Introduction

Snowflake Statistics: The company Snowflake, Inc. achieves fast growth because it operates in a market where data increases and artificial intelligence and cloud computing technologies dominate. Snowflake transformed data management because its AI Data Cloud platform provides customers with financial success and new ways to handle and study large datasets. The year 2025 represented a pivotal phase in the company’s growth story, underpinned by robust revenue growth, expanding enterprise adoption, and strategic AI investments.

The article investigates Snowflake Statistics, which occurred during 2025, by examining its revenue results and growth rates, customer volume increase, retention performance, future financial obligations, and industry research background.

Editor’s Choice

- The Total Addressable Market (TAM) for Snowflake Inc. will increase from USD 170 billion in CY24 to USD 355 billion by CY29.

- The annual product revenue achieved strong multi-year growth by increasing from USD 1.94 billion in FY23 to USD 3.46 billion in FY25.

- Quarterly revenue increased from USD 900 million in Q3 FY25 to USD 1.16 billion in Q3 FY26.

- The Remaining Performance Obligations (RPO) grew by 37% year-over-year to reach USD 7.88 billion in Q3 FY26.

- The company expects that 48 to 50% of RPO will change into revenue during the next 12 months.

- The customer base grew from 10,490 to 12,621 during the year, which represents about 20% growth and more than 2,100 new customers who joined the company.

- The number of customers who generated more than USD 1 million in annual product revenue rose by 29% year-on-year from 534 to 688.

- Net Revenue Retention (NRR) maintained stable operation at 120% throughout the period until it reached 125% during Q3 FY26.

- The company achieved a gross profit of USD 2.41 billion in FY25.

- The product gross margin decreased to 71%, which represented a 3% decline from the previous 74%.

- The operating cash flow for the company increased to USD 959.8 million during FY25, which showed a 76% growth from the two years before this time.

- Free cash flow of USD 884.1 million during FY25, which demonstrated its progress in managing capital resources while maintaining strong cash reserves.

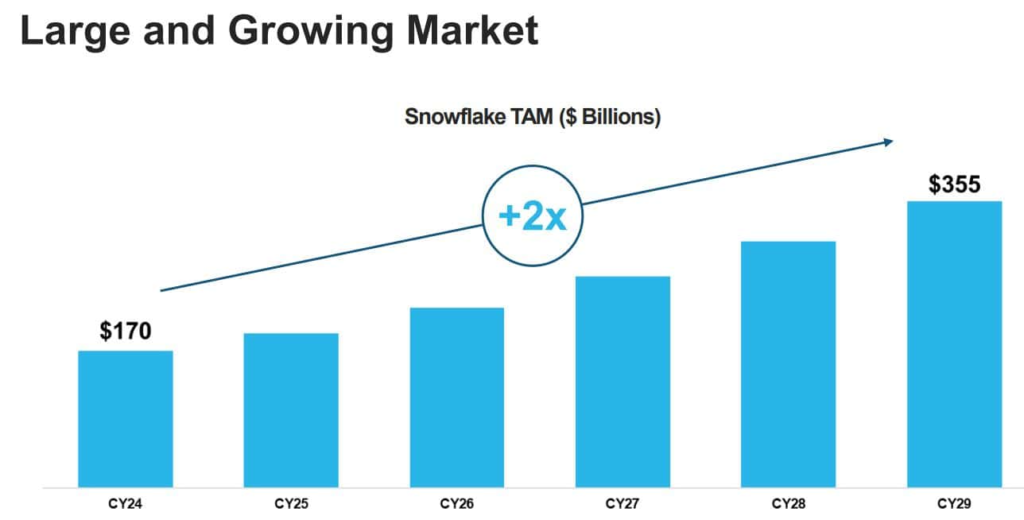

Snowflake Growing Market

(Source: q4cdn.com)

- The chart demonstrates a strong potential for future expansion, which will continue through time.

- Snowflake’s Total Addressable Market (TAM) is projected to expand from USD 170 billion in CY24 to USD 355 billion by CY29, representing more than 2x growth within five years.

- The continuous upward trend shows that enterprises are increasingly adopting cloud services while integrating AI technologies, and users are consuming more data worldwide.

- The business expansion creates new ways to generate revenue, which enables the company to continuously increase its revenue streams.

- The growing Total Addressable Market (TAM) of Snowflake shows that there will be continued demand for the company’s products.

- The market size of Snowflake has increased two times, which indicates that investors should expect industry growth that will last beyond short-term market trends.

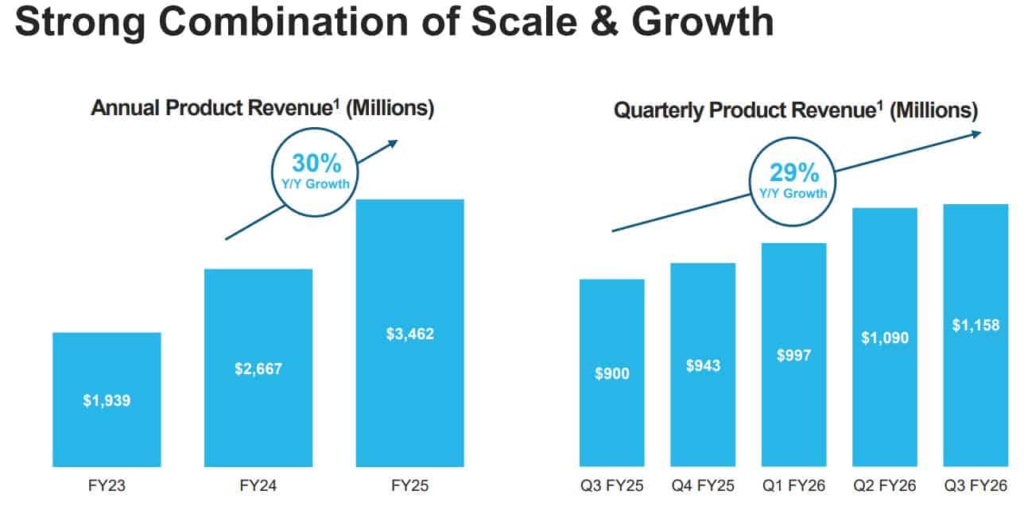

Snowflake Product Revenue

(Source: q4cdn.com)

- Annual product revenue increased from USD 1.94 billion in FY23 to USD 2.67 billion in FY24 and reached USD 3.46 billion in FY25, which demonstrates ongoing business expansion because it generates 30% annual revenue growth.

- The present multi-billion-dollar expansion demonstrates that enterprises choose to adopt Snowflake services according to all Snowflake business data.

- The quarterly performance establishes the validity of this growth story. Revenue grew from USD 900 million in Q3 FY25 to USD 1.16 billion in Q3 FY26, which shows a 29% increase compared to the previous year.

- The consistent sequential rise—from USD 943 million to USD 997 million, then USD 1.09 billion and USD 1.16 billion—demonstrates durable consumption demand and improving customer spend patterns.

- The platform demonstrates customer loyalty because Snowflake’s revenue numbers keep increasing both annually and quarterly.

- The data shows Snowflake is moving from a period of fast growth to a stage of sustainable operational growth, according to investors monitoring Snowflake’s performance data.

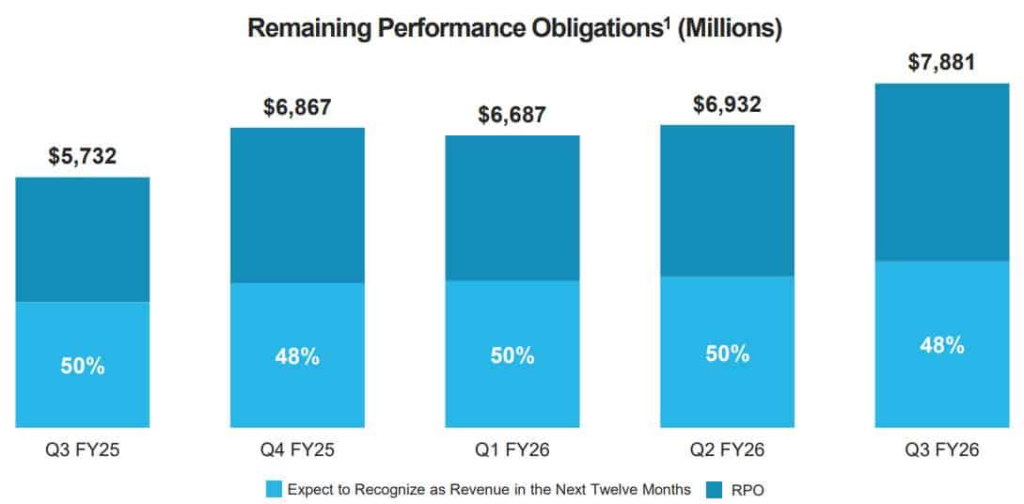

Snowflake’s Expanding Contracted Revenue Pipeline

(Source: q4cdn.com)

- The chart demonstrates how forward revenue visibility improves because Remaining Performance Obligations (RPO) numbers keep increasing.

- Snowflake’s RPO grew from USD 5.73 billion in Q3 FY25 to USD 7.88 billion in Q3 FY26, which represents a 37% year-over-year growth.

- The continuous growth demonstrates that companies are making deeper commitments through extended contract periods, which serve as vital metrics to measure Snowflake’s overall performance.

- The quarterly progress demonstrates increasing momentum because RPO increased from USD 6.87 billion in Q4 FY25 to USD 6.93 billion in Q2 FY26.

- The RPO contains about 48 to 50 % of its value, which will be recognized as revenue during the upcoming 12-month period, which displays strong potential for short-term revenue conversion.

- The increasing RPO value brings strategic advantages because it enhances revenue predictability while maintaining valuation stability.

- The contracted backlog at this level shows customer certainty about their future platform usage according to Snowflake’s complete statistical data.

- The continuous RPO growth proves that investors can expect Snowflake demand to continue while the company achieves better sales results and larger revenue growth from its major clients.

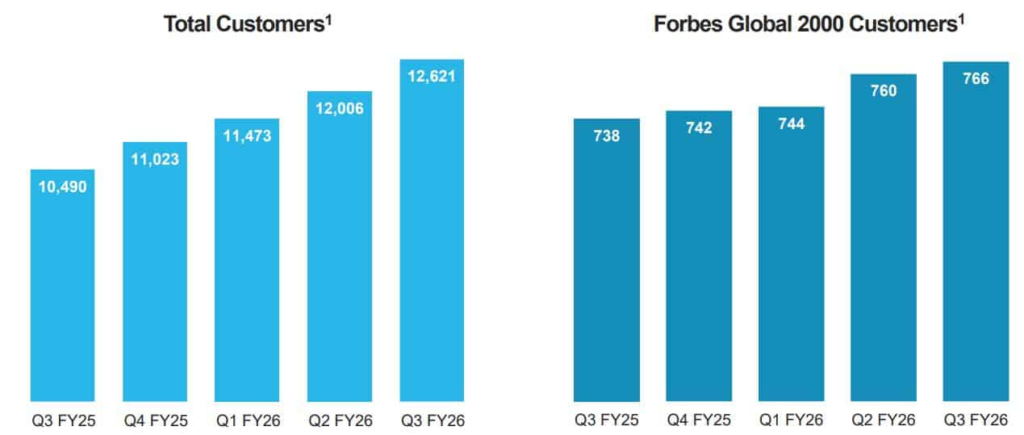

Snowflake Total Customers

(Source: q4cdn.com)

- The chart demonstrates that businesses are expanding their market presence while their established brands maintain a strong reputation.

- Total customers increased from 10,490 in Q3 FY25 to 12,621 in Q3 FY26, which shows growth of more than 2,100 new customers.

- The period between 11,023 and 12,621 shows that demand for the product has increased while more businesses have started using it in different sectors.

- Large global enterprises need to achieve traction because it provides essential value. The number of Forbes Global 2000 customers increased from 738 to 766 during that time period, which shows the company has established stronger connections with major worldwide businesses.

- The strategic aspect of customer growth proves beneficial because it boosts revenue stability through improved cross-selling possibilities, which occur when Global 2000 clients become active customers.

- The Snowflake statistics show that customer expansion acts as the primary growth indicator for investors who want to see sustainable business development.

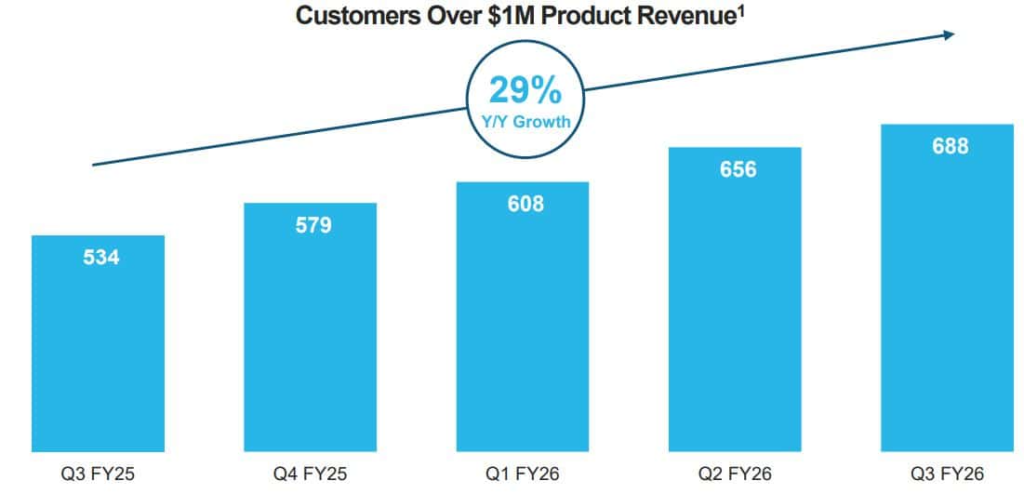

Snowflake Accelerating High-Value Customer Expansion

(Source: q4cdn.com)

- The chart demonstrates that Snowflake Inc. shows strong growth in its ability to generate revenue through enterprise monetization.

- The number of customers who produced more than USD 1 million in product revenue increased from 534 to 688 between Q3 FY25 and Q3 FY26, which resulted in the company acquiring 154 new high-value customers during that period.

- Through the year-to-year growth rate of 29%, which shows both platform retention and increasing company use of the platform, the platform shows that businesses prefer to use the system.

- The quarterly results show continuous development because the numbers increased from 534 to 579 and then to 608 and 656 before reaching 688.

- The company sustains its growth through regular upselling activities while gaining more customer spending power than through infrequent large contract agreements.

- The demand pattern shows persistence through the period from Q3 FY25 to Q4 FY25, which shows a 10% increase followed by steady mid-single-digit growth for the subsequent quarters.

- Snowflake’s performance data shows high customer retention, which enables businesses to handle increasing data processing requirements.

- The business relationship between customers who spend more than USD 1 million annually and their companies exists because high switching costs and established analytics systems create long-term strategic ties.

- The company achieves revenue growth through its operational model, which creates stable financial results over an extended period.

- The process of acquiring large clients every three months creates a positive impact on the company’s lifetime value indicators through multiplicative growth.

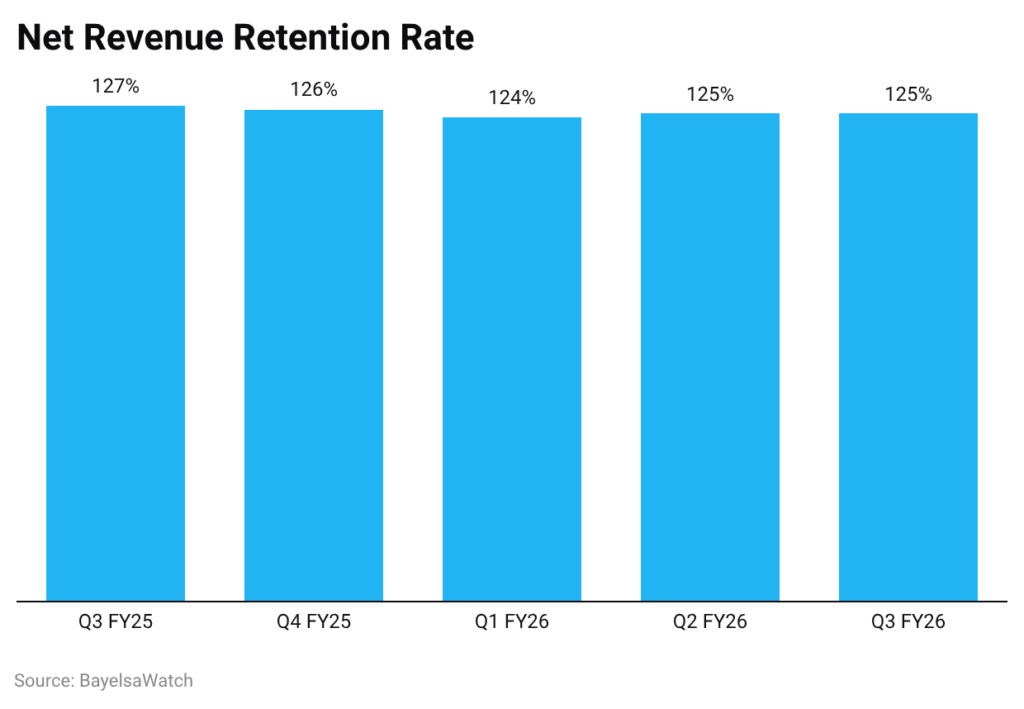

Snowflake Net Revenue Retention Rate

(Reference: q4cdn.com)

- Snowflake Inc. demonstrates superior expansion capacity through its net revenue retention NRR performance.

- The company reports NRR of 127% in Q3 FY25, 126% in Q4 FY25, 124% in Q1 FY26, and stabilizing at 125% through Q2 and Q3 FY26.

- The company demonstrates strong upsell capacity with low customer attrition because it has maintained customer retention above 120% during five consecutive quarters.

- Existing customers at Snowflake increased their spending by 25% during the year because the company achieved 125% NRR despite losing some customers who downgraded.

- The usage data from Snowflake shows that their products achieve permanent market acceptance while their enterprise clients experience increasing data processing requirements.

- The expansion rate has decreased from 127% to 124-125%, which shows a return to standard operating conditions after reaching the highest level of development.

- The persistent pattern of demand shows fundamental market requirements instead of short-term growth tendencies.

- Snowflake now competes with top SaaS companies because its retention rate exceeds 120%, which represents the industry standard for excellence.

- The Snowflake statistics show that existing customers drive predictable revenue growth, which does not require the company to depend on acquiring new clients.

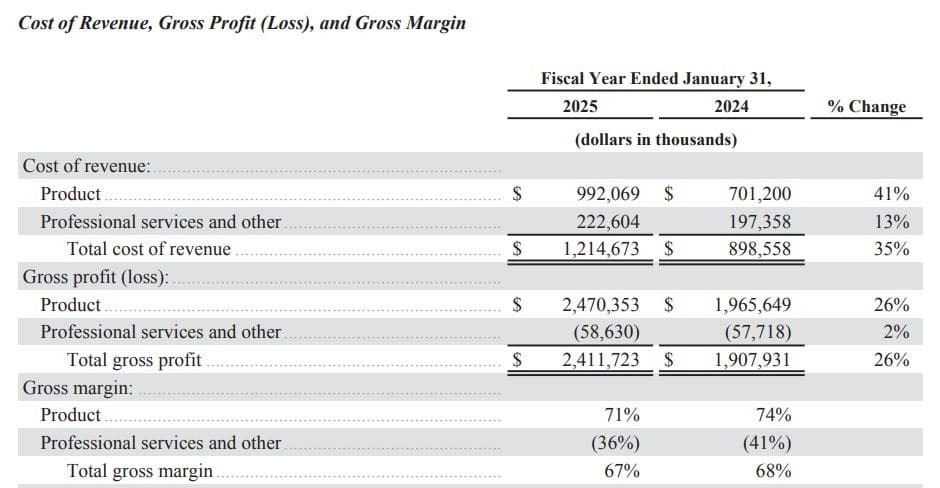

Snowflake Profitability Performance

(Source: q4cdn.com)

- Public Company has released its latest financial report, which demonstrates its controlled business growth strategy while maintaining its ongoing investment activities.

- The company reported a 35% increase in total revenue expenses, which reached 1.21 billion dollars after growing from 898.6 million dollars.

- The cost of products increased to 992.1 million dollars, which represented a 41% rise, while professional services costs increased to 222.6 million dollars, which demonstrated a limited growth of 13% because the company concentrated on delivering its main platform service.

- The company achieved a 26% increase in gross profit, which amounted to 2.41 billion dollars after it had reported 1.91 billion dollars.

- The product gross profit increased 26% to 2.47 billion dollars, which showed that the company achieved effective revenue generation.

- The total gross margin decreased from 68% to 67% because product margin dropped from 74% to 71%.

- Professional services showed a negative performance of 36% but improved from the previous 41% level, which showed that the company achieved better operational performance.

- The infrastructure spending data from Snowflake shows that the company has increased its expenditures to meet demand while its profitability remains stable.

- The margin compression that occurred throughout the period appears to follow an intentional pattern instead of an inherent business framework.

- Snowflake data demonstrates that strong operating leverage exists for the company because its revenue growth exceeds the pace at which its long-term expenses reach their typical levels, which will enable the company to maintain higher profit margins as it grows.

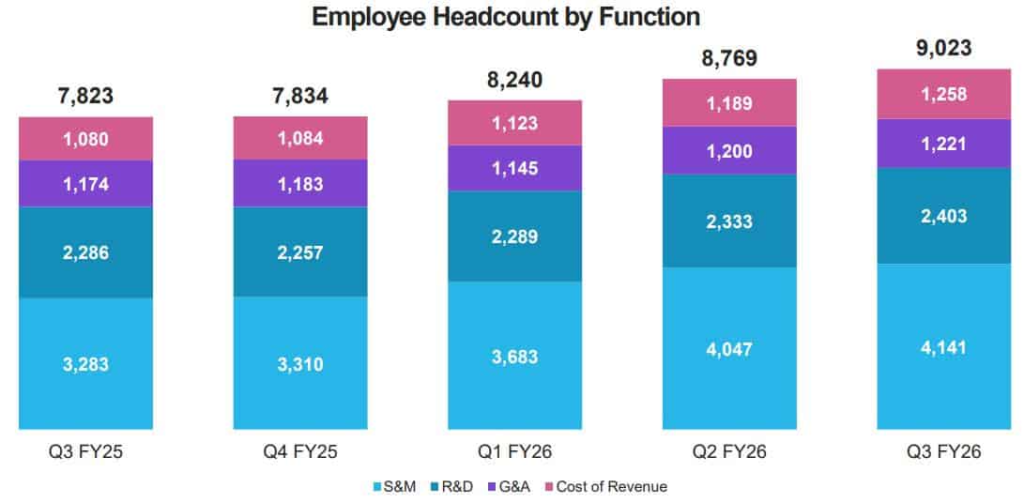

Snowflake Employee Head Count By Function

(Source: q4cdn.com)

- Snowflake Inc. shows its workforce pattern through controlled operational growth that matches its development requirements.

- The total number of employees grew from 7,823 in Q3 FY25 to 9,023 in Q3 FY26, which means that 1,200 new employees joined the company, and this number represents approximately 15% of the total employees.

- The company achieves steady growth because its revenue increases at the same time as it keeps its operational activities steady.

- The Sales & Marketing (S&M) department has become the biggest operational unit since it added 858 staff members to reach a total of 4,141 workers from 3,283 staff members.

- The company demonstrates its commitment to worldwide market development and its determination to establish its presence in new business sectors.

- Research & Development (R&D) grew from 2,286 to 2,403 employees, which shows that the company continues its innovation efforts, although the company implements its work at a slow speed approximately 5 % of total expansion.

- The General & Administrative (G&A) expenses increased from 1,174 to 1,221 through controlled overhead management, which showed disciplined expense handling.

- The Cost of Revenue department needed to increase its workforce from 1,080 employees to 1,258 employees because the department needed to meet infrastructure demands and service delivery requirements.

- The S&M department has increased its share of total staff because the company needs to acquire new customers.

- The Snowflake statistics show how the organization develops its workforce to meet business needs while achieving operational success and maintaining long-term profit margins.

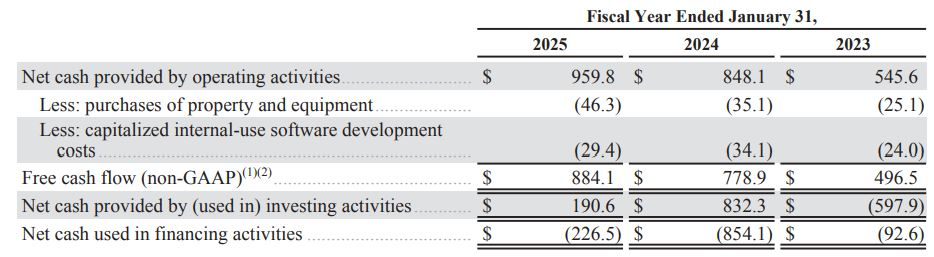

Snowflake Free Cashflow

(Source: q4cdn.com)

- Snowflake Inc. exhibits financial strength and efficient capital spending through its cash flow operations.

- Net cash provided by operating activities climbed to USD 959.8 million in FY2025, up from USD 848.1 million in FY2024 and USD 545.6 million in FY2023—marking a two-year increase of roughly 76%.

- The company demonstrates its ability to manage operations through increasing operational capacity and effective management of working capital.

- Free cash flow (non-GAAP) reached USD 884.1 million in FY2025 after deducting USD 46.3 million for property and equipment purchases and USD 29.4 million for capitalized software development expenses.

- The current value stands at USD 778.9 million for FY2024, while the previous year showed USD 496.5 million for FY2023—the two-year period experienced an impressive 78% growth.

- Snowflake demonstrates its capability to transform revenue growth into actual cash through these financial metrics.

- The company experienced USD 190.6 million in cash from investing activities during FY2025 after experiencing previous financial instability, while financing activities showed net cash outflows of USD 226.5 million because of capital structure changes.

- The Snowflake statistics demonstrate a business that has moved from rapid expansion to its current phase of developing consistent revenue streams, which generate cash.

- The company achieves strategic flexibility through improved free cash flow, which also enhances its financial stability and creates value for shareholders over time.

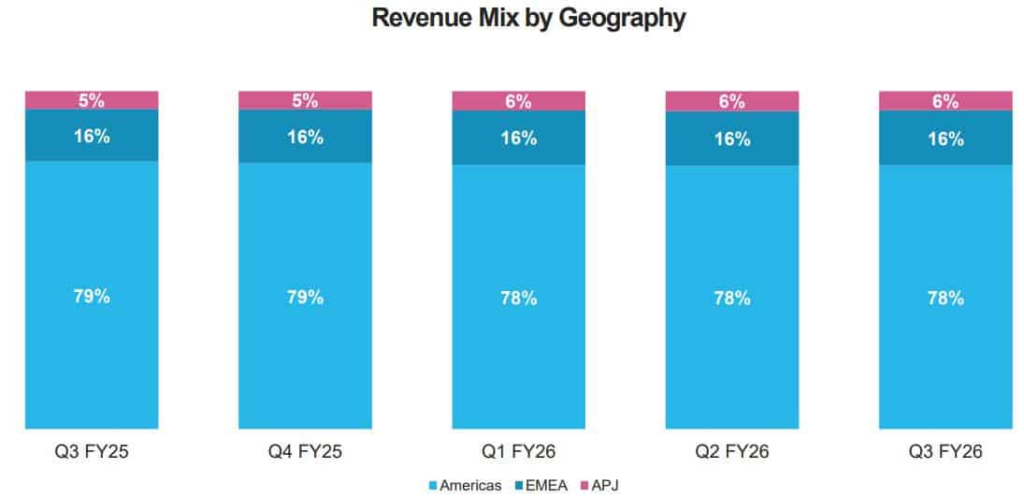

Snowflake Global Revenue By Region

(Source: q4cdn.com)

- The revenue composition at Snowflake Inc. demonstrates both dominance in core markets and steady international penetration.

- The Americas consistently contribute 78–79% of total revenue across five consecutive quarters, underscoring the company’s strong North American enterprise footprint.

- EMEA maintains a constant 16% share of total revenue, while APJ (Asia-Pacific and Japan) has increased its share from 5% to 6%, which indicates that the company is slowly entering new markets.

- The Americas generate approximately 80% of total revenue, but the company experiences a slight revenue change because of its early-stage business expansion into high-value digital markets in APJ. The geographic distribution from Q3 FY25 to Q3 FY26 showed stable weather patterns because it indicated both predictable demand patterns and low regional volatility.

- Snowflake statistics show that the company is expanding its global operations, yet it still faces revenue concentration issues because most of its revenue comes from the Americas.

- The company can achieve better revenue stability through EMEA and APJ share growth, which will help it reduce dependence on one region.

Challenges and Future Growth

- Snowflake achieved outstanding results during 2025, which generated substantial profits for its investors.

- The company’s stock experienced a 70 % increase throughout the year because of strong earnings results and positive future predictions.

- The broader performance trend showed increasing investor confidence because the company did not achieve all of its projections to the highest market level.

- The company received positive market reactions because enterprise cloud adoption increased, and artificial intelligence products showed rapid development.

- The company currently encounters various natural challenges that typically affect organizations in their growth phase.

- Snowflake experienced stock price fluctuations because of financial projections that fell short of the aggressive targets set by investors.

- It needs to develop its platform and product offerings while balancing fast innovation with effective business operations, according to its main strategic goal.

Conclusion

Snowflake Statistics: Snowflake evolved from its initial startup phase as a cloud data company in 2025 to become a complete business platform that enables worldwide organizations to access their data assets. Snowflake has become a fundamental component of corporate data systems because it generates billions in yearly revenue while maintaining strong customer loyalty and increasing its use by businesses through its focus on AI-powered data solutions.

The company faces two main obstacles because its cloud services face price competition and investors expect certain financial outcomes, but its technological progress, together with its market presence, indicate strong growth potential. The statistics from Snowflake 2025 show that the company operates at the forefront of the data revolution because organizations today shift toward using data for decision-making, automation, and AI solutions.

FAQ

Snowflake Inc. forecasts its total addressable market to increase from 170 billion dollars in calendar year 2024 to 355 billion dollars by calendar year 2029, which represents more than a twofold growth during the five years.

Snowflake achieved product revenue of 3.46 billion dollars for FY25, which showed 30% growth compared to the previous year.

The company reported 1.16 billion dollars in revenue for Q3 FY26, which represented a 29% increase over Q3 FY25.

Remaining performance obligations reached 7.88 billion dollars in Q3 FY26, which represented a 37 % increase from the previous year.

Snowflake had 12621 customers during Q3 FY26, which included more than 2100 new customers who joined since the previous year.

The number of customers generating over 1 million dollars in product revenue grew to 688 during Q3 FY26, which showed a 29 % yearly increase.