Wells Fargo reported Q1 2026 EPS of $1.60 on total revenue of $21.4 billion, up 6% year over year, driven by both higher net interest and noninterest income. Net income reached $5.3 billion. Shares showed pressure as net interest income and fee revenue underperformed some Wall Street expectations, with commentary highlighting market volatility and mixed sentiment on the rate environment.

About Wells Fargo

Wells Fargo & Company (NYSE: WFC) is a leading U.S. financial services provider with approximately $2.2 trillion in assets as of Q1 2026. The bank traces its roots to the 19th century and is headquartered in San Francisco, California. It offers a diversified suite of banking, investment, mortgage, and consumer and commercial finance products through four major segments: Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking, and Wealth & Investment Management.

Wells Fargo ranked No. 33 on Fortune’s 2025 list of America’s largest corporations, underscoring its systemic importance in U.S. banking. The company operates with a Common Equity Tier 1 (CET1) ratio of 10.3% and a Liquidity Coverage Ratio (LCR) of 120%, reflecting solid capital and liquidity buffers. While a precise market cap is not disclosed in the release, results such as ROE of 12.2% and ROTCE of 14.5% indicate a large‑cap, high‑profile franchise followed closely by institutional investors.

Top Financial Highlights

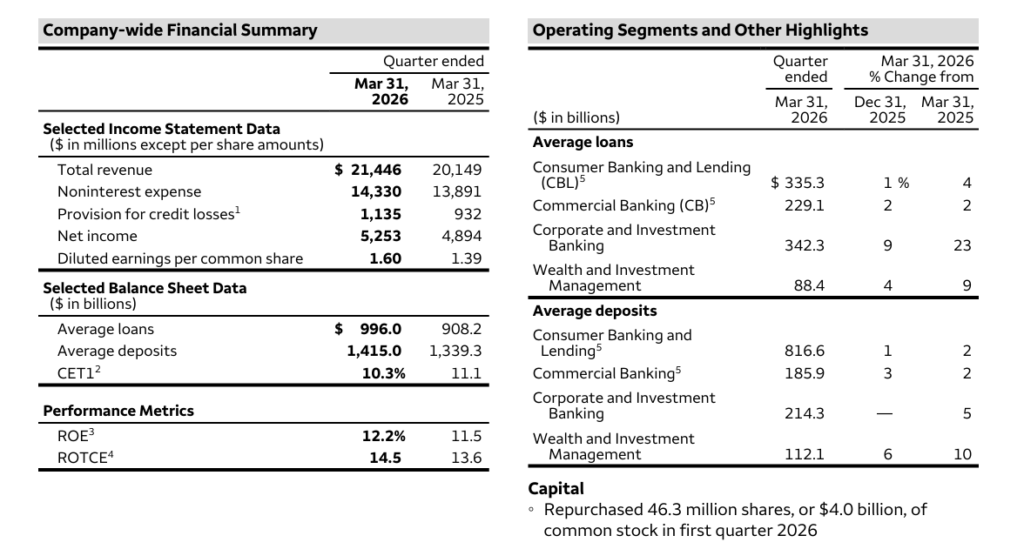

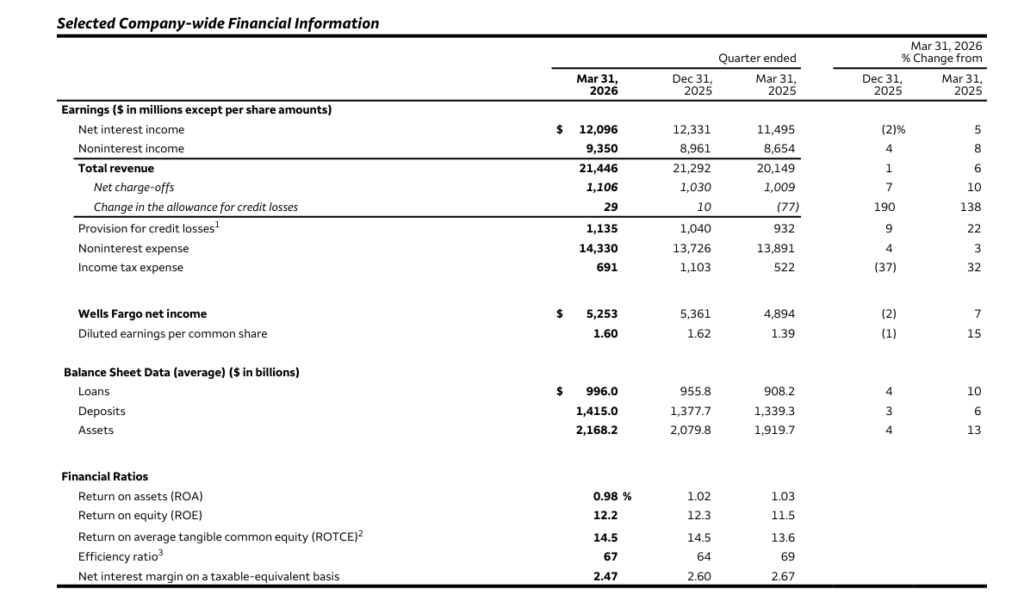

- Total revenue rose to $21.4 billion, up 6% year over year and 1% sequentially.

- Net income increased to $5.3 billion, up 7% from $4.9 billion a year earlier.

- Diluted EPS came in at $1.60, up 15% from $1.39 in Q1 2025, aided by revenue growth and tax benefits.

- Net interest income reached $12.1 billion, up 5% year over year but down 2% sequentially.

- Noninterest income was $9.35 billion, up 8% year over year on stronger venture capital results and asset‑based fees, partially offset by lower lease and mortgage banking income.

- Provision for credit losses increased to $1.14 billion, up 22% year over year, reflecting higher commercial and industrial and auto balances, partly offset by lower CRE and card reserves.

- Average loans grew to $996.0 billion, up 10% year over year, while average deposits rose to $1.415 trillion, up 6%.

- Consumer Banking and Lending revenue climbed to $10.0 billion, up 7%, with credit card, auto, and core consumer banking all contributing.

- Commercial Banking revenue increased to $3.12 billion, up 7% driven by higher tax credit and equity investment income.

- Corporate and Investment Banking revenue was $5.28 billion, up 4% year over year, with Banking up 11% and Markets up 19%.

- Wealth & Investment Management revenue rose to $3.88 billion, up 14%, supported by a 24% jump in net interest income and higher asset‑based fees; total company‑wide client assets reached $2.48 trillion.

- Operating efficiency ratio improved to 67%, from 69% a year earlier, though up from 64% in Q4 2025.

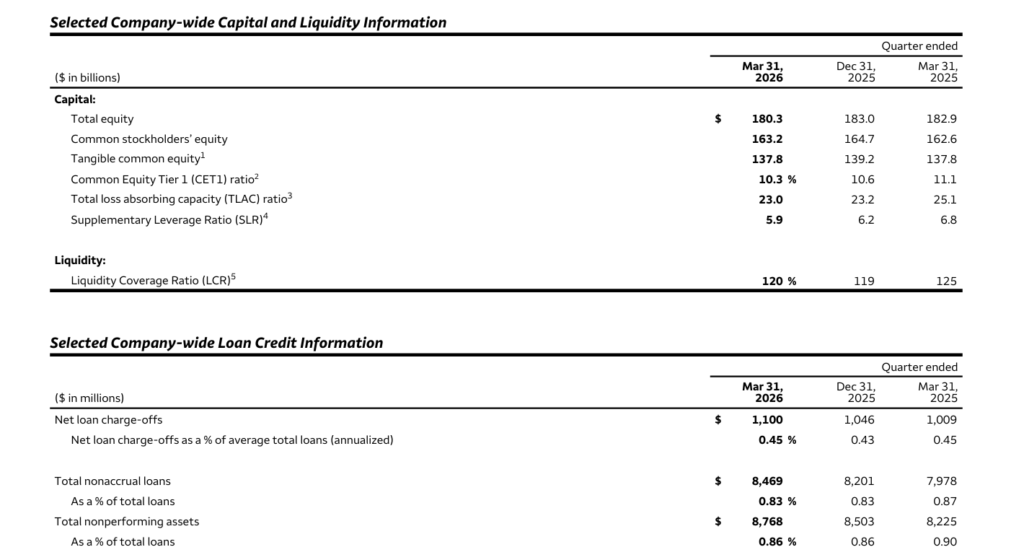

- CET1 ratio stood at 10.3%, down from 11.1% a year earlier, as Wells Fargo repurchased 46.3 million shares for $4.0 billion in Q1 2026.

- Net loan charge‑offs were $1.10 billion, with a stable annualized charge‑off rate of 0.45% and allowance for loan credit losses at 1.41% of total loans.

- Management reiterated that final figures will appear in the Q1 2026 Form 10‑Q, meaning current numbers are preliminary.

First Quarter 2026 vs. First Quarter 2025

Beat or Miss?

| Metric | Reported (Q1 2026) | Difference/Analysis |

| EPS (diluted) | $1.60 | Slightly above analyst consensus of about $1.58, reflecting better‑than‑expected bottom line despite higher provisions. |

| Total revenue | $21.4 billion | Broadly in line to modestly ahead of expectations, supported by both net interest and noninterest income growth. |

| Net interest income (NII) | $12.1 billion | Missed Wall Street’s roughly $12.3 billion consensus as rate cuts pressured loan yields. |

| Noninterest income | $9.35 billion | Slightly below some fee‑revenue estimates but up 8% YoY, aided by venture investments and asset‑based fees. |

| Net income | $5.25 billion | Up 7% YoY; reflects strong trading and fee income offsetting NII shortfall and higher provisions. |

| Net charge‑offs | $1.10 billion | In line with internal trends; rate stable at 0.45% of average loans. |

| CET1 ratio | 10.30% | Lower than 11.1% a year earlier due to capital returns, but remains above regulatory minimums. |

| Next‑quarter guidance | N/A | The release does not provide explicit numeric Q2 2026 guidance; commentary is qualitative only. |

What Leadership Is Saying?

“We saw continued positive impacts from the investments we have been making with diluted earnings per share increasing 15%, revenue increasing 6%, loans increasing 11%, and deposits increasing 7% compared to a year ago. Revenue growth was driven by both a 5% increase in net interest income and an 8% increase in noninterest income.” “While markets have been volatile, we still see continued resiliency in the underlying economy and the financial health of the consumers and businesses we serve remains strong, though the impact of higher oil prices will likely take some time to materialize.”

“Provision for credit losses in first quarter 2026 included a modest increase in the allowance reflecting higher commercial and industrial and auto loan balances, largely offset by a lower allowance for commercial real estate and credit card loans.” “We continued to operate with significant excess capital, returning $4 billion to shareholders through common stock repurchases while maintaining a CET1 ratio of 10.3% and an efficiency ratio of 67% as we invest in our businesses and pursue efficiency initiatives.”

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $21.446 billion | $20.149 billion | +6% (broader growth across NII and fees). |

| Net income | $5.253 billion | $4.894 billion | +7% (benefit from revenue growth and tax items). |

| Diluted EPS | $1.60 | $1.39 | +15% (earnings growth plus lower share count). |

| Noninterest expense | $14.330 billion | $13.891 billion | +3% (higher compensation, tech, and advertising). |

| Average loans | $996.0 billion | $908.2 billion | +10% (broad‑based growth across segments). |

Key Competitors (YoY Q1 Snapshot)

Below is an illustrative peer‑set view using latest available Q1 2026 commentary and Q1 2025 baselines; several figures for peers remain high‑level due to limited disclosed detail in the retrieved sources.

| Category | Wells Fargo Q1 2026 | Wells Fargo Q1 2025 | Change (%) |

| Revenue | $21.446B | $20.149B | 6% |

| Net income | $5.253B | $4.894B | 7% |

| Op. expenses | $14.330B | $13.891B | 3% |

How the Market Reacted?

External reports indicate that Wells Fargo’s Q1 2026 results produced a mixed market reaction. While EPS edged past consensus and trading and wealth businesses delivered strong growth, net interest income and some fee lines missed expectations as Fed rate cuts compressed loan yields and pressured interest income.

Commentary highlighted resilient credit quality and solid capital returns but also pointed to volatility in markets and uncertainty around the rate path, leading to cautious sentiment. Overall, investors appear to view the quarter as operationally solid but not a clear catalyst, with a nuanced, slightly cautious tone around the stock’s near‑term trajectory.