West Fraser posted Q1 2026 revenue of $1.334 billion and a diluted EPS of -$2.40, badly missing the consensus estimate of -$1.24. The result was heavily distorted by a non-cash $114 million duty charge for prior periods. The stock opened down approximately 1.5% the following trading session.

About West Fraser Timber Co. Ltd.

West Fraser Timber Co. Ltd. (TSX and NYSE: WFG) is a diversified Canadian wood products company founded in 1955 and headquartered in Vancouver, British Columbia. The company operates more than 50 facilities across Canada, the United States, the United Kingdom, and Europe, and employs approximately 10,000 workers globally.

West Fraser produces lumber, engineered wood products (including OSB, LVL, MDF, plywood, and particleboard), pulp, newsprint, wood chips, and other residuals. Its products serve residential construction, repair and renovation, industrial, and paper end markets.

As of the Q1 2026 earnings date, the company carried a market cap of approximately $4.79 billion (NYSE-listed USD shares) and a negative P/E ratio of -5.17, reflecting the current loss environment. The stock’s 52-week range spans $57.34 to $78.55. West Fraser pays a quarterly dividend of $0.32 per share (annualized $1.28), equating to an approximate dividend yield of ~2.0% at recent prices, despite a negative payout ratio.

Top Financial Highlights

- Total revenue reached $1.334 billion in Q1 2026, increasing sequentially from $1.165 billion in Q4 2025, while declining 8.6% year over year from $1.459 billion in Q1 2025.

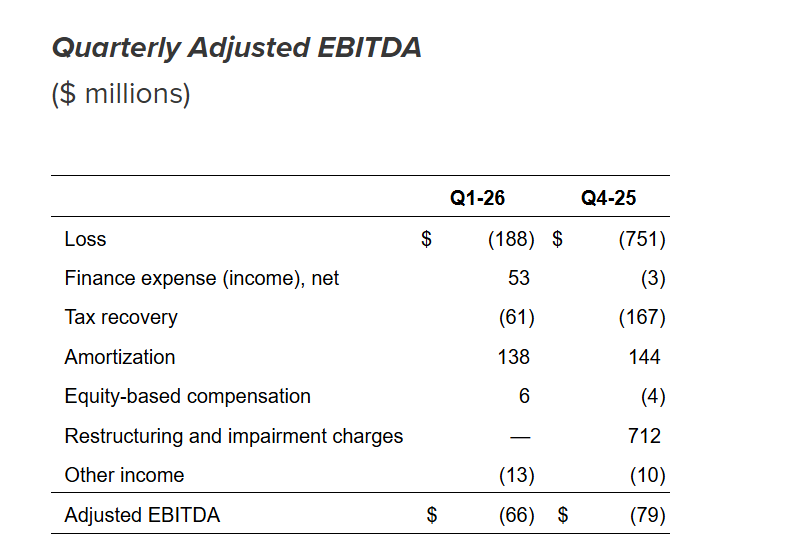

- Net loss stood at $188 million, improving from a loss of $751 million in Q4 2025 but reversing from net income of $42 million in Q1 2025.

- Diluted EPS was -$2.40, compared to -$9.63 in Q4 2025 and $0.46 in Q1 2025.

- Adjusted EBITDA was-$66 million, including a $114 million non-cash charge related to duty adjustments; excluding this, underlying adjusted EBITDA would have been approximately $48 million.

- Gross profit totaled $155 million, declining 42.2% year over year.

- Operating loss was $210 million, reflecting a significant year-over-year increase in losses.

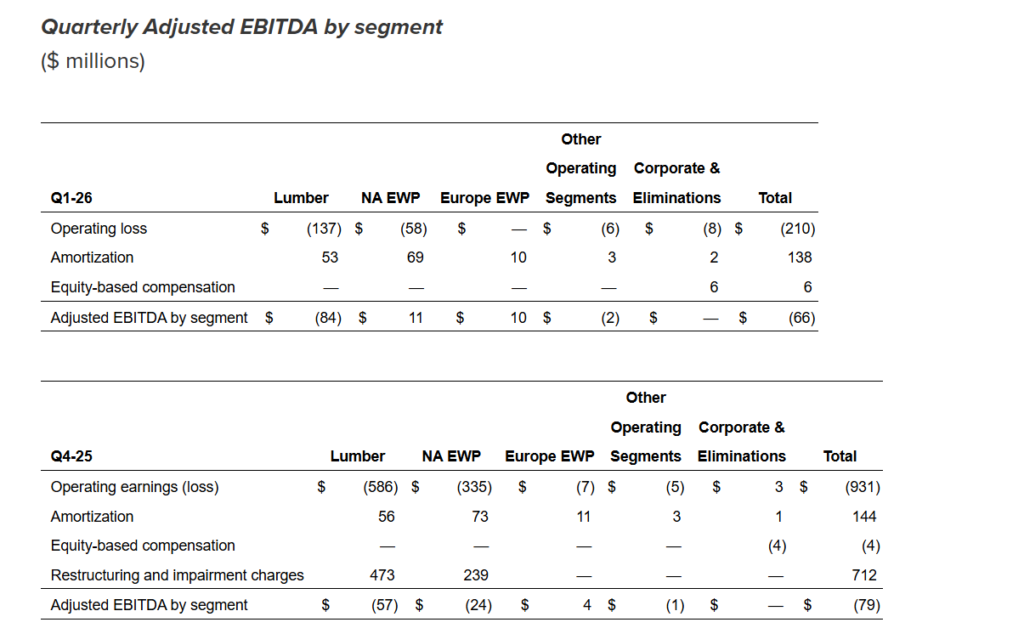

- Lumber segment adjusted EBITDA was -$84 million, impacted by duty charges; excluding these, the segment would have generated approximately $30 million, showing improvement from Q4 levels.

- North America engineered wood products segment reported adjusted EBITDA of $11 million, recovering from a loss in the previous quarter.

- Europe engineered wood products segment generated adjusted EBITDA of $10 million, marking its highest level since Q2 2023.

- Cash and short-term investments stood at $81 million as of April 3, 2026, down from $202 million at year-end 2025.

- Total liquidity was approximately $900 million, including $203 million drawn under a $1 billion credit facility.

- Capital expenditures were $94 million in Q1 2026, with full-year guidance maintained at $300 million to $350 million.

- Dividends paid were $0.32 per share, reflecting two payments during the quarter due to fiscal calendar timing.

Beat or Miss?

| Metric | Reported | Consensus Estimate | Difference / Analysis |

| Diluted EPS | ($2.40) | ($1.24) | Miss by -$1.17; $114M non-cash duty adjustment was primary driver |

| Revenue | $1.334 billion | ~$1.29 billion | Beat by ~$44M; modest outperformance on top line |

| Adjusted EBITDA | -$66 million | N/A | Underlying EBITDA ex-duties was approximately +$48M |

| Net Loss | -$188 million | N/A | Significant deterioration YoY; driven by softwood lumber duty charges |

What Leadership Is Saying?

CEO Sean McLaren on Strategy and Resilience

“In the first quarter of 2026 we benefited from improved commodity pricing and continue to demonstrate the resilience of West Fraser’s diversified portfolio. Although net income was impacted by significant non-cash duty adjustments, these relate to prior year shipments. Excluding the impact of prior year duty adjustments, we were pleased to see all of our core segments — lumber, NA EWP, and Europe EWP — report positive Adjusted EBITDA.”

CFO Chris Verostek on Financials and Capital Allocation

“In Q1, we generated negative $66 million of adjusted EBITDA. As Sean discussed, we had two large softwood lumber duty-related adjustments in Q1, totaling $114 million. Both adjustments are non-cash in nature… Cash flow from operations was impacted by the seasonal build in working capital, resulting in negative $170 million in the first quarter and a net debt position of $457 million. We expect this working capital position to reverse in the second and third quarters.”

Historical Performance: WFG YoY Comparison

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $1,334M | $1,459M | -8.60% |

| Net Income (Loss) | -$188M | +$42M | -547.60% |

| Diluted EPS | ($2.40) | $0.46 | N/M (swing to loss) |

| Adjusted EBITDA | -$66M | +$195M | -133.80% |

| Lumber Segment EBITDA | -$84M | +$66M | N/M (swing to loss) |

| NA EWP Segment EBITDA | +$11M | +$125M | -91.20% |

| Europe EWP Segment EBITDA | +$10M | -$2M | Positive swing |

| Operating Loss | -$210M | +$64M | N/M (swing to loss) |

Note: Q1 2025 Pulp & Paper segment (Adjusted EBITDA of +$7M) was reclassified as “Other” in Q1 2026 and is no longer separately reported.

Competitor Comparison: Q1 2026 vs. Q1 2025

The table below compares West Fraser against its closest publicly traded peer, Weyerhaeuser Co. (NYSE: WY), which also reported Q1 2026 results in late April 2026.

| Category | WFG Q1 2026 | WFG Q1 2025 | WY Q1 2026 | WY Q1 2025 |

| Revenue | $1.334B | $1.459B | $1.727B | ~$1.76B |

| Net Income (Loss) | -$188M | +$42M | +$156M | ~$77M adjusted |

| Diluted EPS | ($2.40) | $0.46 | $0.22 | +$0.11 adj. |

| Adjusted EBITDA | -$66M | +$195M | +$308M | N/A (120% QoQ rise) |

| Revenue YoY Change | -8.60% | N/A | -2% | N/A |

| Key Driver of Variance | $114M duty charge | N/A | Large conservation easement deal | N/A |

Weyerhaeuser’s Q1 2026 EPS of $0.11 (adjusted) beat the Zacks consensus estimate of $0.04 by 175%, contrasting sharply with West Fraser’s EPS miss. Weyerhaeuser’s adjusted EBITDA of $308 million represented a 120% sequential increase, driven significantly by its Strategic Land Solutions segment and a conservation easement transaction. West Fraser’s shortfall was largely attributable to sector-wide softwood lumber duty headwinds specific to Canadian exporters, which are non-recurring in nature.

How the Market Reacted?

West Fraser’s stock (NYSE: WFG) closed at $86.28 on April 29, 2026 (the day of the earnings release), down approximately 1.61% from the prior session. The stock continued its decline over the following two trading days, falling to $86.00 on April 30 and $84.88 on May 1. MarketBeat confirmed the stock opened down approximately 1.5% at $63.00 on the NYSE (USD) the day following the release.

Despite the earnings miss, the market reaction was relatively muted, reflecting the market’s understanding that the steep EPS miss was largely driven by the non-cash, prior-period duty adjustment of $114 million rather than underlying operational deterioration.

Management’s emphasis on a $120 million sequential turnaround in underlying EBITDA (ex-duties) and strong liquidity of ~$900 million provided a degree of reassurance to investors. Sentiment on the report is broadly cautious but not overtly bearish, given the company’s solid balance sheet and the non-recurring nature of the duty charges.