Palantir smashed Wall Street expectations in Q4 2025, posting adjusted EPS of $0.25 (vs. $0.23 estimated) and revenue of $1.41 billion (vs. $1.32 billion consensus), marking a 70% year-over-year gain. The company also issued a fiscal 2026 revenue guide of $7.18–$7.20 billion, far above analyst projections of $6.28 billion. Shares surged over 12% in premarket trading following the announcement, reflecting broad investor enthusiasm.

About Palantir Technologies

Palantir Technologies Inc. (NASDAQ: PLTR) was founded in 2003 and is headquartered in Denver, Colorado, with operations now also based in Miami, Florida. The company builds and deploys data analytics and artificial intelligence software platforms for government agencies and commercial enterprises globally, with flagship products including Gotham (government intelligence), Foundry (commercial operations), and its AI Platform (AIP) that has become the primary commercial growth engine.

As of early May 2026, Palantir carries a market capitalization of approximately $342-$345 billion, with shares trading around $144. The stock trades at a forward price-to-earnings (P/E) ratio of roughly 220x, reflecting the premium the market assigns to its AI-driven hypergrowth trajectory. Palantir does not pay a dividend. The company employs thousands across its global operations and has been GAAP profitable for multiple consecutive quarters, a milestone that separates it from many peers in the enterprise AI space.

Top Financial Highlights

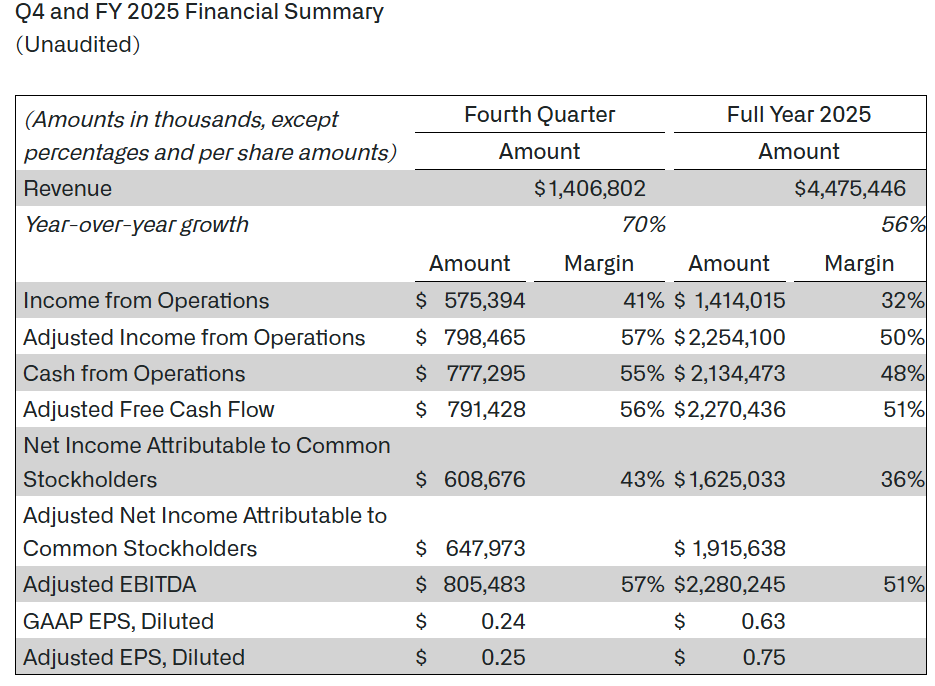

- Total revenue reached $1.41 billion in Q4 2025, up 70% year-over-year – the highest growth rate in Palantir’s history as a public company

- U.S. revenue surged 93% year-over-year (and 22% quarter-over-quarter) to $1.076 billion, now representing 77% of total revenue

- U.S. commercial revenue skyrocketed 137% year-over-year and 28% quarter-over-quarter to $507 million

- U.S. government revenue grew 66% year-over-year and 17% quarter-over-quarter to $570 million

- GAAP EPS (diluted) came in at $0.24; adjusted EPS (diluted) reached $0.25, beating the $0.23 consensus by 8.7%

- GAAP net income was $609 million, representing a 43% net margin

- GAAP income from operations hit $575 million at a 41% operating margin

- Adjusted income from operations was $798 million at a 57% adjusted operating margin, beating estimates by 13.9%

- Cash from operations totaled $777 million with a 55% margin; adjusted free cash flow reached $791 million at a 56% margin

- Record total contract value (TCV) of $4.262 billion, up 138% year-over-year, including a record $1.344 billion in U.S. commercial TCV

- U.S. commercial remaining deal value (RDV) stood at $4.38 billion, up 145% year-over-year

- Customer count grew 34% year-over-year, with 180 deals of at least $1 million, 84 of at least $5 million, and 61 of at least $10 million

- Cash, cash equivalents, and short-term U.S. Treasury securities of $7.2 billion on hand

- Rule of 40 score reached a record 127%, marking the 10th consecutive quarter of expansion

Beat or Miss?

| Metric | Reported | Consensus Estimate | Difference / Analysis |

| Total Revenue | $1.41 billion | $1.32 billion | Beat by ~$90M (+6.8%) |

| Adjusted EPS | $0.25 | $0.23 | Beat by $0.02 (+8.7%) |

| GAAP EPS (Diluted) | $0.24 | $0.23 | Beat by $0.01 |

| U.S. Commercial Revenue | $507 million | $479 million | Beat by ~$28M (+5.8%) |

| U.S. Government Revenue | $570 million | $522 million | Beat by ~$48M (+9.2%) |

| Adjusted Operating Income | $798.5 million | $701.1 million | Beat by 13.9% (+56.8% margin) |

| Q1 2026 Revenue Guidance | $1.532–$1.536 billion | $1.33 billion (prior) | Crushed by +15.3% |

| FY 2026 Revenue Guidance | $7.18–$7.20 billion | $6.28 billion | Crushed by ~14.5% |

What Leadership Is Saying?

CEO Alex Karp on Strategy and AI Vision:

“Palantir’s Rule of 40 score is now an incredible 127%. Last quarter, our U.S. revenue grew 93% year-over-year and U.S. commercial revenue grew 137% year-over-year. We are also announcing a 2026 revenue growth guide of 61% year-over-year. We are an n of 1, and these numbers prove it. Palantir is alone in choosing to exclusively focus on scaling the operational leverage made possible by the rapid advancements of AI models, a trend that we first called ‘commodity cognition’ well before others started repeating it.”

CFO Dave Glazer on Financials and Execution:

“Our fourth quarter results are nothing short of historic, capping off a monumental year for our business. In Q4, overall revenue surged 70% year-over-year – our highest growth rate as a public company – propelled by the relentless momentum of our U.S. business. The quarter marked our highest reported revenue growth rate as a public company and exceeded the high end of our prior guidance by over 900 basis points.”

Historical Performance

The table below compares Palantir’s Q4 2025 results against the same quarter one year prior (Q4 2024):

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Total Revenue | $1.41 billion | $827.5 million | 70% |

| GAAP Net Income | $609 million | $79 million | 671% |

| Adjusted Operating Income | $798.5 million | $372.5 million | 114% |

| GAAP Operating Income | $575 million | $11 million | 5113% |

| Adjusted EPS | $0.25 | $0.14 | 79% |

| Cash from Operations | $777 million | $460 million | 69% |

| Adjusted Free Cash Flow | $791 million | $517 million | 53% |

| U.S. Commercial Revenue | $507 million | ~$216 million | 135% |

Competitor Performance

The table below benchmarks Palantir’s Q4 2025 results against close AI software competitors over the same comparable period:

| Category | Palantir (Q4 2025) | C3.ai (Q4 CY2025) | Snowflake (Q4 CY2025) |

| Revenue | $1.41 billion | $75.1 million | $1.28 billion |

| Revenue Growth (YoY) | 70% | -20.3% (decline) | +30.1% |

| GAAP Net Income / Loss | +$609 million | Negative (loss) | Operating loss (GAAP) |

| Adjusted Operating Margin | 57% | Negative | ~9% |

| Free Cash Flow | $791 million | N/A | $415 million |

Palantir’s lead over C3.ai has widened dramatically, with Palantir’s revenue now nearly 19 times larger, while Snowflake – the closest comparable by scale – grew at less than half Palantir’s rate. Both C3.ai and Snowflake remain unprofitable on a GAAP basis, whereas Palantir has posted GAAP operating profitability for multiple consecutive quarters.

How the Market Reacted?

Palantir stock climbed more than 12% in premarket trading on February 3, 2026, the morning after the Q4 2025 results were released, reflecting widespread investor optimism about the company’s record-breaking revenue growth and far-above-consensus FY 2026 guidance. The reaction followed a period of pullback for the stock, which had retreated more than 20% year-to-date heading into earnings as high-multiple AI names faced valuation pressure.

Entering the Q1 2026 earnings event on May 4, 2026 – where Palantir has guided for $1.532–$1.536 billion in revenue and Wall Street consensus sits at $1.54 billion, implying 74% year-over-year growth – PLTR was trading near $144, and options markets were pricing in a 10.55% swing in either direction on the earnings day. With Polymarket assigning a 96% probability of an EPS beat, sentiment heading into Q1 2026 results remains strongly bullish.