Vipshop (NYSE: VIPS) reported Q1 2026 EPS of $0.65 (GAAP) / $0.68 (Non-GAAP), beating analyst consensus of $0.64 by 6.25%. Total net revenues reached RMB26.6 billion (US$3.9 billion), up 1.2% year-over-year, broadly in line with expectations. Net income jumped 13.6% YoY. After-hours market movement remained modest and the stock traded near pre-earnings levels around $14.20.

About Vipshop Holdings Limited

Vipshop Holdings Limited (NYSE: VIPS) is a leading off-price retailer in China, founded in 2008 and headquartered in Guangzhou, Guangdong Province. The company offers high-quality branded products to consumers throughout China at deep discounts through both online and offline channels, including its flagship Vipshop App, vip.com website, Vipshop WeChat Mini-Program, and its Shan Shan Outlets retail network. Since its IPO on the New York Stock Exchange in March 2012, Vipshop has built a loyal customer base of 41.7 million active customers as of Q1 2026.

As of May 2026, VIPS traded near $14.20 per share with a 52-week range of $13.36 to $21.08, and a consensus analyst price target of approximately $19.53 to $20.14, implying significant upside from current levels. The company is primarily focused on the brand-discount apparel and lifestyle segment within China’s vast e-commerce landscape, where it competes with giants such as Alibaba, JD.com, and Pinduoduo. Analysts tracking the stock hold a consensus “Buy” rating, with 8 buy ratings, 2 hold ratings, and 0 sell ratings.

Top Financial Highlights

- Total net revenues reached RMB26.6 billion (US$3.9 billion), increasing 1.2% year over year from RMB26.3 billion in Q1 2025.

- Gross merchandise value totaled RMB56.9 billion, rising 8.6% from RMB52.4 billion in the prior-year period.

- Gross profit increased to RMB6.5 billion (US$941.6 million), up 6.8% year over year.

- Gross margin improved to 24.4%, compared to 23.2% in Q1 2025.

- GAAP net income attributable to shareholders reached RMB2.2 billion (US$319.8 million), increasing 13.6% year over year.

- Non-GAAP net income attributable to shareholders was RMB2.31 billion (US$334.2 million), remaining broadly stable year over year.

- GAAP diluted EPS per ADS stood at RMB4.48 (US$0.65), compared to RMB3.72 in Q1 2025.

- Non-GAAP diluted EPS per ADS increased to RMB4.68 (US$0.68), up from RMB4.43 in the prior-year quarter.

- Income from operations totaled RMB2.5 billion (US$362.1 million), rising 9.7% year over year, with operating margin improving to 9.4% from 8.7%.

- Cash, cash equivalents, and restricted cash stood at RMB28.3 billion (US$4.1 billion) as of March 31, 2026.

- Short-term investments totaled RMB2.7 billion (US$389.2 million).

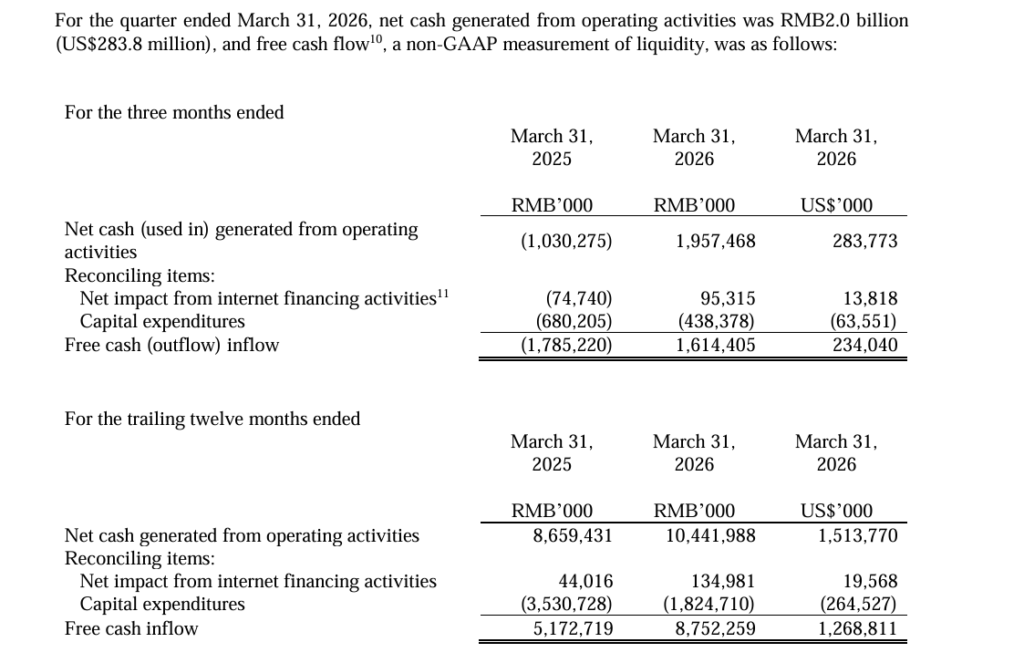

- Net cash generated from operating activities was RMB2.0 billion (US$283.8 million), compared to an outflow in Q1 2025.

- Active customers reached 41.7 million, increasing 0.9% year over year.

- Total orders grew to 172.6 million, up 3.2% from 167.2 million in the prior-year period.

- Q2 2026 revenue guidance is projected between RMB24.5 billion and RMB25.8 billion, representing a year-over-year change ranging from a 5% decline to flat growth.

Beat or Miss?

| Metric | Reported | Estimated/Expected | Difference / Analysis |

| Non-GAAP EPS (per ADS) | $0.68 | $0.64 | Beat by +6.25% |

| GAAP EPS (per ADS) | $0.65 | ~$0.58 (GAAP estimate) | Beat consensus |

| Total Net Revenue | RMB 26.6B (US$3.9B) | ~$3.85B–$3.88B | Broadly in line; slight beat vs. $3.85B estimate |

| Gross Margin | 24.40% | N/A (not in consensus) | Improved from 23.2% YoY |

| Operating Margin | 9.40% | N/A | Up from 8.7% YoY |

| GMV | RMB 56.9B | N/A | Up 8.6% YoY – meaningfully ahead of net revenue growth |

| Q2 2026 Revenue Guidance | RMB 24.5B–25.8B | N/A | Implies -5% to 0% YoY, signaling cautious near-term outlook |

What Leadership Is Saying?

CEO – Eric Shen on Strategy and Growth

“Our first-quarter performance was driven by strong apparel sales, supported by a successful Chinese New Year holiday when consumers responded enthusiastically to our seasonal, value-for-money collections. Our SVIP customer base achieved solid growth in both number and contribution, reflecting our long-standing appeal to high-value consumers. Alongside these results, we have made steady progress across our merchandising portfolio, customer engagement, and AI integration, all of which are helping to further leverage our off-price retail model for growth. With continued dedication to the brand-discount space, we remain confident in our ability to deliver sustainable, profitable growth over the long term.”

CFO – Mark Wang on Financials and Margins

“We delivered an in-line quarter, reflecting a pull-forward of demand around the Chinese New Year, which concentrated activity in the first two months. Margins remained healthy and stable, supported by a stronger mix of higher-margin categories and disciplined operations. In April, we completed our annual dividend payout, and remain committed to delivering on our full-year shareholder return promises. With a solid financial position and consistent execution, we are well positioned to fund our strategic initiatives and business growth, while driving value for our shareholders.”

Historical Performance: Q1 2026 vs. Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Net Revenue | RMB 26.6B (US$3.9B) | RMB 26.3B | +1.2% |

| Gross Profit | RMB 6.5B (US$941.6M) | RMB 6.1B | +6.8% |

| Gross Margin | 24.40% | 23.20% | +120 bps |

| Net Income (Vipshop shareholders) | RMB 2.2B (US$319.8M) | RMB 1.9B | +13.6% |

| Non-GAAP Net Income (shareholders) | RMB 2.31B (US$334.2M) | RMB 2.31B | Flat (0%) |

| Income from Operations | RMB 2.5B (US$362.1M) | RMB 2.3B | +9.7% |

| Operating Margin | 9.40% | 8.70% | +70 bps |

| Total Operating Expenses | RMB 4.2B (US$603.8M) | RMB 4.0B | +3.6% |

| GMV | RMB 56.9B | RMB 52.4B | +8.6% |

| Active Customers | 41.7 million | 41.3 million | +0.9% |

| Diluted EPS (GAAP, per ADS) | RMB 4.48 (US$0.65) | RMB 3.72 | +20.4% |

| Non-GAAP Diluted EPS (per ADS) | RMB 4.68 (US$0.68) | RMB 4.43 | +5.6% |

| Free Cash Flow (quarterly) | RMB 1.61B (US$234M) | -RMB 1.79B (outflow) | Turned positive |

Competitor YoY Performance: Q1 2026 vs. Q1 2025

| Company | Metric | Q1 2026 | Q1 2025 | Change (%) |

| Vipshop (VIPS) | Net Revenue | RMB 26.6B (US$3.9B) | RMB 26.3B | +1.2% |

| Vipshop (VIPS) | Net Income | RMB 2.2B (US$319.8M) | RMB 1.9B | +13.6% |

| Vipshop (VIPS) | Gross Margin | 24.40% | 23.20% | +120 bps |

| JD.com (JD) | Net Revenue | RMB 315.7B (US$45.8B) | RMB 301.1B | +4.9% |

| JD.com (JD) | Net Income (GAAP) | RMB 5.1B (US$0.7B) | RMB 10.9B | -53.2% |

| JD.com (JD) | Non-GAAP Net Income | RMB 7.4B (US$1.1B) | RMB 12.8B | -42.2% |

| Alibaba (BABA) | Net Revenue (Mar Q) | RMB 243.4B (US$35.3B) | ~RMB 236.5B est. | +3.0% |

| Alibaba (BABA) | Non-GAAP Net Income | RMB 86M (US$12M) | ~RMB 29B | -99.70% |

| Alibaba (BABA) | GAAP Net Income | RMB 25.5B (US$3.7B) | N/A | +96% YoY |

Note: Alibaba’s fiscal year ends March 31, so its March 2026 quarter represents Q4 FY2026 – the same calendar period as Vipshop’s Q1 2026. Alibaba’s massive non-GAAP income collapse reflects heavy investment in AI infrastructure, quick commerce, and cloud expansion, not operational deterioration. JD.com’s net income decline was driven by food-delivery segment losses, though JD Retail’s operating margin improved to 5.6%.

How the Market Reacted?

Vipshop stock (NYSE: VIPS) was trading near $14.20 in the session preceding the May 21, 2026 earnings announcement, slightly above its recent multi-month low of $13.36. The Q1 2026 results beat Non-GAAP EPS estimates by 6.25% and revenue landed broadly in line with the $3.85 billion consensus, which tends to support a neutral to slightly positive post-earnings reaction.

The management’s conservative Q2 guidance – projecting revenues to potentially decline as much as 5% year-over-year due to a Chinese New Year demand pull-forward – is likely to weigh on near-term sentiment despite the solid underlying margin improvement. With a consensus analyst price target near $19.53–$20.14 versus a pre-announcement price of ~$14.20, the stock remains deeply discounted relative to analyst fair value, and Barclays reaffirmed its Buy rating on VIPS as recently as April 2026.