Verde AgriTech reported FY 2025 basic EPS of -$0.22 (improved from -$0.24 in FY 2024) on revenue of $16.6 million CAD, down 23% year over year. Q4 2025 revenue rose slightly to $3.1M from $2.9M in Q4 2024. No specific stock price movement was reported on the earnings date; after-hours movement was not disclosed in the press release.

About Verde AgriTech

Verde AgriTech Ltd (TSX: NPK | OTCQX: VNPKF) is a Brazil-focused specialty fertilizer company founded in 2005 and headquartered in Belo Horizonte, Brazil, with additional offices in Singapore. The company produces and markets multi-nutrient potassium fertilizers sold under the K Forte, BAKS, and Super Greensand brands, targeting the Brazilian agricultural market.

Verde holds a 100% interest in the Cerrado Verde project located in Minas Gerais State, Brazil, and has recently disclosed a district-scale clay-hosted rare earth discovery at its Minas Americas Global Alliance project. As of March 2026, Verde’s market capitalization stood at approximately C$62.65 million, with 56.44 million shares outstanding.

The company does not pay a dividend and carries no positive P/E ratio given its current loss position. Verde reported a net margin of approximately -67.78% and a return on equity of -44.81% as of the last earnings update. The company employs a lean workforce and is implementing workforce reductions as part of BRL 6 million in cost-efficiency initiatives announced in early 2026.

Top Financial Highlights

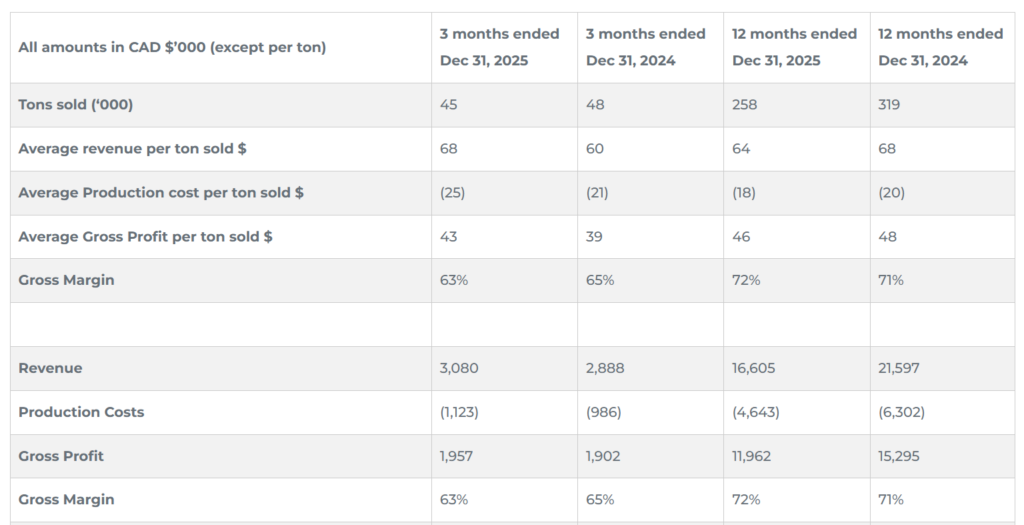

- FY 2025 Revenue was $16.6 million CAD, compared to $21.6 million in FY 2024, a decline of 23.1%

- Q4 2025 Revenue increased to $3.1 million (C$3,080K), up from $2.9 million (C$2,888K) in Q4 2024

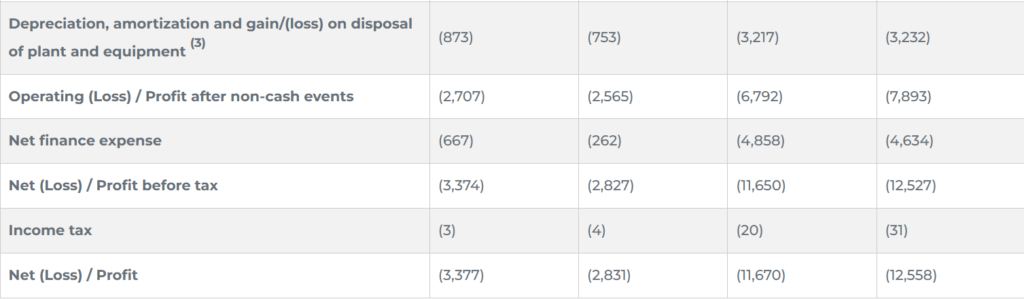

- FY 2025 Net Loss narrowed to $(11.7) million, improving from $(12.6) million in FY 2024

- Q4 2025 Net Loss was $(3.4) million, compared to $(2.8) million in Q4 2024

- Basic EPS for FY 2025 was $(0.22), compared to $(0.24) in FY 2024

- FY 2025 Gross Margin held at 72%, slightly improved from 71% in FY 2024

- Q4 2025 Gross Margin was 63%, down from 65% in Q4 2024

- FY 2025 Sales Volume totaled 258,432 tons, down from 318,870 tons in FY 2024

- Q4 2025 Sales Volume was 45,113 tons, compared to 47,888 tons in Q4 2024

- Cash on Hand as of December 31, 2025 was $3.0 million, with an additional $5.3 million in short-term receivables

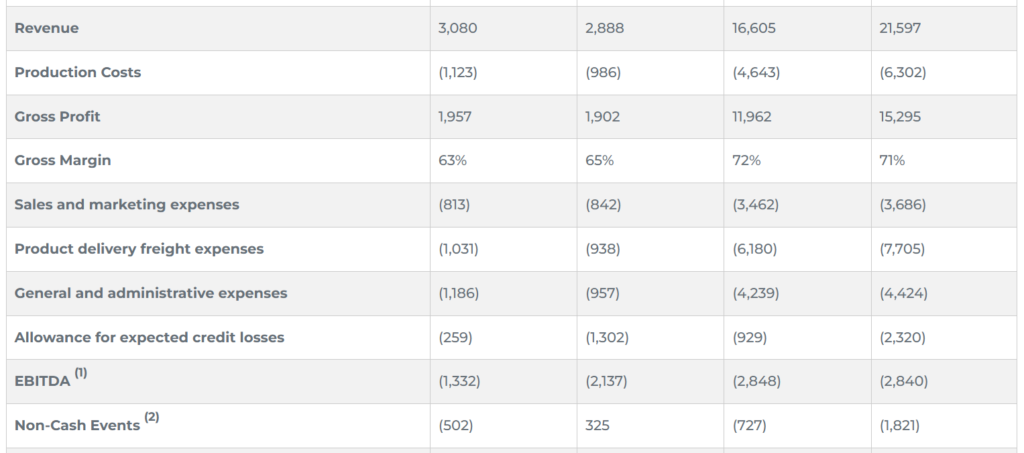

- EBITDA before non-cash events for FY 2025 remained stable at $(2.8) million, same as FY 2024

- Q4 2025 EBITDA improved to $(1.3) million from $(2.1) million in Q4 2024

- Allowance for expected credit losses declined sharply to $0.9 million in FY 2025 from $2.3 million in FY 2024

- Net cash used in operating activities narrowed to $(0.03) million in FY 2025, from $(1.9) million in FY 2024

- Subsequent to year-end, Verde completed a brokered private placement for gross proceeds of $4.5 million to fund rare earth project advancement

Beat or Miss?

No external analyst consensus estimates were publicly available for Verde AgriTech’s Q4 and FY 2025 results, given the company’s micro-cap status. The table below compares reported figures to the previous year’s actuals as the primary reference benchmark.

| Metric | Q4 2025 Reported | Q4 2024 Reported | Difference / Analysis |

| Revenue | C$3.08M | C$2.89M | +6.6% improvement; positive inflection in Q4 |

| Gross Margin | 63% | 65% | -200 bps; freight and input cost pressures |

| Net Loss | $(3.4)M | $(2.8)M | Wider loss; higher finance & G&A costs in Q4 |

| EBITDA (pre-non-cash) | $(1.3)M | $(2.1)M | Significant 38% improvement year over year |

| Sales Volume (tons) | 45,113 | 47,888 | -5.8%; credit tightening reduced high-risk sales |

| Allowance for Credit Losses | $0.3M | $1.3M | -77% reduction; key quality improvement signal |

| EPS (Basic, FY) | ($0.22) | ($0.24) | Modest improvement; losses narrowing |

| Cash on Hand (FY-end) | $3.0M | $3.5M | Slight decline; post-period placement adds $4.3M |

What Leadership Is Saying?

CEO on Market Conditions and Strategy:

“The Great Brazilian Agriculture Crisis continued to weigh on sales throughout 2025, and the sharp rise in judicial recovery filings across Brazil’s agribusiness sector shows how stressed the market remains. Since the crisis began in 2023, Verde has maintained a highly restrictive credit approval policy, prioritizing receivables quality, liquidity preservation and commercial discipline over volume at any cost. We believe this has been the right approach to protect the Company and preserve its ability to grow when sector credit conditions begin to normalize.” – Cristiano Veloso, Founder and CEO of Verde AgriTech

CFO / Financial Perspective (from Financial Results Commentary):

“Net cash used in operating activities narrowed materially to $(0.03) million in FY 2025, compared to $(1.9) million in FY 2024, primarily reflecting tighter credit underwriting and working capital management, which helped stabilize cash flow despite weaker sales.” – Verde AgriTech FY 2025 Financial Results Statement

Historical Performance

Verde AgriTech Year-over-Year Comparison

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Revenue | C$3.08M | C$2.89M | 6.60% |

| Net Loss | $(3.38)M | $(2.83)M | -19.4% (wider loss) |

| Gross Profit | C$1.96M | C$1.90M | 3.10% |

| Gross Margin | 63% | 65% | -200 bps |

| G&A Expenses | C$1.19M | C$0.96M | 24% |

| EBITDA (pre-non-cash) | $(1.33)M | $(2.14)M | +37.8% improvement |

| Sales Volume (tons) | 45,113 | 47,888 | -5.80% |

| Avg. Revenue per Ton | C$68 | C$60 | 13.30% |

| Category | FY 2025 | FY 2024 | Change (%) |

| Revenue | C$16.6M | C$21.6M | -23.10% |

| Net Loss | $(11.67)M | $(12.56)M | +7.1% improvement |

| Gross Profit | C$11.96M | C$15.30M | -21.80% |

| Gross Margin | 72% | 71% | +100 bps |

| G&A Expenses | C$4.24M | C$4.42M | -4.10% |

| Sales Volume (tons) | 258,432 | 318,870 | -18.90% |

| Basic EPS | ($0.22) | ($0.24) | +8.3% improvement |

Competitor Year-over-Year Comparison

Verde AgriTech operates as a micro-cap specialty fertilizer producer in Brazil, while its larger industry peers Nutrien and Mosaic are global commodity fertilizer giants. Their FY 2025 results are included for sector context.

| Category | Verde AgriTech FY 2025 | Verde AgriTech FY 2024 | Change (%) |

| Revenue | C$16.6 | C$21.6Mwire | -23.10% |

| Net Income / Loss | $(11.67)M | $(12.56)M | +7.1% improvement |

| Gross Margin | 72% | 71% | +100 bps |

| Category | Nutrien (NTR) FY 2025 | Nutrien (NTR) FY 2024 | Change (%) |

| Revenue | USD 26,885M | USD 25,972M | 3.50% |

| Net Income | USD 2,267M | USD 674M | 236% |

| Adjusted EBITDA | USD 6.05B | USD 5.35B (est.) | 13% |

| Category | Mosaic (MOS) FY 2025 | Mosaic (MOS) FY 2024 | Change (%) |

| Revenue | USD 12,052M | USD 11,123M | 8.30% |

| Net Income | USD 540.7M | USD 174.9M | 209% |

| Adjusted EBITDA | USD 2.4B | USD 2.2Btradingview | 10% |

How the Market Reacted?

Verde AgriTech’s Q4 and FY 2025 earnings press release, dated March 26, 2026, did not include specific commentary on same-day stock price movement. The company’s TSX-listed shares (NPK) had traded in a wide 52-week range of C$0.44 to C$2.73, reflecting the speculative nature of the stock driven by both fertilizer fundamentals and the rare earth project announcement in October 2025. A buy signal was noted from a pivot bottom on March 16, 2026, with the stock having risen approximately 5.71% from that point.

The report’s tone is broadly neutral to cautiously constructive: operating cash flow nearly breakeven, EBITDA improving in Q4, and credit loss provisions sharply reduced all represent incremental positives, while the narrowing net loss and a successful $4.5 million post-period placement provide modest liquidity support. Market sentiment remains mixed, balancing ongoing sector stress in Brazilian agriculture against Verde’s pivot toward a higher-margin rare earth discovery narrative.