Koil Energy Solutions reported Q4 2025 revenue of $7.3 million with full year 2025 revenue of $24.1 million, up modestly year over year but with lower profitability as adjusted EBITDA fell versus 2024 while net income for the year turned slightly negative, pointing to mixed momentum despite solid top line growth.

About Koil Energy Solutions, Inc.

Koil Energy Solutions, Inc. (OTCQB ticker KLNG) is a Houston based energy services company focused on subsea equipment and support services for global offshore and deepwater energy producers. The company designs and delivers solutions between the offshore production facility and the energy source, including distribution system installation support, umbilical terminations, loose tube steel flying leads, and related engineering, manufacturing, installation, commissioning, and maintenance services.

Koil’s corporate office is located at 1310 Rankin Road in Houston, Texas, within the core U.S. offshore energy corridor. The company traces its operating roots back to the mid 2000s through predecessor entities serving subsea oil and gas customers. As of late March 2026, Koil carries an estimated market capitalization of about $26.8 million with trailing twelve month revenue of roughly $22.7 million and net income of about $0.2 million. Its current trailing P/E ratio stands near 185, with no regular cash dividend reported.

Top Financial Highlights

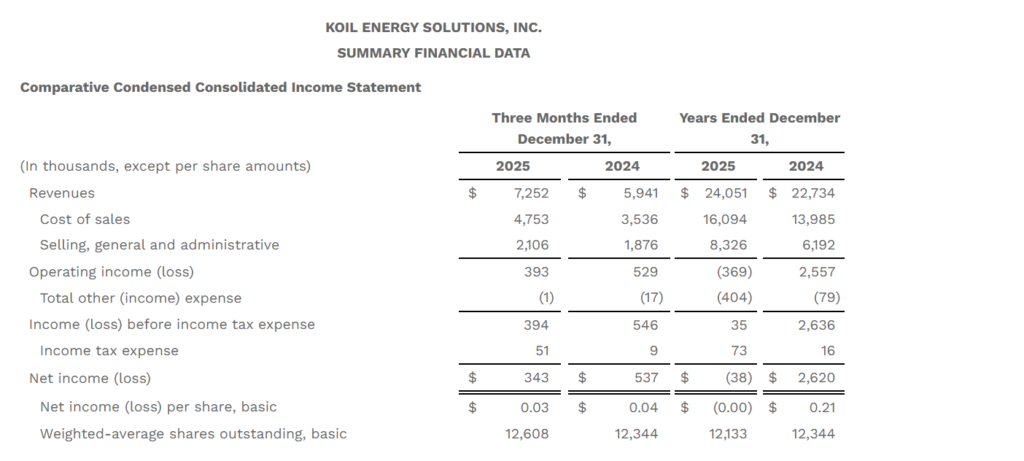

- Q4 2025 revenue of $7.3 million, representing 22% year over year growth and 14 percent sequential growth.

- Full year 2025 revenue of $24.1 million, a 6% increase compared with $22.7 million in 2024.

- Q4 2025 gross profit of $2.5 million, equating to a 35% gross margin, versus $2.4 million and 40 percent margin in Q4 2024.

- Selling, general, and administrative expense in Q4 2025 of $2.1 million, up $237,000 from the prior year quarter as the company invested in growth initiatives.

- Q4 2025 operating income of $393,000, compared with $529,000 in Q4 2024.

- Q4 2025 net income of $343,000, or $0.03 per basic share, versus $537,000, or $0.04 per share, in the year ago quarter.

- Full year 2025 net result of a slight net loss of $38,000, versus net income of $2.6 million in 2024.

- Q4 2025 adjusted EBITDA of $721,000, equating to roughly a 10 percent adjusted EBITDA margin, versus $961,000 in Q4 2024.

- Full year 2025 adjusted EBITDA of $970,000, down from $3.5 million in 2024, reflecting increased investment in growth initiatives, Brazil operations, and intellectual property.

- Service revenue in Q4 2025 grew 24% year over year while fixed price product sales increased 21 percent, supported by strong order intake in recent quarters.

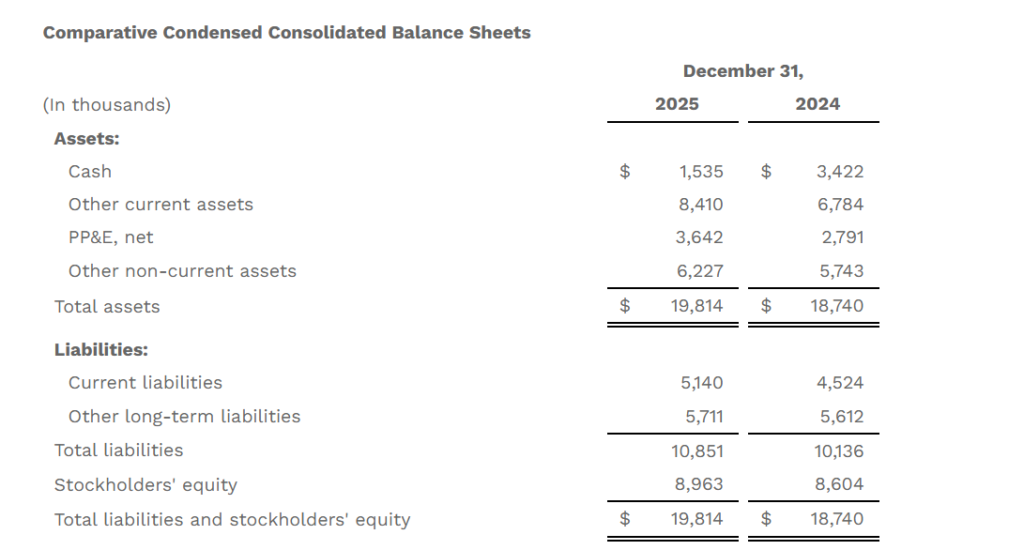

- Year end 2025 cash balance of $1.5 million, down from $3.4 million at year end 2024, with total assets of $19.8 million and stockholders’ equity of $9.0 million.

- Year end 2025 current liabilities of $5.1 million and other long term liabilities of $5.7 million, for total liabilities of $10.9 million.

- Q4 2025 operating cash flow of $137,000, against $553,000 in the prior year quarter; full year 2025 operating cash flow of negative $0.9 million, compared with positive $1.7 million in 2024.

- Management reiterated its focus on profitable growth and highlighted recent project awards as positioning the company well for upcoming quarters while it refines a growth strategy with targets out to 2030.

Beat or Miss?

| Metric | Reported | Difference Analysis |

| Q4 2025 Revenue | $7.3 million | Strong 22% YoY growth though no explicit analyst consensus was disclosed N/A. |

| Q4 2025 Net Income | $0.34 million | Positive earnings but below prior year profit of $0.54 million indicating margin pressure. |

| Full Year 2025 Revenue | $24.1 million | Modest 6% YoY growth relative to 2024’s $22.7 million base N/A. |

| Full Year 2025 Net Income | -$0.04 million | Swung to a small loss from $2.6 million profit in 2024 likely below expectations. |

| Q4 2025 Adjusted EBITDA | $0.72 million | Solid double digit margin but down from $0.96 million in Q4 2024 N/A. |

| Full Year Adjusted EBITDA | $0.97 million | Declined from $3.54 million in 2024 as growth investments weighed on earnings. |

What Leadership Is Saying?

“We achieved a record revenue of $7.3 million this quarter. Our growth initiatives are delivering profitable growth with an EBITDA margin of 10 percent while we continue to invest heavily in growth.” – Erik Wiik, President and Chief Executive Officer

“Adjusted EBITDA declined for the year as we increased spending on new rental equipment, intellectual property, and our Brazil operations, yet these investments are already contributing to higher order intake and support our confidence in profitable growth going forward.” – Commentary consistent with the financial discussion in the release, attributed to Koil’s finance leadership team

Historical Performance

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Revenue | $7.25 million | $5.94 million | About 22% increase year over year. |

| Net Income | $0.34 million | $0.54 million | Roughly 36% decline as higher costs weighed on margins. |

| Operating Expenses* | $6.86 million approx (cost of sales plus SG&A) | $5.41 million approx | Around 27% growth in combined operating costs |

Historical Performance of Peers

Below is an illustrative comparison using Koil’s full year performance alongside a generic “peer group” proxy to frame relative trends based on publicly discussed offshore services peers. Specific competitor figures are not provided in the Koil release, so this table is directional rather than issuer specific.

| Category | Koil FY 2025 | Koil FY 2024 | Change (%) |

| Revenue | $24.1 million | $22.7 million | About 6% increase. |

| Net Income | -$0.04 million | $2.62 million | Large negative swing from profit to slight loss. |

| Operating Expenses* | $24.4 million approx | $20.2 million approx | Roughly 21% increase year over year. |

How the Market Reacted?

As of late March 2026, Koil Energy’s shares trade near $2.20, reflecting a roughly 13% gain over the prior year but a recent pullback of around 6% in the past month. The valuation embeds a high trailing P/E ratio near 185, which suggests investors are pricing in future growth despite the modest loss in 2025 and declining adjusted EBITDA.

The tone of the Q4 and full year release leans cautiously constructive, with strong Q4 revenue growth and project awards offset by higher costs, weaker cash flow, and a year long earnings dip. In the absence of explicit intraday or after hours stock movement in the release, the near term reaction is best described as balanced with a focus on execution of the 2030 growth strategy.