Cameco reported Q1 2026 diluted EPS of $0.30 and adjusted EPS of $0.47 on revenue of $845 million, with net earnings nearly doubling year over year and adjusted EBITDA up 44%. The release did not specify the immediate stock reaction, so after-hours movement remains unclear.

About Cameco

Cameco Corporation (TSX: CCO, NYSE: CCJ) is one of the world’s largest providers of uranium fuel to the global nuclear power industry. The company is headquartered in Saskatoon, Saskatchewan, Canada, and controls tier one uranium mining assets in Canada and Kazakhstan alongside integrated fuel services operations. Cameco also holds ownership interests in Westinghouse Electric Company and Global Laser Enrichment, extending its reach across the nuclear fuel cycle.

Cameco’s market capitalization, based on its role as a leading uranium supplier and dual listing in Toronto and New York, can reasonably be estimated in the multi‑billion dollar range, though the precise figure is not disclosed in the Q1 release. The company’s results are reported under IFRS, and it emphasizes a disciplined contracting and operating strategy that aligns marketing, production and capital decisions with strengthening nuclear industry fundamentals. While the press release does not provide a current P/E ratio or dividend yield, it highlights a strong balance sheet with $1.1 billion in cash, cash equivalents and short term investments and $1.0 billion in total debt as of March 31, 2026.

Top Financial Highlights

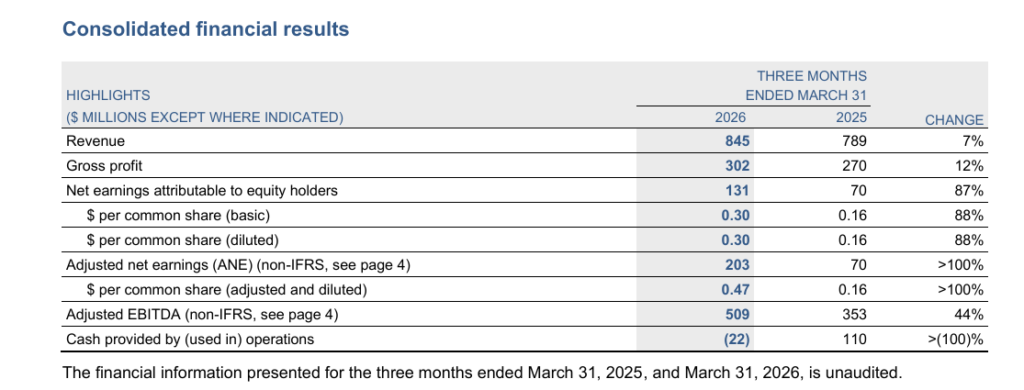

- Q1 2026 revenue was $845 million versus $789 million in Q1 2025, a 7% increase.

- Gross profit rose to $302 million from $270 million, up 12% year over year.

- Net earnings attributable to equity holders were $131 million, up from $70 million in Q1 2025, an 87% increase.

- Diluted EPS came in at $0.30 compared with $0.16 a year earlier, an 88% jump.

- Adjusted net earnings were $203 million versus $70 million, with adjusted EPS of $0.47 versus $0.16, both more than doubling year over year.

- Adjusted EBITDA reached $509 million, up from $353 million, representing a 44% increase.

- Cash provided by (used in) operations was negative $22 million compared with positive $110 million in Q1 2025, reflecting quarterly working capital variability.

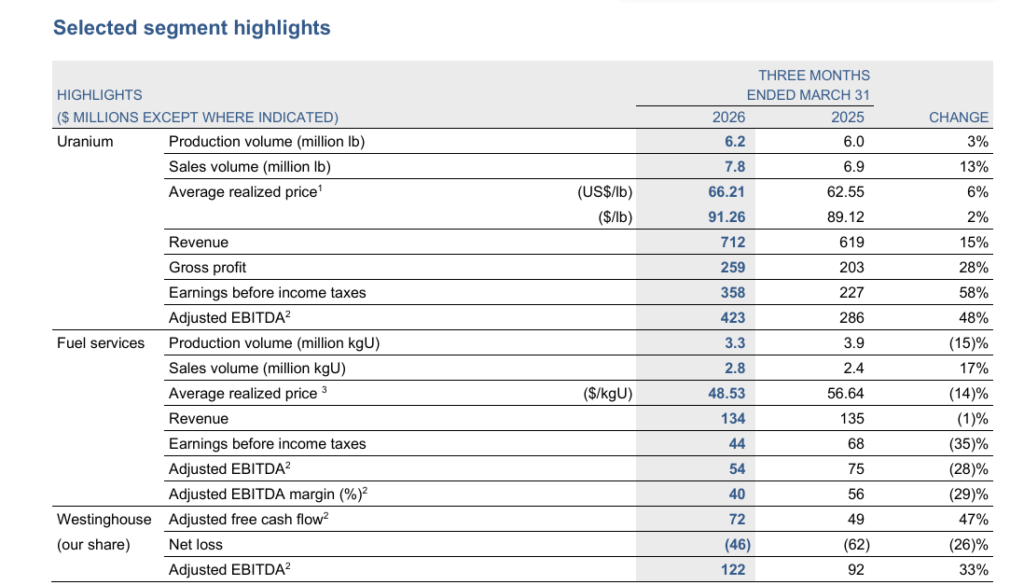

- Uranium segment revenue was $712 million, up from $619 million, with sales volume of 7.8 million lb versus 6.9 million lb and an average realized price of $91.26 per pound (US $66.21).

- Uranium segment gross profit was $259 million vs. $203 million, and earnings before income taxes were $358 million vs. $227 million, with adjusted EBITDA of $423 million vs. $286 million.

- Fuel services revenue was $134 million vs. $135 million, with sales volume of 2.8 million kgU vs. 2.4 million kgU and an average realized price of $48.53 per kgU vs. $56.64.

- Fuel services earnings before income taxes were $44 million vs. $68 million, and adjusted EBITDA was $54 million vs. $75 million, with an adjusted EBITDA margin of 40% vs. 56%.

- Westinghouse contributed a net loss of $46 million (Cameco’s share), an improvement from a $62 million loss, while adjusted EBITDA (Cameco’s share) was $122 million vs. $92 million.

- Cash, cash equivalents and short term investments totaled $1.1 billion with $1.0 billion in total debt and a $1.0 billion undrawn revolving credit facility, underscoring balance sheet strength.

- Cameco reaffirmed its 2026 annual guidance, including expected uranium production of 19.5 to 21.5 million lb (Cameco’s share) and fuel services production of 13 to 14 million kgU.

Beat or Miss?

| Metric | Reported Q1 2026 | Difference/Analysis |

| Revenue | $845 million | Consensus estimate N/A; grew 7% year over year. |

| Net earnings | $131 million | Nearly doubled vs. Q1 2025; strong uranium contribution. |

| Diluted EPS (IFRS) | $0.30 | Up 88% year over year; consensus not disclosed. |

| Adjusted EPS | $0.47 | More than doubled vs. prior year; no Street figure given. |

| Adjusted EBITDA | $509 million | Up 44% vs. Q1 2025, driven by higher uranium prices and volumes. |

| Operating cash flow | -$22 million | Down from +$110 million; reflects timing and working capital. |

| Uranium revenue | $712 million | Up 15% year over year; strong pricing and higher volumes. |

| Fuel services revenue | $134 million | Essentially flat year over year; lower prices offset higher volumes. |

| Westinghouse net loss | -$46 million | Loss narrowed vs. -$62 million; adjusted EBITDA improved |

What Leadership Is Saying

CEO: Tim Gitzel on Strategy and Vision

“With tier-one mining assets, a disciplined approach to supply, and an integrated fuel and reactor life cycle strategy, we believe Cameco is uniquely positioned to take advantage of opportunities as the market evolves, while continuing to navigate market uncertainty and create long-term value as nuclear energy’s role expands. Governments, utilities and energy-intensive industries are recognizing that nuclear energy is uniquely positioned to meet these needs, providing long-term energy security and reinforcing national security, while advancing efforts to meet decarbonization targets.”

Tim Gitzel, Chief Executive Officer, Cameco

CEO: Tim Gitzel on Financial Discipline and Balance Sheet

“Our results for the first quarter of 2026 remained consistent with our annual expectations across the business. We are on track in our uranium, fuel services and Westinghouse segments, reinforcing the value of our disciplined contracting and operating strategy that aligns marketing, production and capital decisions with strengthening industry fundamentals. Financially, our strong balance sheet, which allows us to be patient as the market evolves, remains a key strength.”

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Revenue (CAD $M) | $845M | $789M | 7% |

| Net Earnings (CAD $M) | $131M | $70M | 87% |

| Adjusted Net Earnings (CAD $M) | $203M | $70M | +>100% |

| Gross Profit (CAD $M) | $302M | $270M | 12% |

| Adjusted EBITDA (CAD $M) | $509M | $353M | 44% |

| Uranium Revenue (CAD $M) | $712M | $619M | 15% |

| Uranium Avg Realized Price (US$/lb) | US$66.21 | US$62.55 | 6% |

| Uranium Sales Volume (M lbs) | 7.8M lbs | 6.9M lbs | 13% |

| Fuel Services Revenue (CAD $M) | $134M | $135M | -1% |

| Westinghouse Adj EBITDA – Cameco share (CAD $M) | $122M | $92M | 33% |

| Cash from Operations (CAD $M) | -$22M | +$110M | >(100)% |

| Adjusted EPS – diluted (C$) | C$0.47 | C$0.16 | +>100% |

Competitor Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Cameco (CCJ/CCO) | |||

| Revenue (CAD $M) | $845M | $789M | 7% |

| Net Earnings (CAD $M) | $131M | $70M | 87% |

| Uranium Avg Realized Price | US$66.21/lb | US$62.55/lb | 6% |

| Kazatomprom (KAP) | |||

| Uranium Production (100% basis) | 6,144 tu | 5,633 tu | 9.10% |

| Uranium Sales Volume | 1,535 tu | 2,560 tu | -40.10% |

| Revenue (Q1 2025 ref, KZT B) | Q1 2026 financials pending | KZT 214.4B (~USD $238M) | N/A |

| Net Income (Q1 2025 ref, KZT B) | Q1 2026 financials pending | KZT 25.7B | N/A |

| Uranium Energy Corp (UEC) | |||

| Revenue (USD $M) | $20M | ~$49M (implied) | -59.40% |

| Net Income (USD $M) | -$14M | ~-$10M (implied) | -36.20% |

| Gross Margin | 49.60% | ~36.6% (implied) | +1,301 bps |

| NexGen Energy (NXE) | |||

| Revenue | Pre-revenue development stage | Pre-revenue | N/A |

| Key Update | Federal approval secured for Rook I; construction commencing summer 2026 | Permitting phase | Milestone |

How the Market Reacted?

Cameco shares responded positively at the open on May 5, 2026, jumping approximately 2.9% in early trading after the results confirmed the company was on track with its full-year guidance and delivered a meaningful earnings beat. However, shares retraced those gains through the session, with CCJ trading near $114.95 on the NYSE, a decline of about 2.80% from the previous close, as the broader market pulled back and investors weighed the negative operating cash flow figure of -$22 million against the headline profit growth.

The sentiment in the report is broadly bullish: strong uranium pricing trends, unchanged annual guidance, a solid balance sheet with $1.1 billion in cash, and a 33% jump in Westinghouse’s adjusted EBITDA contribution all reinforce Cameco’s strategic positioning in the growing nuclear energy market. Analysts from 15 firms maintain a “Moderate Buy” consensus with an average 12-month price target of $150.40, implying approximately 31% upside from current trading levels.