Array Digital Infrastructure (NYSE: AD) posted Q1 2026 diluted EPS of $2.08 from continuing operations, crushing the FactSet consensus of $0.91, while total operating revenue of $52.0 million came in below the analyst estimate of $54.3 million. Shares surged roughly 13.7% to $56.06 on earnings day, reflecting strong investor enthusiasm over the spectrum monetization windfall and reaffirmed full-year guidance.

About Array Digital Infrastructure

Array Digital Infrastructure, Inc. (NYSE: AD) is a Chicago-based owner and operator of shared wireless communications infrastructure in the United States. Formerly United States Cellular Corporation (USCC), the company was renamed Array following the close of a landmark deal in which T-Mobile acquired USCC’s wireless operations for approximately $4.4 billion on August 1, 2025.

Today, Array owns 4,452 cell towers across 19 states and enables deployment of 5G and other wireless technologies nationwide. The company trades on the NYSE under the ticker AD, carries a market capitalization of approximately $4.82 billion, and is approximately 81.9% owned by Telephone and Data Systems, Inc. (TDS). As a standalone tower company with a portfolio of monetizable spectrum assets, Array also holds equity interests in unconsolidated wireless entities worth $435 million on its balance sheet as of Q1 2026.

Top Financial Highlights

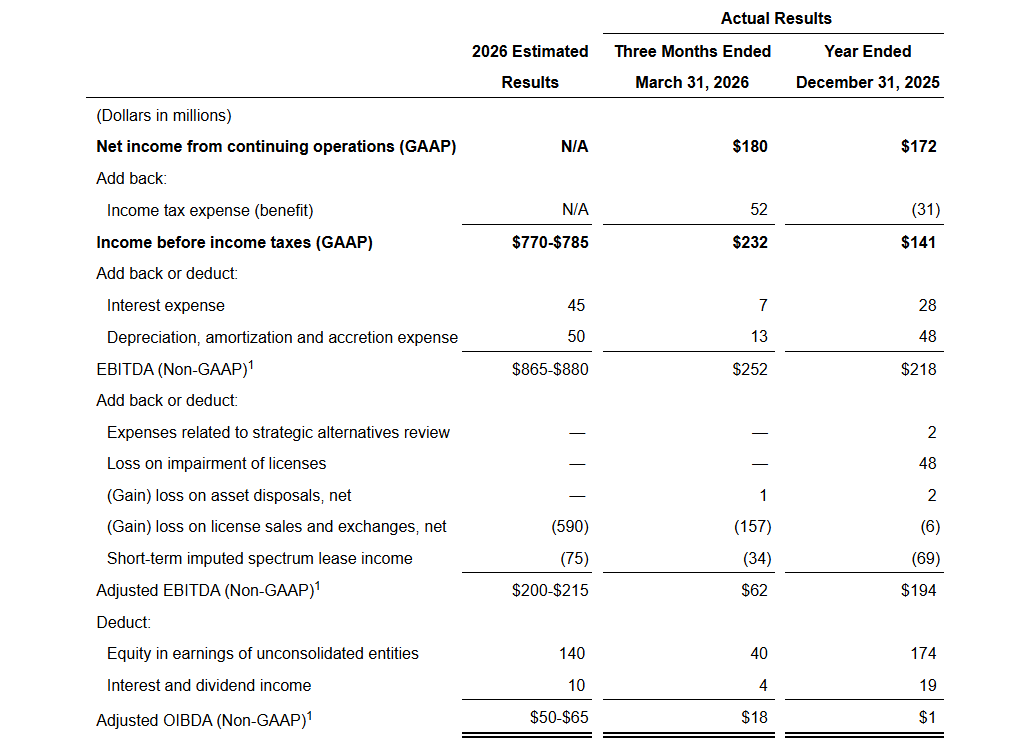

- Total operating revenue from continuing operations reached $52.0 million, increasing 93% year over year from $27.0 million in Q1 2025.

- Site rental revenue totaled $51.0 million, rising 92% year over year and continuing to represent the company’s primary business segment.

- Services revenue was $988 thousand, compared to $389 thousand in Q1 2025.

- Net income from continuing operations attributable to shareholders reached $179.8 million, significantly higher than $4.7 million in the prior-year quarter.

- Diluted EPS from continuing operations stood at $2.08, compared to $0.05 in Q1 2025.

- Total diluted EPS was $2.06, including a minor loss from discontinued operations.

- Adjusted EBITDA increased to $62.5 million, compared to $21.2 million in Q1 2025.

- Adjusted OIBDA reached $17.8 million, improving from a loss of $17.4 million in the prior-year period.

- Operating cash flow from continuing operations was $24.5 million, compared to a cash use of $71.2 million in Q1 2025.

- Adjusted free cash flow from continuing operations totaled $30.7 million during the quarter.

- Cash and cash equivalents stood at $253.6 million as of March 31, 2026, increasing from $113.4 million at the end of 2025.

- The company recorded a spectrum-related book gain of $156.6 million, or $117.5 million net of tax, following completion of spectrum license sales valued at $1.018 billion.

- Capital expenditures were $8.6 million in Q1 2026, with full-year guidance maintained between $25 million and $35 million.

- Full-year 2026 guidance remains unchanged, with expected total operating revenue of $200 million to $215 million, adjusted EBITDA of $200 million to $215 million, and adjusted OIBDA between $50 million and $65 million.

Beat or Miss?

| Metric | Reported | Estimate | Difference/Analysis |

| Diluted EPS (Continuing Ops) | $2.08 | $0.91 (FactSet) | Beat by $1.17; driven by $156.6M spectrum license gain |

| Total Operating Revenue | $52.0M | $54.3M (FactSet) | Missed by ~$2.3M; tower business growing but DISH headwind persists |

| Site Rental Revenue | $51.0M | N/A | Up 92% YoY; core driver of business |

| Full-Year 2026 Revenue Guidance | $200M to $215M | $209M (FactSet) | In line with consensus midpoint |

| Adjusted EBITDA (Q1) | $62.5M | N/A | More than doubled from $21.2M in Q1 2025 |

What Leadership Is Saying?

CEO Anthony Carlson on strategy and execution:

“Array is executing on its 2026 priorities. Since standing-up Array just eight months ago, we remain laser-focused on optimizing our tower operations, including securing new colocation applications and delivering steady tower tenancy growth. And we are continuing to close our pending spectrum transactions and support T-Mobile’s integration.”

CFO Vicki L. Villacrez on financial performance (from earnings call participation):

Array’s Q1 results reflected meaningful progress in transitioning to a standalone tower company, with Adjusted EBITDA tripling year over year to $62.5 million, operating cash flow turning positive at $24.5 million, and the balance sheet strengthened by over $1 billion in spectrum proceeds, positioning the company to deliver on its full-year 2026 targets.

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Total Operating Revenue | $52.0M | $27.0M | 93% |

| Site Rental Revenue | $51.0M | $26.6M | 92% |

| Net Income (Continuing Ops, to Shareholders) | $179.8M | $4.7M | 3,733% |

| Total Operating Expenses | $(108.8M) | $56.6M | N/M (gain on spectrum sale reversed expenses) |

| SG&A Expenses | $12.7M | $29.2M | -56% |

| Cost of Operations | $21.6M | $16.3M | 33% |

| Adjusted EBITDA | $62.5M | $21.2M | 195% |

| Diluted EPS (Continuing Ops) | $2.08 | $0.05 | 4,060% |

| Cash and Cash Equivalents | $253.6M | $200.5M (end of Q1 2025) | 27% |

Competitor YoY Comparison

Q1 2026 vs Q1 2025

The following table benchmarks Array Digital Infrastructure against key U.S. tower and wireless infrastructure peers:

| Company (Ticker) | Q1 2026 Revenue | Q1 2025 Revenue | Change (%) | Q1 2026 Net Income | Q1 2025 Net Income | Net Income Change (%) |

| Array Digital Infrastructure (AD) | $52.0M | $27.0M | 93% | $179.8M | $4.7M | 3733% |

| American Tower (AMT) | $2,738M | $2,563M (est.) | 6.80% | $879M | $499M (est.) | 76.20% |

| Crown Castle (CCI) | $961M | $1,011M | -5% | $151M | $(464M) | N/M (loss to income) |

| SBA Communications (SBAC) | $703.4M | ~$680M (est.) | ~+3% | $184.8M | N/A | N/A |

How the Market Reacted?

Array Digital Infrastructure shares surged +13.72% to close at $56.06 on May 8, 2026, the day Q1 2026 results were reported, with after-hours trading adding another +1.11% to approximately $56.69. The reaction reflected bullish sentiment on the massive EPS beat ($2.08 vs. $0.91 estimated) and the confirmation of a non-binding acquisition proposal from majority owner TDS to buy out all remaining public shareholders at $10.40 per share in net proceeds. Analyst consensus rated the stock Strong Buy with a 12-month price target of $55.00, and the stock’s 52-week range spans from $44.03 to $79.17, underscoring ongoing investor confidence in Array’s tower-focused transition strategy.