Sanofi posted Q1 2026 Business EPS of €1.88 (up 14% at CER), beating analyst estimates of $1.04 per ADR, on revenues of €10.51 billion that topped consensus of €10.22 billion. Shares of SNY jumped on April 23, 2026, after the strong Dupixent-driven beat, with the stock rising approximately 4.28% in after-hours movement.

About Sanofi

Sanofi S.A. (NASDAQ: SNY; Euronext: SAN) is a French multinational pharmaceutical and healthcare company headquartered in Paris. The company traces its roots to 1973 and took its current structure through the 2004 merger of Sanofi-Synthélabo and Aventis, making it one of the world’s largest drugmakers by revenue.

As of April 2026, Sanofi carries a market capitalization of approximately $112-$113 billion, employs more than 83,000 people across 70 countries, and runs one of the industry’s most closely watched pipelines spanning immunology, rare diseases, vaccines, neurology, and oncology.

The company’s flagship asset, Dupixent (dupilumab), co-developed with Regeneron, is now approved for 11 indications globally and is quickly becoming one of the best-selling drugs in the world. SNY currently trades at a price-to-earnings ratio of approximately 19.82x, with a 52-week price range of $43.32 to $55.73.

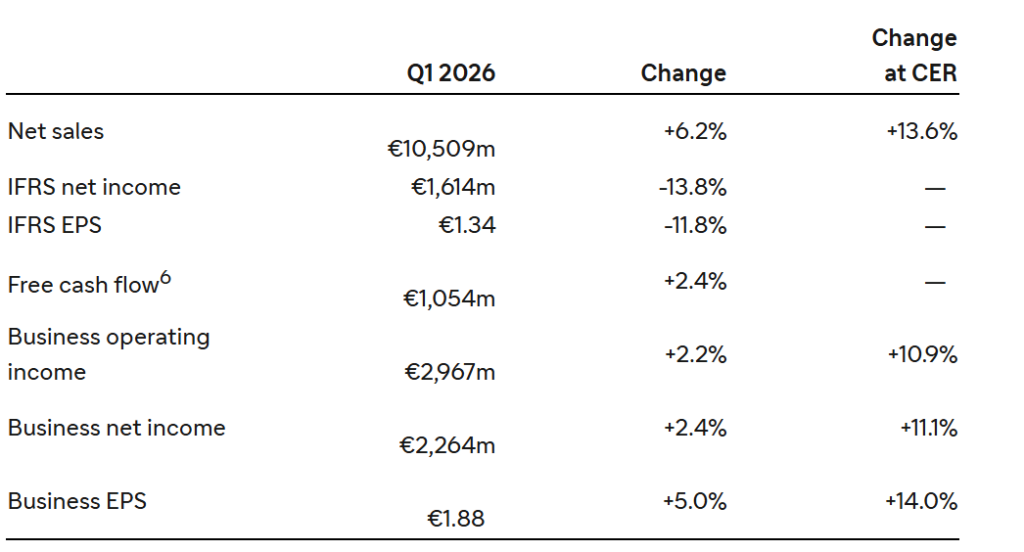

Top Financial Highlights

- Net sales reached €10,509 million, increasing 6.2% on a reported basis and 13.6% at constant exchange rates, reflecting strong underlying demand.

- Business EPS stood at €1.88, up 14.0% at constant exchange rates and 5.0% reported, while IFRS EPS was €1.34, declining 11.8% due to non-cash amortization impacts.

- Dupixent sales totaled €4,170 million, rising 30.8% globally and exceeding the €4 billion quarterly level for the second consecutive quarter.

- U.S. sales reached €5,289 million, growing 26.2% at constant exchange rates, supported by key product performance and recent acquisitions.

- Pharma launches generated €1,171 million, increasing 49.6%, led by strong contributions from ALTUVIIIO, Ayvakit, and Sarclisa.

- Vaccines sales were €1,293 million, up 2.1%, supported by portfolio expansion following recent acquisitions.

- Business operating income totaled €2,967 million, increasing 10.9%, with a margin of 28.6%, slightly lower by 0.7 percentage points.

- Business net income reached €2,264 million, up 11.1%, reflecting solid operational performance.

- Free cash flow stood at €1,054 million, increasing 2.4% year over year.

- Research and development expenses were €1.7 billion, rising 1.5%, indicating controlled investment in innovation.

- Selling, general, and administrative expenses reached €2.3 billion, up 11.6%, primarily due to acquisition-related impacts.

- Share buybacks totaled €921 million, nearing completion of the €1 billion program.

- Full-year 2026 guidance has been reaffirmed, with expected high single-digit sales growth and business EPS projected to grow slightly faster than revenue on a constant exchange rate basis.

Beat or Miss?

| Metric | Reported | Estimated | Difference / Analysis |

| Net Sales (EUR) | €10,509m | €10,220m | Beat by ~€289m; analysts at Vara Research |

| Net Sales (USD equiv.) | $12.44B | $12.40B | Narrow beat per FactSet |

| Business EPS (ADR, USD) | $1.10 | $1.04-$1.06 | Beat by ~3.8-5.8% |

| Business EPS (EUR, CER) | € 1.88 | €1.79 implied | Beat vs prior year; +14% CER growth |

| Business Operating Income | €2,967m | €2,850m | Beat by ~€117m |

| Dupixent Sales | €4,170m | ~€3,890m | Beat by ~€280m |

What Leadership Is Saying?

CEO – Olivier Charmeil (Interim CEO):

“We had a strong start to 2026 with double-digit sales and business EPS growth. Sales increased by 13.6%, supported by Pharma launches and recent acquisitions. Dupixent sales were above the €4 billion quarterly mark again and grew by 30.8%. Business EPS was up by 14.0%, reflecting a measured growth of 7.0% in total operating expenses. We reiterate our guidance for 2026: we continue to expect sales to grow by a high single-digit percentage and business EPS to grow slightly faster than sales, at constant exchange rates, delivering profitable growth.”

CFO – Francois-Xavier Roger:

“Net sales grew 13.6% to EUR 10.5 billion in the first quarter, with like-for-like sales up 12%.”

Historical Performance

Sanofi: Q1 2026 vs. Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Net Sales (EUR) | €10,509m | €9,895m | +6.2% reported; +13.6% CER |

| IFRS Net Income | €1,614m | €1,872m | -13.80% |

| IFRS EPS | € 1.34 | € 1.52 | -11.80% |

| Business EPS | € 1.88 | € 1.79 | +5.0% reported; +14.0% CER |

| Business Operating Income | €2,967m | €2,902m | +2.2% reported; +10.9% CER |

| Business Net Income | €2,264m | €2,212m | +2.4% reported; +11.1% CER |

| Free Cash Flow | €1,054m | €1,029m | 2.40% |

| Dupixent Sales | €4,170m | ~€3,188m | +30.8% CER |

| Pharma Launches | €1,171m | ~€782m | +49.6% CER |

| R&D Expenses | €1.7B | €1.8B | -1.5% (down) |

Competitor Performance

Key pharma peers for context (most recent available data, calendar Q1 2026 where published, otherwise latest reported quarter):

| Company | Period | Revenue | YoY Revenue Change | Net Income / EPS | Key Note |

| Sanofi (SNY) | Q1 2026 | €10,509m (~$12.44B) | +13.6% CER | Business EPS €1.88 | Beat estimates; Dupixent +30.8% |

| AstraZeneca (AZN) | FY 2025 (Q4 2025 = $15.5B) | $58,739m FY 2025 | +9% FY 2025 | Core EPS $9.16 FY 2025 | Q1 2026 results due April 29; analysts expected $14.74B revenue |

| Pfizer (PFE) | FY 2025 / Q4 2025 | $62.6B FY 2025 | -2% operational FY 2025 | Adj. EPS $3.22 FY 2025 | 2026 revenue guidance $59.5-$62.5B; Q1 2026 results due May 5 |

| Novo Nordisk (NVO) | Q1 2025 | $11.02B | +19% YoY (DKK) | EPS $0.92/ADR | Q1 2026 results due May 6; 2026 sales growth revised to 5-13% |

How the Market Reacted?

Sanofi shares (SNY on NASDAQ) responded positively to the Q1 2026 beat, with the stock jumping following the earnings announcement on April 23, 2026. The closing price on April 23 was $47.56, compared to an opening of $47.39 on the same day, reflecting a 0.36% gain on a day when the broader market was processing the results.

The investor reaction aligned with the bullish tone of the report: revenues of €10.51 billion topped the €10.22 billion analyst consensus, business operating income of €2.97 billion beat the €2.85 billion forecast, and Dupixent’s €4.17 billion in sales exceeded the ~€3.89 billion consensus.

The sentiment was predominantly bullish, bolstered by reaffirmed 2026 guidance and five new regulatory approvals all in the high-growth immunology space, though the decline in IFRS EPS (-11.8%) and slightly lower BOI margin (-0.7 pp) tempered some enthusiasm among value-focused investors.