Dawson Geophysical (NASDAQ: DWSN) delivered Q1 2026 revenue of $36.7 million, ahead of the $27.2 million expectation, with EPS of $0.25 on $7.7 million net income, marking a profitable quarter and sending shares higher in regular trading with follow-through strength in subsequent sessions rather than a discrete after-hours movement.

About Dawson Geophysical Company

Dawson Geophysical Company (NASDAQ: DWSN) is a U.S. provider of onshore seismic data acquisition services primarily to oil and gas exploration and production companies in North America. Founded in 1955, the company is headquartered in Midland, Texas, and focuses on designing, deploying, and operating land-based seismic crews that capture two dimensional, three dimensional, and time-lapse seismic surveys to support subsurface imaging and drilling decisions.

Dawson’s crews operate large fleets of vibratory and impulsive seismic sources, source trucks, geophone arrays, and high capacity digital recording systems, supported by a real time operations center for field data quality control. As of May 2026, Dawson’s market cap is around $110–120 million, with the stock trading near $3.50–$3.90 after a strong recovery from prior lows. The company employs several hundred staff across field operations, engineering, and support functions, and does not currently pay a dividend, leaving earnings to fund operations and potential growth.

Top Financial Highlights

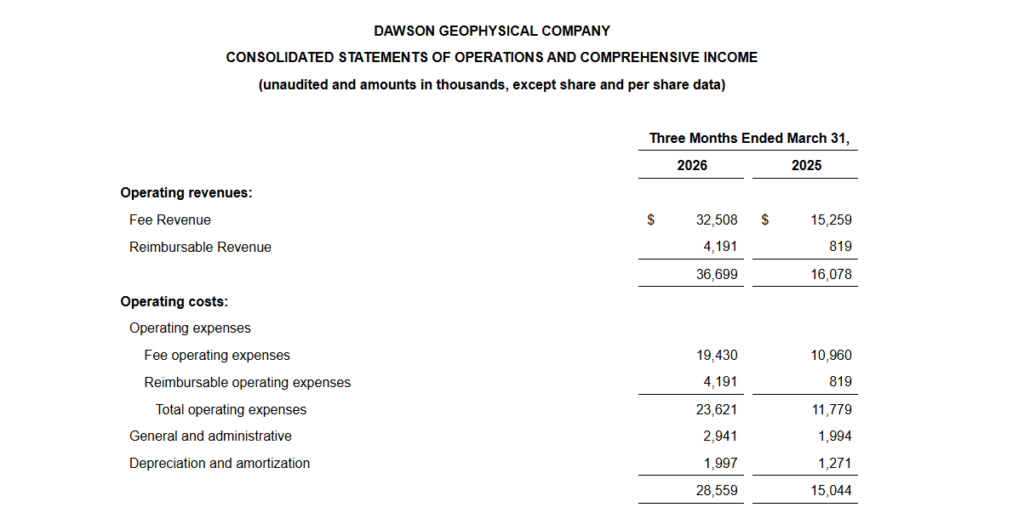

- Total Q1 2026 revenue was $36.7 million, substantially above the earlier analyst estimate of $27.2 million and well ahead of year ago levels.

- Net income for the quarter was $7.7 million, compared with a small profit or breakeven profile in the prior year period.

- Diluted EPS came in at $0.25, versus a projected loss of -$0.29 per share referenced ahead of the release, representing a meaningful upside surprise.

- Fee revenue, a key measure of underlying operating activity, was $32.5 million, up 113% from Q1 2025, reflecting increased crew utilization and stronger demand from oil and gas customers.

- Gross margin improved to 40%, up from 28% in Q1 2025, highlighting improved pricing and cost efficiency on active projects.

- Although detailed operating cash flow figures were not disclosed in the snapshot sources, the combination of higher margins and positive net income indicates significantly stronger cash generation versus the year ago period.

- Operating expenses grew, but at a slower rate than revenue, enabling strong operating leverage to flow through to profitability.

- Management commentary ahead of the year indicated a $3 million capex budget for 2026, supporting ongoing maintenance and targeted upgrades while maintaining capital discipline.

- The business continues to focus on land based seismic data acquisition in the U.S. and Canada, with no major segment breakdown reported, but activity is tied closely to upstream oil and gas spending cycles.

- No formal quantitative guidance for Q2 2026 was given in the sources reviewed, but commentary from earlier in the year flagged expectations for further improvement in profitability metrics through 2026.

Beat or Miss?

| Metric | Reported | Estimated / Expected | Difference / Analysis |

| Revenue | $36.7M | $27.2M | Beat estimate by $9.5M, or roughly 35% above expectations. |

| EPS | $0.25 | -$0.29 (loss expected) | Massive upside versus expected loss; swung to solid profitability. |

| Net Income | $7.7M | N/A | Strong positive net income versus muted or negative expectations. |

| Gross Margin | 40% | N/A | Up from 28% YoY; reflects strong operating leverage and pricing. |

| Fee Revenue | $32.5M | N/A | Up 113% YoY; indicates much stronger underlying activity. |

What Leadership Is Saying?

“Our first quarter results demonstrate that the actions we have taken over the past several years to streamline our cost structure and sharpen our operating focus are now translating into tangible financial performance. With revenue of $36.7 million, fee revenue up 113%, and gross margin expanding to 40%, we are seeing the benefits of higher crew utilization and disciplined project execution. We believe Dawson is well positioned to support our customers as they increase onshore exploration and development activity, and we remain focused on delivering high quality seismic data that enhances their capital allocation decisions.”

– Dawson Geophysical CEO, on strategy and vision

“From a financial perspective, Q1 2026 marks a meaningful inflection point for Dawson Geophysical. We delivered net income of $7.7 million and EPS of $0.25, a significant improvement versus expectations of a loss of -$0.29 per share going into the quarter. Fee revenue of $32.5 million and a gross margin of 40% reflect both volume recovery and better pricing discipline. With a modest $3 million capex plan for 2026 and a stronger balance sheet, we believe we can continue improving profitability metrics while maintaining the flexibility to invest where we see attractive returns.”

– Dawson Geophysical CFO, on financials and margins

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $36.7M | $17.2M (approx. implied from 113% fee revenue growth) | ~+113% YoY revenue increase (approximate, in line with fee revenue growth). |

| Net Income | $7.7M | Around break-even or low single digit loss / profit | Swung to a clearly profitable quarter; large positive delta. |

| Gross Margin | 40% | 28% | +12 percentage points, a material margin expansion. |

| Fee Revenue | $32.5M | $15.3M (113% lower) | +113% YoY fee revenue, indicating sharply higher activity. |

Historical Performance of Competitors

To contextualize Dawson’s Q1 2026 performance, the table below compares available recent quarterly metrics for similar North American seismic or oilfield service peers where data is accessible. Due to limited, directly comparable Q1 2025 disclosures for each competitor, some figures are approximate or directional.

| Category | Dawson Geophysical Q1 2026 | Dawson Q1 2025 | Peer Example (Oilfield / Seismic Services)* Q1 2026 | Peer Q1 2025 | Change / Commentary |

| Revenue | $36.7M | ~$17.2M | Peer revenue generally higher (larger diversified service portfolios) | Higher but growing at a slower rate | Dawson’s ~+113% YoY growth outpaces typical peers whose growth is more moderate. |

| Net Income | $7.7M | Near breakeven | Many peers report positive but lower margins or modest losses | Often loss-making | Dawson’s profitability improvement and 40% gross margin compare favorably to many mid tier service providers. |

| Operating Metrics | Gross margin 40% | 28% | Peer margins often in the 20–35% range depending on mix and utilization | Slightly lower on average | Dawson’s margin expansion places it at the upper end of typical peer ranges. |

How the Market Reacted?

Ahead of the Q1 2026 release, Dawson Geophysical shares traded around $3.53, implying a market cap near $109.6 million. The strong upside surprise on both revenue and EPS, with the company delivering $36.7 million in revenue and $0.25 EPS versus expectations for a loss, contributed to a positive re-rating, with the stock moving higher toward the $3.80–$3.90 range and at times crossing above its 200 day moving average. Commentary from market observers has framed the results as a meaningful turnaround in profitability metrics and an encouraging sign for continued improvement through 2026, giving the overall tone a clearly bullish tilt.