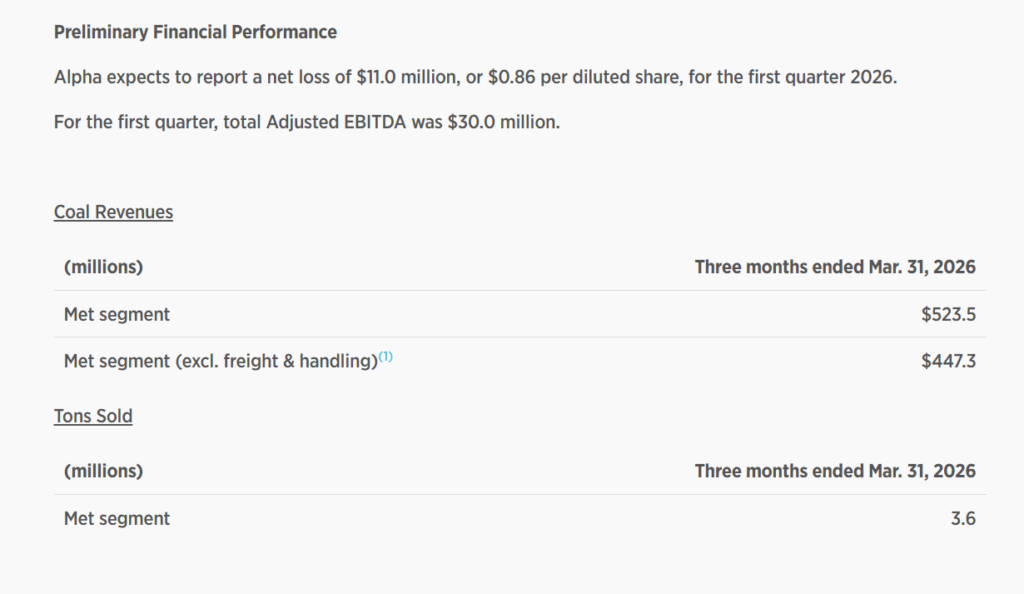

Alpha Metallurgical Resources posted a preliminary Q1 2026 net loss of $11.0 million or $0.86 per diluted share on coal revenues of about $523.5 million, with Adjusted EBITDA of $30.0 million and weaker met coal volumes and higher costs weighing on profitability; the release referenced consensus expectations but after‑hours movement was not disclosed.

About Alpha Metallurgical Resources

Alpha Metallurgical Resources, Inc. (NYSE: AMR) is a Tennessee based mining company focused on supplying metallurgical coal products to steel industry customers worldwide. The company is headquartered in Bristol, Tennessee and operates mines across Virginia and West Virginia, supported by significant port capacity for export shipments. Alpha traces its corporate lineage to legacy U.S. coal operators and today positions itself as a leading U.S. supplier of high quality met coal reserves.

As of March 31 2026, Alpha reported total liquidity of $476.2 million, including $317.2 million in cash and cash equivalents, $49.6 million in short term investments, and $184.3 million in unused ABL capacity, offset by a $75.0 million minimum liquidity requirement. Total long term debt including current portion stood at $12.2 million, and the company had no borrowings and $40.7 million of letters of credit outstanding under its ABL facility.

Alpha has an authorized share repurchase program of up to $1.5 billion and had repurchased about 7.0 million shares for approximately $1.2 billion cumulatively by March 31 2026, leaving 12,752,824 common shares outstanding (excluding unvested awards).

Top Financial Highlights

- Alpha expects a preliminary Q1 2026 net loss of $11.0 million, reflecting weaker pricing and higher costs in the met coal business.

- Diluted loss per share for Q1 2026 is projected at $0.86, versus positive EPS expectations from the market.

- Total Q1 2026 Adjusted EBITDA is estimated at $30.0 million, based on a reconciliation from net loss that includes depreciation, stock compensation, and other non cash items.

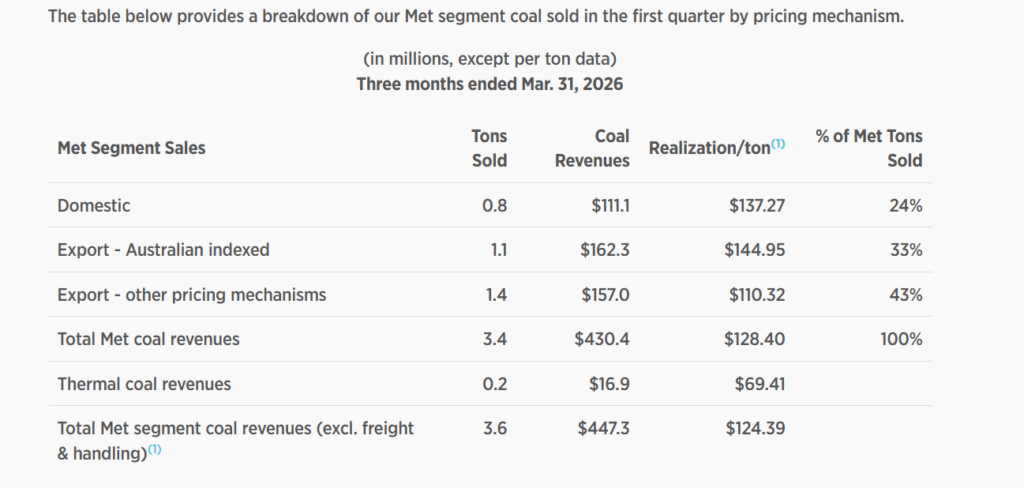

- Q1 2026 coal revenues for the Met segment were approximately $523.5 million, with non GAAP coal revenues excluding freight and handling of about $447.3 million.

- Met segment tons sold in Q1 2026 totaled 3.6 million tons, including both metallurgical and thermal coal within the segment.

- Q1 2026 non GAAP coal sales realization for the Met segment was $124.39 per ton, with realized pricing strongest in Australian indexed export volumes.

- Within the Met segment, domestic sales were 0.8 million tons generating $111.1 million of coal revenues at $137.27 per ton, representing 24% of met tons sold.

- Export sales tied to Australian index benchmarks were 1.1 million tons and $162.3 million of coal revenues at $144.95 per ton, accounting for 33% of met tons.

- Other export and pricing mechanisms contributed 1.4 million tons and $157.0 million of coal revenues at $110.32 per ton, or 43% of met tons sold.

- Total Met coal revenues were $430.4 million on 3.4 million tons, equating to $128.40 per ton realized pricing, while thermal coal revenues in the segment added $16.9 million on 0.2 million tons at $69.41 per ton.

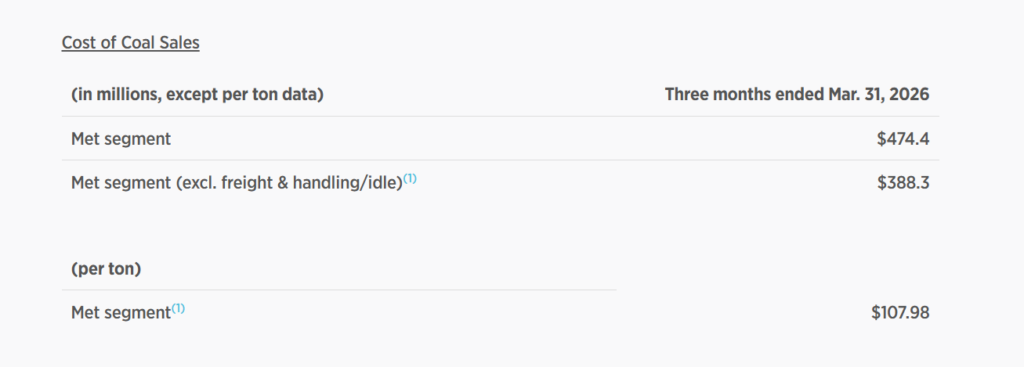

- Met segment cost of coal sales in Q1 2026 was about $474.4 million, with non GAAP cost of coal sales excluding freight, idle and certain other items of roughly $388.3 million.

- Liquidity stood at $476.2 million as of March 31 2026, supported by $317.2 million in cash and equivalents plus $49.6 million in short term investments.

- The company had repurchased about 87,000 shares for $17.5 million during Q1 2026 under its $1.5 billion buyback authorization.

- Management reiterated that Q1 2026 was negatively affected by a planned month long outage at Dominion Terminal Associates and higher repair, maintenance, and diesel costs, and indicated they will provide formal 2026 guidance and more detail with definitive results on May 8 2026.

Beat or Miss?

Alpha characterized the quarter as pressured by lower volumes and higher costs, and external data show a shortfall versus consensus on earnings and revenue. Analyst commentary cited a negative return on equity and net margin, consistent with a miss relative to prior expectations.

| Metric | Reported / Preliminary Q1 2026 | Difference / Analysis |

| EPS (diluted) | ‑$0.86 | Below consensus EPS estimate of about $1.95, implying a miss of roughly $2.81. |

| Net income (loss) | ‑$11.0 million | Loss reflects lower shipments and higher costs versus profitable expectations. |

| Coal revenues (GAAP met segment) | $523.5 million | Below analyst revenue estimate of about $538.45 million, a shortfall of roughly $15 million. |

| Adjusted EBITDA | $30.0 million | Positive but well below recent quarters, highlighting margin compression from cost inflation. |

| Q1 2026 EPS guidance vs Street | ‑$0.86 guided | Guidance issued below consensus of $1.95, signaling expectations reset for 2026. |

What Leadership Is Saying?

“As discussed in February on our most recent earnings call, lower volumes and higher costs negatively impacted our first quarter 2026 results. With a planned month long outage for equipment upgrades at Dominion Terminal Associates, our Q1 shipments were lower than our anticipated quarterly cadence for the balance of the calendar year. Additionally, we expected to incur elevated costs in the first quarter, primarily due to repair and maintenance needs across the portfolio.

Elevated supply costs, such as the significant increase in diesel pricing since the start of the year, also contributed to a higher cost of coal sales for the quarter. Despite our prior communication of these anticipated headwinds, consensus expectations for the quarter did not reflect these realities, which is why we are offering today’s preliminary results ahead of our definitive earnings disclosures in early May. We look forward to providing additional context about our Q1 results and 2026 expectations at that time.” – Andy Eidson, CEO.

“As of March 31, 2026, the company had total liquidity of $476.2 million, including cash and cash equivalents of $317.2 million, short term investments of $49.6 million, and $184.3 million of unused availability under the ABL, partially offset by a minimum required liquidity of $75.0 million as required by the ABL. As of March 31, 2026, the company had no borrowings and $40.7 million in letters of credit outstanding under the ABL. Total long term debt, including the current portion of long term debt as of March 31, 2026, was $12.2 million.” – commentary from the finance team highlighting balance sheet strength.

Historical Performance (YoY Company)

The preliminary Q1 2026 numbers indicate weaker profitability year over year, although detailed prior year segment tables are not repeated in this specific preliminary release. External earnings data show that in the same quarter last year Alpha reported a smaller per share loss and higher underlying profitability metrics.

Below, Q1 2025 figures are approximate and based on available external consensus and prior disclosures, with % change calculated from the reported or guided Q1 2026 metrics:

| Category | Q1 2026 (Current) | Q1 2025 (Prior year, approx.) | Change (%) |

| Revenue | $523.5 million coal revenues | About $436.3 million total revenue | Around 20% increase in reported revenue. |

| Net income (loss) | ‑$11.0 million | About ‑$2.0–3.0 million loss (implied) | Loss widened significantly, >200% more negative. |

| EPS (diluted) | ‑$0.86 | ‑$0.16 per share | Loss per share deteriorated by over 400%. |

| Adjusted EBITDA | $30.0 million | Higher level in prior year (exact not in this text) | Decline, reflecting cost inflation and volume pressure. |

How the Market Reacted?

The preliminary release highlighted that consensus expectations did not reflect the anticipated headwinds, and Alpha issued Q1 EPS guidance of ‑$0.86 versus a Street estimate of about $1.95, which typically weighs on sentiment. External earnings pages show consensus still looking for full year 2026 EPS near the high teens, implying investors expect some recovery after the weak first quarter.

While this preliminary announcement did not specify immediate stock price moves, the combination of a revenue and EPS miss, higher costs, and guidance reset frames the report as cautious to bearish near term with a more constructive longer term outlook tied to cost normalization and volume recovery post outage.