Introduction

Student Loan Burden and Repayment Statistics: Student loans help many people pay for college, but they can also become a heavy burden after graduation. Tuition and living costs continue to rise, so students borrow more than ever. Later, monthly payments, interest, and long repayment periods can create stress and limit major life decisions such as buying a home, starting a family, or changing jobs.

For some, even a steady salary isn’t enough to feel secure. This article examines the meaning of the student loan burden, why repayment can be difficult, and who bears it most. It also explains repayment plans and simple ways to manage debt, avoid missed payments, and stay on track financially.

Editor’s Choice

- Total student loan debt is approximately USD 1.833 trillion (latest compiled estimate, updated February 2, 2026).

- As of 2025, California has the highest total student debt, at USD 154.50 billion.

- 54.7% of total federal student loan debt is from Stafford Loans (18% subsidized and 36.7% unsubsidized), while 31.6% is held in Direct Consolidation Loans.

- Private student loans typically account for less than 10% of total student loan debt.

- In 2026, among 61,000 respondents, borrowers took an average of more than 20 years to repay their student loans fully.

- Approximately 20% of U.S. adults with an undergraduate degree currently have outstanding student loan debt.

- The share of adults who have ever borrowed student loans for their own education is 42% among adults aged 18-29 (35% still owe, and 7% have fully repaid).

- Borrowers with at least USD 25,000 debt increased to 23% for some college or technical degree holders.

- New Hampshire averages USD 39,928 in debt, while Utah averages USD 18,344, a USD 21,584 gap, about 118%.

- In 2025, although major income-driven repayment forgiveness programs were paused due to legal challenges, approximately 121,000 borrowers still received federal student loan forgiveness.

Student Loan Debt Statistics

- According to EducationData.org, total student loan debt is approximately USD 1.833 trillion (latest compiled estimate, updated February 2, 2026).

- Federal student loans account for the largest share: the outstanding federal balance is USD 1.693 trillion, and 42.8 million borrowers currently have federal student loan debt.

- Federal loans account for 90.9% of all student loan debt, while private loans account for 9.13%, including approximately USD 29.7 billion in student loan refinancing debt.

- The average federal student loan balance is USD 39,547, and the average total balance (including private loans) may be as high as USD 43,333.

- As of Q4 2025, about 10% of federal student loan dollars were delinquent, meaning payments were past due.

- As of Q3 2025, about 1.62% of private student loans were in default, meaning borrowers failed to repay under the loan terms.

- On average, a student at a public university borrows USD 31,960 to complete a bachelor’s degree.

- Total U.S. student loan debt rose from USD 1,805,464.6 million in 2025 Q1 to USD 1,813,619.89 million in 2025 Q2 and USD 1,832,977.54 million in 2025 Q3, with year-over-year growth of 2.97%, 4.16%, and 3.39%, respectively.

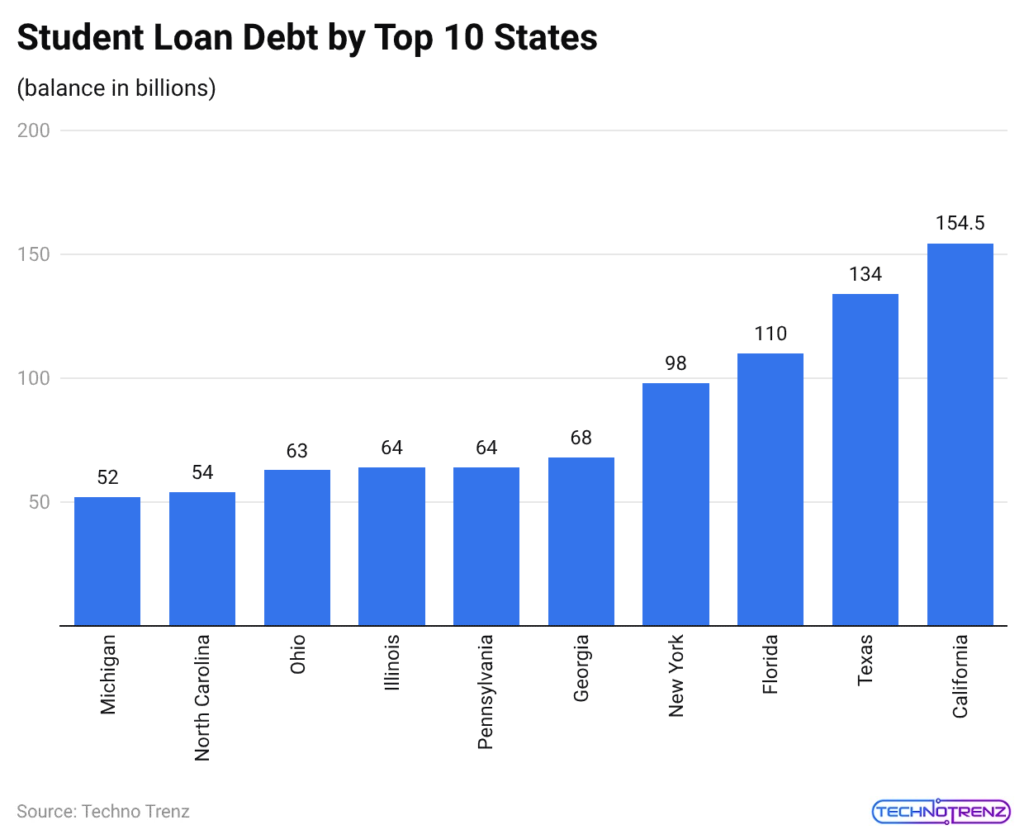

By Top 10 States

(Reference: wooclap.com)

- As of 2025, California has the highest total student debt, at USD 154.50 billion.

- Meanwhile, Michigan has the lowest total among the top 10 states, with 52.00 billion USD in student debt.

- Texas ranks second with USD 134.00 billion, followed by Florida at USD 110.00 billion, New York at USD 98.00 billion, Georgia at USD 68.00 billion, Illinois and Pennsylvania at USD 64.00 billion, Ohio at USD 63.00 billion, and North Carolina at USD 54.00 billion.

Federal Student Loan Debt Analyses, 2025

- A report published by EducationData.org indicates that approximately 53.3% of undergraduate program completers use federal loans at some point during their education.

- Moreover, 54.7% of total federal student loan debt is from Stafford Loans (18% subsidized and 36.7% unsubsidized), while 31.6% is held in Direct Consolidation Loans.

- The federal government disburses approximately USD 87.2 billion annually to all postsecondary students, including graduate and professional students.

- Additionally, Parent PLUS loans account for 6.7% of debt, and Grad PLUS loans for 6.8%, while 28% of undergraduates and 61% of graduates borrow.

| Quarter | Total Federal Student Loan Debt (USD, billions) | YoY Change |

| Q1 | 1,639.60 | 2.58% |

| Q2 | 1,660.70 | 2.51% |

| Q3 | 1,665.60 | 3.39% |

| Q4 | 1,692.60 | 3.30% |

Federal Student Loan Interest Rates

- A report published by Wooclap stated that the annual federal student loan interest rate for Direct Subsidised Loans and Direct Unsubsidized Loans for undergraduate students is 6.39%.

- Direct Unsubsidized Loans for graduate or professional students is 7.94%.

- The interest rate for Direct PLUS Loans (for parents and graduate/professional students) is 8.94%.

Private Student Loan Debt

- Private student loans typically account for less than 10% of total student loan debt.

- The national private student loan balance was USD 133.4 billion.

- Of this private loan balance, 90.70% was for undergraduate borrowing and 9.3% was for graduate student borrowing.

- Regarding repayment status, 19.33% of private student debt was in deferment, 1.86% was in forbearance, and 2.91% was in a grace period.

- Co-signers are widely used: co-signed loans make up 92.45% of private undergraduate student debt, and graduate students use co-signers for 68.46% of their private loan dollars.

Student Loan Repayment Timelines In 2026

- According to a Research.com survey of 61,000 respondents, borrowers take an average of more than 20 years to repay their student loans fully.

- Borrowers who leave college without earning a degree typically take approximately 17 years to repay their student loans.

- Borrowers with graduate degrees (e.g., master’s or PhD) typically take longer to repay, with repayment lasting approximately 23 years on average.

- These repayment timeframes generally align with federal repayment plan terms, which range from 10 to 30 years.

- Under Standard and Graduated repayment options, repayment terms can run from 10 to 30 years.

- Under the Extended Repayment Plan, repayment is typically set at 25 years.

- Under the Income-Sensitive Repayment Plan, repayment is typically set at 15 years.

- Under Income-Driven Repayment options, repayment typically lasts 20 to 25 years, including REPAYE (20 years for undergraduate debt or 25 years for graduate debt), PAYE (20 years), IBR (20 years for certain newer borrowers and 25 years for others), and ICR (25 years).

- NCES data indicate that non-completers are more likely to default (stop paying for 270 days), and only 18.7% of non-completers repaid without default within 12 years, compared with 50% of completers over the same period.

Student Loan Borrower Statistics

- Approximately 20% of U.S. adults with an undergraduate degree currently have outstanding student loan debt.

- 24% of U.S. postgraduates still have student loan debt, while approximately 20% of adults have repaid their loans.

- Over the past 5 years, student loan debt has grown at an average annual rate of 1.66%, while the average tuition and fees have declined by 0.72%.

- In a single year, 28.6% of undergraduate students took out federal student loans.

- Among borrowers with student loan debt, 40% owe money for their own education, while 5% owe money for a child’s or grandchild’s education.

- Additionally, around 28% have a remaining student loan balance of less than USD 10,000.

Student Loan Repayment Statistics

- According to newyorkfed.org, in 2025 Q4, the total outstanding student loan debt (based on credit-bureau data) was USD 1.66 trillion.

- During the same period, the student loan delinquency rate for balances 90+ days past due was 9.6%.

- About 1,000,000 borrowers who were 120+ days past due were transferred due to severe past-due repayment status.

- In June 2025, the federal student loan portfolio covered 42.3 million recipients with a total balance of USD 1.67 trillion.

- Around 5.3 million borrowers were in default, representing around USD 117 billion, which is roughly 7% of the USD 1.58 trillion federally managed loan balance.

- Among borrowers in active repayment, more than 65% were current, while 34.4% were 30+ days delinquent.

- The delinquency rate by dollar balance for loans in active repayment that were 31+ days delinquent was 29.5%.

- In August 2025, 21% of borrowers had a recently reported student-loan delinquency of 60+ days past due within the prior 24 months.

- In 2025, the median required monthly payment for borrowers in repayment (based on credit-bureau data) was USD 182, compared with USD 173 in 2024.

- In August 2025, prime-credit borrowers had a median balance that was 86% of their August 2023 balance, which implies a median paydown of about 14% since repayment restarted.

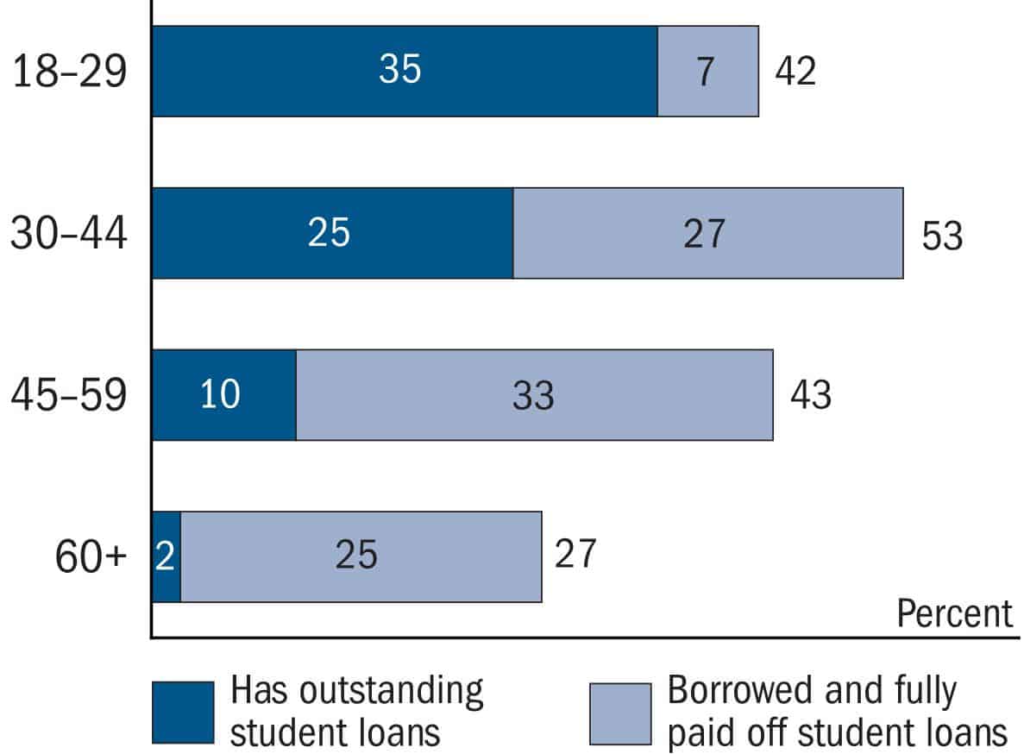

Student Loan Borrowing And Repayment Statistics By Age

(Source: federalreserve.gov)

- The share of adults who ever borrowed student loans for their own education is 42% for ages 18-29 (35% still owe and 7% have fully paid), 53% for ages 30-44 (25% still owe and 27% have fully paid), 43% for ages 45-59 (10% still owe and 33% have fully paid), and 27% for ages 60+ (2% still owe and 25% have fully paid).

- Overall, outstanding debt declines with age, from 35% (ages 18-29) to 2% (ages 60+), while the fully paid share is higher in older groups (from 7% in ages 18-29 to 33% in ages 45-59).

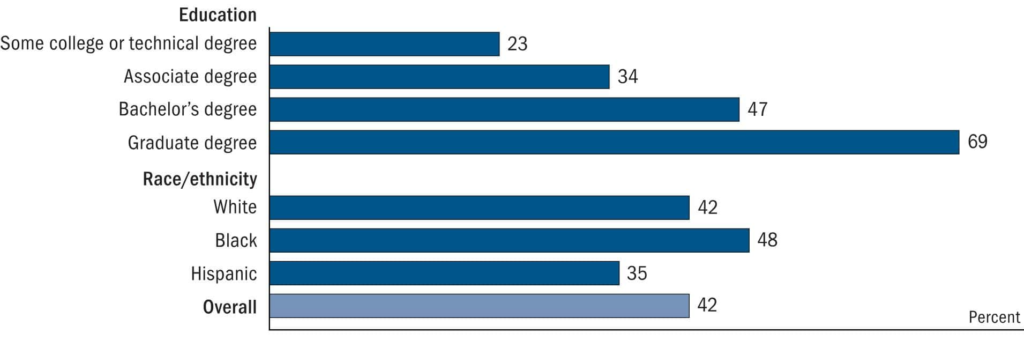

By Education and Race/Ethnicity

(Source: federalreserve.gov)

- The share of borrowers with at least USD 25,000 in student loan debt increases with education level: 23% for some college or a technical degree, 34% for an associate degree, 47% for a bachelor’s degree, and 69% for a graduate degree.

- By race/ethnicity, the share of borrowers with at least USD 25,000 is 42% for White borrowers, 48% for Black borrowers, and 35% for Hispanic borrowers, and the overall share is 42%.

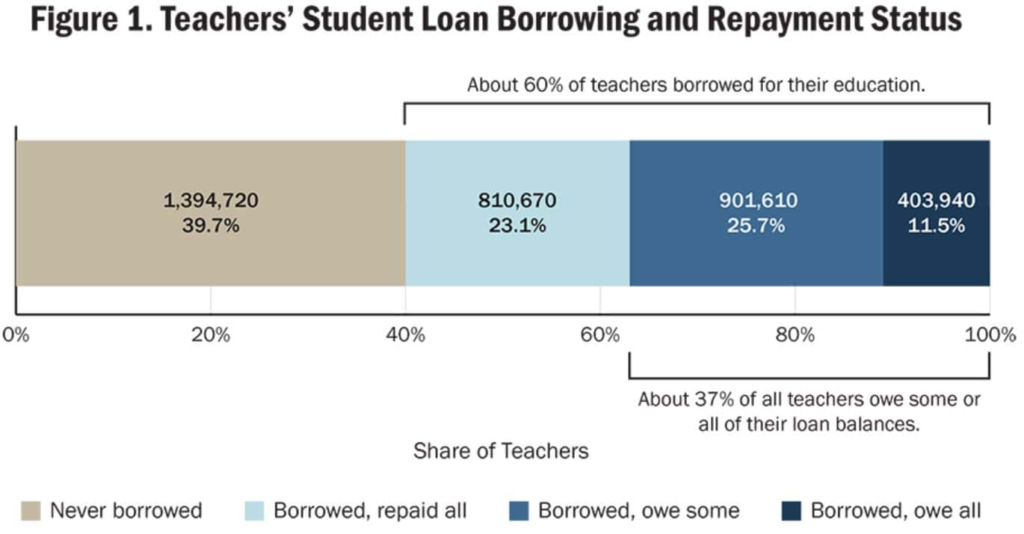

Teachers’ Student Loan Borrowing And Repayment Status

(Source: learningpolicyinstitute.org)

| Status category | Number of teachers | Share of teachers |

| Never borrowed student loans | 1,394,720 | 39.7% |

| Borrowed student loans and repaid 100% | 810,670 | 23.1% |

| Borrowed student loans and still owe some balance | 901,610 | 25.7% |

| Borrowed student loans and still owe all balance | 403,940.00 | 11.5% |

| Total | 3,510,940 | 100% |

States With The Highest And Lowest Average Student Debt

- According to Forbes, the difference between the highest state (New Hampshire, USD 39,928) and the lowest state (Utah, USD 18,344) is USD 21,584, corresponding to about 118% of the difference between the highest and lowest.

| Category | State | Average student debt (USD) |

| Highest debt | New Hampshire | 39,928 |

| Delaware | 39,705 | |

| Pennsylvania | 39,375 | |

| Rhode Island | 36,791 | |

| Connecticut | 35,853 | |

| Lowest debt | Utah | 18,344 |

| New Mexico | 20,868 | |

| California | 21,125 | |

| Nevada | 21,357 | |

| Wyoming | 23,510 |

Student Loan Forgiveness Statistics

- In 2025, although major income-driven repayment forgiveness programs were paused due to legal challenges, approximately 121,000 borrowers still received federal student loan forgiveness, according to Investopedia.

- The collegeaidservices.net report further stated that approximately 117,280 borrowers received relief through the Public Service Loan Forgiveness program, while 3,570 borrowers received forgiveness through income-driven repayment (IDR) plans.

- By early 2025, in the U.S., the Department of Education approved more than USD 600 million in student loan forgiveness through its final IBR and borrower defense actions for that year.

- In January 2025 alone, an additional USD 3.82 billion was approved for 146,000 borrowers, bringing total approved relief since 2021 to more than USD 183.6 billion.

Strategies To Pay Off Student Loans Faster

- Pay a small additional amount each month to reduce the loan balance faster.

- Add USD 50 or USD 100 as soon as possible.

- Try biweekly payments to make 1 extra payment each year.

- Refinance only if your interest rate drops by 1%-2% or more.

- Don’t refinance federal loans if you need forgiveness or flexible repayment options.

- Pick a shorter repayment plan if you can afford the higher monthly payment.

- Round up your payment (for example, to the nearest USD 50 or USD 100).

- Use bonuses, gifts, or tax refunds to make a big one-time payment.

- Keep your spending steady after a raise and put the extra money toward your loan.

- Seek help, such as forgiveness programs, employer support, or a side income.

Conclusion

Student loans can weaken graduates’ financial health by lowering credit scores, slowing savings, and delaying major life goals such as buying a home or starting a family. Repayment is not equally hard for everyone; income, course choice, finishing college, and racial and wealth gaps all shape who struggles most. Real progress needs more than better budgeting.

We need repayment plans that match people’s incomes, limit runaway interest, and make help easy to find. Cutting loan stress isn’t just relief for borrowers, it strengthens opportunity and boosts the economy.

FAQ

Use a loan calculator with principal, interest rate, and term; check your lender statement.

High interest rates, low income/unemployment, short repayment terms, multiple loans, capitalized interest, and high living costs.

Fixed standard, graduated, extended, income-driven, refinancing, consolidation, and temporary relief like deferment/forbearance.

Build an emergency fund first; then pay extra on high-interest loans, especially credit cards and private loans.

You may become delinquent, then default, which can trigger fees, credit damage, collections, and possible wage garnishment.