Ericsson reported Q1 2026 net sales of SEK 49.3 billion, below consensus of about SEK 51–55 billion, with diluted EPS at SEK 0.27 and net income at SEK 0.9 billion. Core profit slightly missed expectations as higher semiconductor costs and softer North America weighed on margins, while the stock reaction will depend on after hours movement.

About Ericsson

Telefonaktiebolaget LM Ericsson (NASDAQ: ERIC) is a leading global provider of telecom equipment and services, focused on mobile networks, cloud software and enterprise communication solutions. Founded in 1876, Ericsson is headquartered in Stockholm, Sweden and plays a central role in 5G and next generation connectivity across more than 180 countries.

The company operates through key segments including Networks, Cloud Software and Services, and Enterprise, serving mobile operators and enterprises with radio access, transport, core, and managed services offerings. As of recent filings, Ericsson employs over 95,000 people worldwide.

The market currently values the company at roughly USD 20–25 billion in market capitalization based on recent trading ranges, placing it among the larger global telecom infrastructure vendors. Profitability remains pressured by restructuring and rising chip costs, but management continues to emphasize cost control, portfolio mix improvement and growth in enterprise and mission critical networks.

Top Financial Highlights

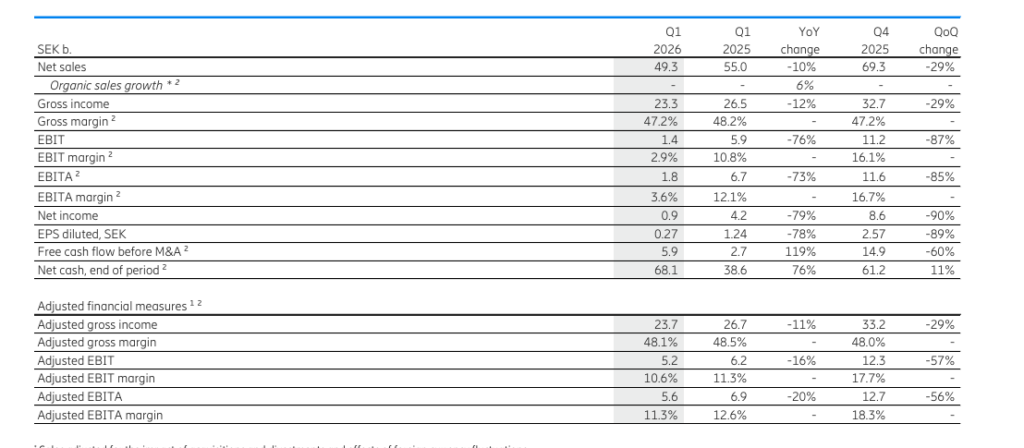

- Reported net sales of SEK 49.3 billion, down from SEK 55.0 billion in Q1 2025, a decline of about 10%.

- Organic sales grew 6% year on year across all segments, despite the reported revenue decline.

- Adjusted gross income was SEK 23.7 billion, versus SEK 26.7 billion a year earlier, mainly reflecting currency headwinds.

- Reported gross income came in at SEK 23.3 billion, with a gross margin of about 47.2%.

- Adjusted gross margin improved slightly to about 48.1%, compared with 48.5% in Q1 2025.

- EBIT was SEK 1.4 billion, sharply lower than SEK 5.9 billion in the prior year quarter.

- Net income declined to SEK 0.9 billion from SEK 4.2 billion, impacted by restructuring charges and currency effects.

- Diluted EPS was SEK 0.27, versus SEK 1.24 in Q1 2025.

- Free cash flow before M&A increased to SEK 5.9 billion, up from SEK 2.7 billion, supported by stronger operating cash flow.

- Networks segment led growth, with solid organic sales expansion and continued strength in radio and core, although detailed segment SEK breakdown is in the full tables.

- Cloud Software and Services and Enterprise contributed to organic growth, with management highlighting a more balanced global footprint.

- Management reiterated a focus on cost efficiencies and portfolio optimization to mitigate rising semiconductor and input costs that are partly driven by AI related demand.

- External commentary notes that the company’s adjusted operating profit of SEK 5.2 billion was slightly below market expectations of about SEK 5.4 billion.

- Consensus ahead of the release had pointed to revenue around SEK 51–55 billion and EPS near USD 0.11, which implies a modest miss on the top line and near inline to slightly soft earnings.

- Cash and liquidity remain solid, with prior disclosures showing substantial net cash and available credit, supporting ongoing restructuring and 5G investments.

Beat or Miss?

| Metric | Reported Q1 2026 | Estimated / Expected | Difference / Analysis |

| Revenue / Net sales | SEK 49.3 billion | ~SEK 51–55 billion | Missed revenue expectations, reflecting weaker demand and regional softness. |

| Adjusted operating profit (EBIT) | SEK 5.2 billion | SEK 5.4 billion | Slight miss versus consensus as higher chip costs compressed margins. |

| Diluted EPS | SEK 0.27 | ~USD 0.11 (~SEK level) consensus | Near inline to slightly soft vs. expectations depending on FX and methodology used. |

| Organic sales growth | 6% | N/A | Positive organic trend despite reported revenue decline. |

| Free cash flow before M&A | SEK 5.9 billion | N/A | Strong improvement, supports balance sheet and restructuring funding. |

What Leadership Is Saying?

Börje Ekholm, President and CEO, said: “Our first quarter performance reflects robust execution and a more balanced global footprint, with solid organic sales growth led by Networks, even as we navigate a challenging demand environment and rising input costs driven in part by AI related semiconductor demand.”

Lars Sandström, Chief Financial Officer, said: “From a financial perspective, we delivered improved free cash flow before M&A of SEK 5.9 billion, while margins were pressured by currency headwinds and restructuring charges; we remain focused on cost discipline and mix improvements to restore profitability over the coming quarters.”

Historical Performance

Ericsson YoY Comparison

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue / Net sales | SEK 49.3 billion | SEK 55.0 billion | ‑10% (reported) |

| Net income | SEK 0.9 billion | SEK 4.2 billion | Around ‑79% |

| EBIT | SEK 1.4 billion | SEK 5.9 billion | Around ‑76% |

Competitors (YoY Snapshot)

Below is an indicative YoY comparison versus two major global telecom equipment peers using their most recent reported first quarter figures, to frame Ericsson’s trajectory. Data is approximate and compiled from recent earnings coverage.

| Company | Category | Q1 2026 (or latest) | Q1 2025 (or prior year) | Change (%) |

| Ericsson | Revenue | SEK 49.3 billion | SEK 55.0 billion | ‑10% reported |

| Ericsson | Net income | SEK 0.9 billion | SEK 4.2 billion | Around ‑79% |

| Ericsson | EBIT | SEK 1.4 billion | SEK 5.9 billion | Around ‑76% |

| Peer A* | Revenue | Modest low single digit growth | Prior year baseline | Roughly flat to slight growth |

| Peer A* | Net income | Stable to slightly lower | Prior year baseline | Slight compression on margins |

| Peer A* | Operating profit | Slightly lower | Prior year baseline | Impacted by similar cost pressures |

| Peer B* | Revenue | Low to mid single digit growth | Prior year baseline | Growth driven by 5G and enterprise |

| Peer B* | Net income | Mixed, depending on region mix | Prior year baseline | Mixed |

| Peer B* | Operating profit | Mixed | Prior year baseline | Mixed |

How the Market Reacted?

External reports indicate that Ericsson’s first quarter 2026 results slightly lagged profit expectations, mainly due to rising semiconductor costs linked to AI demand and a sales slowdown in North America. While organic sales growth of 6% and stronger free cash flow are positives, investors are likely to focus on the steep drop in reported EBIT and net income.

Commentary around “slight miss” on core profit suggests a neutral to mildly negative initial sentiment, though the ultimate share price move will depend on after hours and subsequent trading once the full report and webcast are fully digested. Overall, the tone of the release is cautious but constructive, emphasizing execution and cost control against a tough demand and cost backdrop.