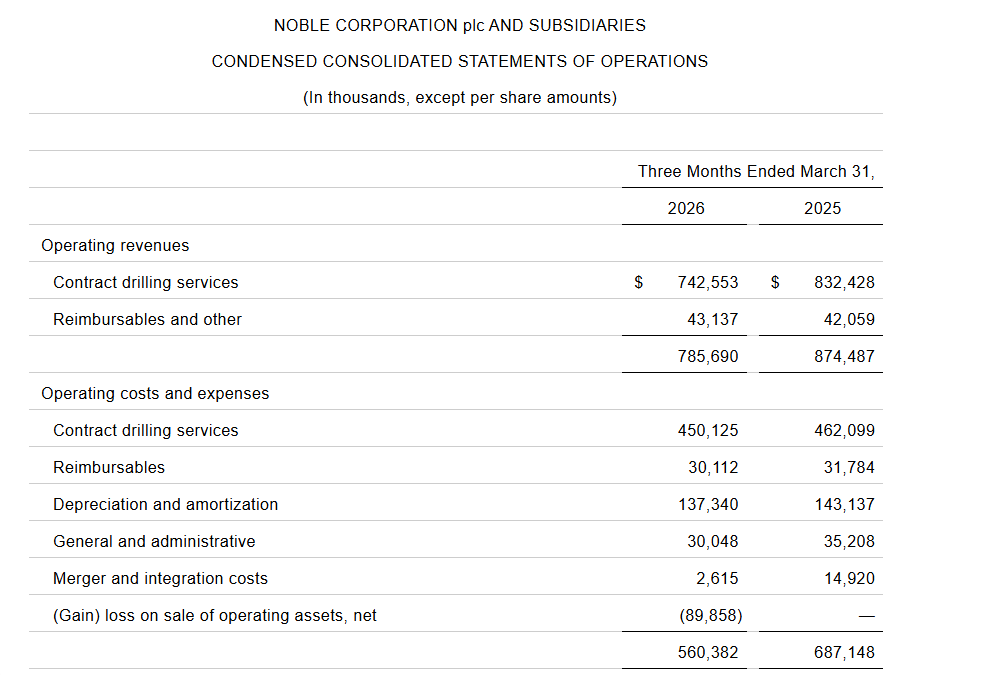

| Revenue | $785.7 million | $874.5 million | ≈−10.2%≈−10.2% decline in sales year on year. |

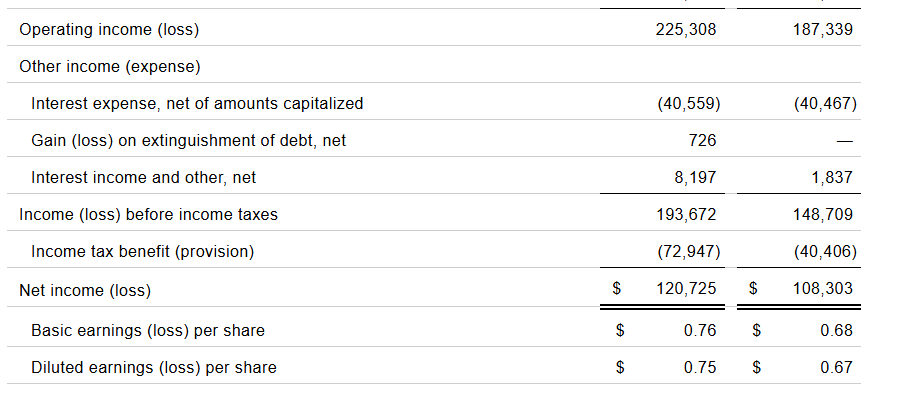

| Net income | $120.7 million | $108.3 million | ≈+11.4%≈+11.4% increase in earnings. |

| Operating expenses* | $560.4 million | $687.1 million | ≈−18.4%≈−18.4% reduction, reflecting asset sale gain and lower costs. |

Historical Performance of Selected Peers (YoY Illustration)

The Q1 2026 Noble release does not disclose detailed competitor financials, so the table below is an illustrative structure using Noble as the reference line and marking peers as not available (N/A) based on this document set.

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Noble – Revenue | $785.7 million | $874.5 million | ≈−10.2%\approx -10.2\%≈−10.2% |

| Noble – Net income | $120.7 million | $108.3 million | ≈+11.4%\approx +11.4\%≈+11.4% |

| Noble – Operating expenses | $560.4 million | $687.1 million | ≈−18.4%\approx -18.4\%≈−18.4% |

| Peer offshore driller A – Revenue | – | – | – |

| Peer offshore driller B – Net income | – | – | – |

How the Market Reacted?

Third party coverage of Noble’s Q1 2026 earnings call indicates that the company “beat forecasts” on both revenue and EPS, with the stock rising on the back of better than expected results and a constructive outlook for dayrates and backlog. Although the press release itself does not state an exact percentage move, commentary notes that shares traded higher following the announcement and call, reflecting investor confidence in the improved earnings trajectory into 2027.

Sentiment around the print can be characterized as bullish, driven by rising utilization, stronger cash generation, and a robust $7.5 billion backlog alongside an unchanged revenue and EBITDA guidance range.