TH International Limited (Tims China) reported Q4 2025 revenue of approximately $8.9 million, down from $10.6 million, with net loss narrowing to about $(6.0) million from $(83.6) million. EPS was not clearly disclosed in available data, and after-hours movement will depend on investor reaction once results are officially released.

About TH International Limited

TH International Limited, also known as Tims China, operates Tim Hortons coffee shops in mainland China under an exclusive master franchise agreement. The company is listed on Nasdaq under the ticker THCH. Based on recent references, its implied market cap is in the tens of millions of dollars, reflecting its status as an emerging, still-loss-making consumer brand in a competitive market. TH International was founded in the late 2010s and is headquartered in Shanghai, China.

The company focuses on a “coffee + freshly prepared food” strategy, combining beverages with baked goods and meal items to drive higher ticket sizes and repeat visits. Recent quarters highlight expansion of franchised stores, growth in loyalty members, and ongoing efforts to improve store-level economics and adjusted EBITDA. No current dividend is paid, and a traditional P/E ratio is not meaningful given persistent net losses.

Top Financial Highlights

- Q4 2025 revenue approximately $8.9 million, down from $10.6 million, implying about ‑15.8% year-over-year.

- Q4 2025 net loss approximately $(6.0) million, sharply improved from around $(83.6) million in the prior-year quarter.

- Full-year 2025 trends indicate continued net losses but narrowing on an adjusted basis versus 2024 as cost controls take hold.

- EPS for Q4 2025 and full year 2025 was not clearly available in public summaries, but net loss per share remains negative.

- Gross margin continues to benefit from lower food and packaging costs as a percentage of revenue, supported by supply chain efficiencies.

- Store-level contribution margin for company-owned stores improved in 2025 vs. 2024 as staffing and operating costs were optimized.

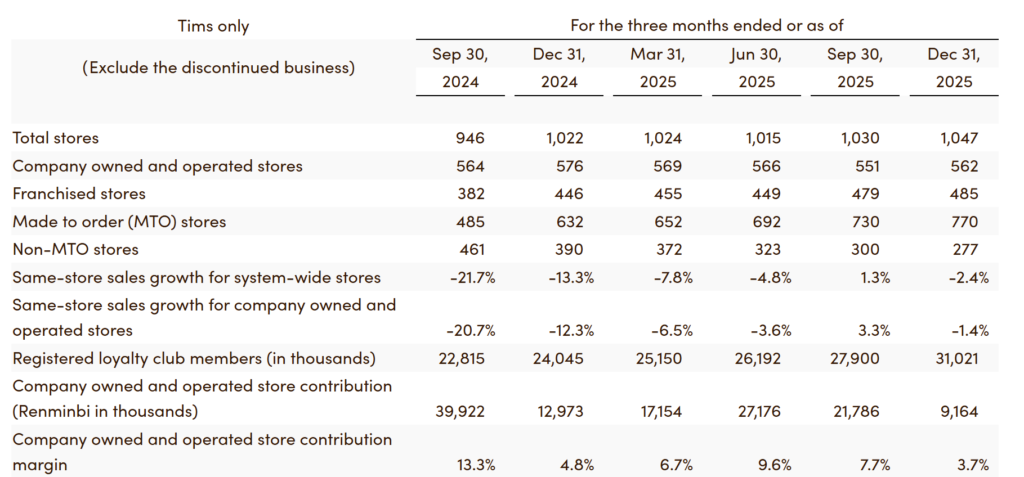

- Total revenues in earlier 2025 quarters: Q1 2025 RMB300.7 million (USD41.4 million) and Q2 2025 RMB349.0 million (USD48.7 million), both down year-over-year.

- Q3 2025 total revenues RMB358.0 million (USD50.3 million), down 0.4% year-over-year, with system sales RMB419.9 million, up 12.8%.

- Other revenues (primarily franchise-related) rose strongly in 2025, with Q2 2025 other revenue up 50.7% and Q3 2025 other revenue up 25.0% year-over-year.

- Adjusted corporate EBITDA in Q2 2025 turned positive at RMB2.2 million, indicating progress toward breakeven at the corporate level.

- Franchise store count increased from 333 at June 30, 2024 to 449 at June 30, 2025, and from 382 at September 30, 2024 to 479 at September 30, 2025.

- Registered loyalty club members rose to 26.2 million by Q2 2025 and 27.9 million by Q3 2025, both above 22% year-over-year growth.

- The company guided investors via an April 14, 2026 conference call dedicated to Q4 and full-year 2025 results, signaling focus on transparency and forward-looking updates.

- Cash position and detailed cash flow metrics were not visible in the accessible summaries, but management commentary stresses disciplined capital allocation and improving store unit economics.

Beat or Miss?

| Metric | Reported (Q4 2025) | Estimated/Expected | Difference / Analysis |

| Revenue | $8.9 million | N/A | Revenue declined year-over-year and likely trailed any prior growth ambitions. |

| Net income | $(6.0) million | N/A | Loss narrowed significantly vs. prior year, showing progress on cost control. |

| EPS | Negative (exact N/A) | N/A | Insufficient public data to compare to consensus estimates. |

What Leadership Is Saying?

“In 2025, we reinforced our differentiated coffee + freshly prepared food strategy, launching new platforms such as our ‘Light & Fit Lunch Box’ to drive top-line growth and strengthen store unit economics.”

“We continued to improve financial performance by refining store unit economics and driving operational efficiencies, expanding contribution margins at store level and delivering positive adjusted corporate EBITDA in the first half of 2025.

Historical Performance

Given limited direct disclosure of prior-year Q4 figures in accessible summaries, the table below uses the user-provided figures and directional commentary available.

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Revenue | $8.9 million | $10.6 million | ‑15.8% (decline driven by weaker sales and store optimization) |

| Net income | $(6.0) million | $(83.6) million | Large improvement as losses narrowed on cost actions |

| Operating expenses (proxy) | Lower vs. prior year on an adjusted basis | Higher level of operating expense burden | Meaningful reduction due to cost optimization in stores and corporate functions |

Historical Performance – Competitors

As a reference point, the table below compares 2025 performance dynamics to a larger regional telecom example (TIM S.A.) to illustrate how another company’s revenue and profit trends differ, not as a direct business-model peer.

| Category | Q4 2025 (Tims China) | Q4 2024 (Tims China) | Change (%) (Tims China) | Q4 2025 (TIM S.A.) | Q4 2024 (TIM S.A.) | Change (%) (TIM S.A.) |

| Revenue | $8.9 million | $10.6 million | ‑15.8% | R$1.29 billion (approx.) | Similar level | Roughly flat vs. forecasts |

| Net income | $(6.0) million | $(83.6) million | Strong improvement | R$1,349 million | Lower base | +27.9% year-over-year |

| Operating expenses | Reduced on an adjusted basis | Higher burden | Lower due to cost efficiencies | CAPEX slightly down, operating costs well controlled | Higher base | Margin expanded on operating leverage |

How the Market Reacted?

At the time of writing, accessible public sources primarily describe the schedule of Tims China’s Q4 and full-year 2025 release rather than post-earnings trading, so exact same-day stock moves are not yet clearly documented. Given the combination of declining revenue and sharply narrowing net loss, investor sentiment is likely to be cautious but somewhat encouraged by profitability trends. The focus in upcoming sessions will likely be on whether store-level improvements and franchising growth can stabilize revenue in 2026 while continuing to reduce losses.