Hemlo Mining Corp. (TSXV: HMMC | OTCQX: HMMCF) reported its inaugural revenue quarter as a gold producer in Q1 2026, posting revenue of $186.3 million and EPS of $0.07 per share. Net income reached $22.1 million. The stock traded near C$5.85 to C$6.35 around the earnings release, reflecting some consolidation after hitting a 52-week high of C$8.05 in February 2026. After-hours movement was not separately disclosed in the press release.

About Hemlo Mining Corp.

Hemlo Mining Corp. (TSXV: HMMC | OTCQX: HMMCF) is a Canadian gold producer headquartered in Toronto, Ontario. The company was formed through the amalgamation of Carcetti Capital Corp. and its subsidiary on November 27, 2025, with the operational history of the Hemlo Gold Mine dating back to 1985.

Its flagship asset, the Hemlo Gold Mine, is located near Marathon in northwestern Ontario along the Trans-Canada Highway, and has produced approximately 25 million ounces of gold since inception. Hemlo Mining trades with a market capitalization of approximately C$1.83 billion, with 296.37 million shares outstanding as of May 2026.

The company employs 294 people as of its most recent reporting. Q1 2026 marks the first full quarter the company operated and generated revenue from the Hemlo Gold Mine following its acquisition from Barrick Mining Corporation on November 26, 2025, for total consideration with a fair value of approximately $1.0 billion.

The P/E ratio is not applicable given the company’s short reported earnings history, and no dividend is currently paid. The EPS (TTM) stood at approximately -C$1.39, reflective of acquisition-related costs in prior periods.

Top Financial Highlights

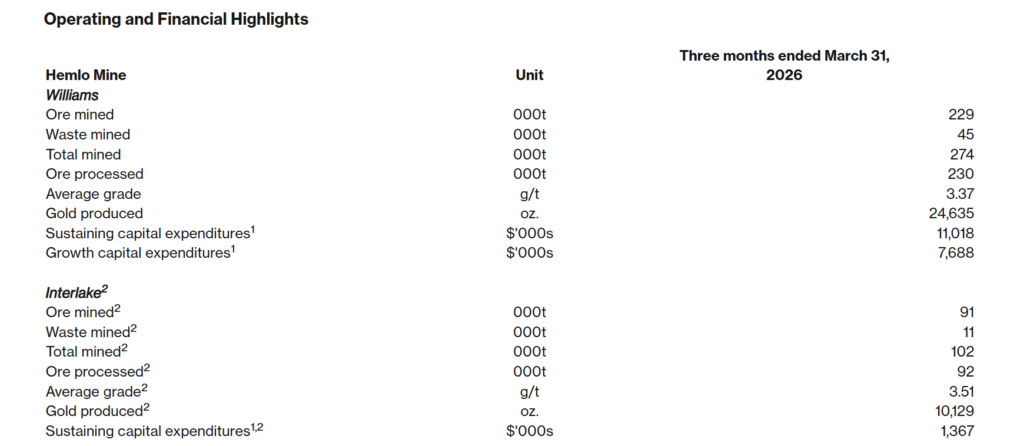

- Revenue of $186.3 million for the three months ended March 31, 2026, entirely from gold sales

- Total gold sold of 38,685 ounces at an average realized price of $4,923 per ounce

- Attributable gold produced of 29,699 ounces (Williams 100% + 50% of Interlake), total gold produced of 34,764 ounces

- Net income of $22.1 million, or $0.07 per share (basic EPS)

- Gross profit of $73.2 million (revenue of $186.3 million less cost of sales of $113.1 million)

- EBITDA of $86.6 million for the quarter

- Cash generated from operating activities of $87.9 million

- Free cash flow of $71.5 million generated during the quarter

- Cash on hand of $123.6 million as at March 31, 2026

- Net debt reduced to $26.2 million (from $93.0 million at December 31, 2025)

- Repaid $75.0 million outstanding under the Revolving Credit Facility in March 2026

- Site attributable cash cost per ounce sold of $1,385 and all-in sustaining cost (AISC) per ounce sold of $1,805

- Income tax expense of $23.6 million; G&A expense of $7.9 million (including share-based compensation of $4.4 million)

- 2026 full-year guidance: Company expects to provide production and cost guidance in the second half of 2026

Beat or Miss?

As Q1 2026 represents Hemlo Mining’s first full operating quarter as a gold producer, no analyst consensus estimates for quarterly EPS or revenue have been widely published against which the company can be formally benchmarked. Moomoo data indicates an EPS estimate of $0.13, against which the reported $0.07 represented a miss. The table below summarizes available reported figures against available or contextual reference points.

| Metric | Reported | Estimated / Expected | Difference / Analysis |

| Revenue | $186.3 million | N/A (first operating quarter) | First-quarter gold revenue since Hemlo Acquisition |

| EPS (Basic) | $0.07 per share | $0.13 (analyst estimate) | Miss of approximately -46.2% |

| Gross Profit | $73.2 million | N/A | Gross margin of approximately 39.3% |

| EBITDA | $86.6 million | N/A | Strong operational leverage on gold price |

| Cash from Operations | $87.9 million | N/A | Ahead of capex requirements for the quarter |

| Cash Position | $123.6 million | N/A | Balance sheet strengthened after RCF repayment |

| AISC per oz sold | $1,805/oz | N/A | Favorable vs. $4,923 realized price |

| Gold Produced (Attributable) | 29,699 oz | In line with company expectations | Management described production as “in line with expectations” |

What Leadership Is Saying?

CEO on Strategy and Vision:

“Q1 was transformational for the Company, representing our first full quarter of ownership of the Hemlo Gold Mine and laying a strong foundation for the year ahead. We delivered production in line with expectations while upholding our standards for health, safety, and environmental performance. During the quarter, we advanced our strategy of optimization, reinvestment, and growth across multiple fronts — transitioning to an owner-operated model ahead of schedule; launching our 130,000-metre drill program; advancing an updated mineral resource estimate;

initiating key mining trade-off studies to support a future technical study; making strong progress transitioning off legacy Barrick systems; hiring key personnel across corporate and site functions; and executing a strategic royalty buyback. We also strengthened our financial position through the full repayment of our revolving credit facility. The pace and breadth of progress in the first quarter reinforce our confidence in the opportunity ahead at Hemlo.” — Jason Kosec, President, CEO and Director

CFO on Financials and Balance Sheet:

“The $75.0 million RCF repayment, completed less than six months after closing the acquisition of the Hemlo Gold Mine, reflects the strong cash flow generation of the asset and the financial discipline of our team. This repayment marks a meaningful step in deleveraging the business as we advance our 2026 strategy focused on operational optimization and growth.” — Jon Case, Chief Financial Officer

Historical Performance

Because Q1 2025 predates the Hemlo Acquisition (completed November 26, 2025), the company had no gold production or revenue in Q1 2025 and was operating as a shell company with minimal activity. The table below compares Q1 2026 to Q1 2025 (restated) as disclosed in the company’s own MD&A.

| Category | Q1 2026 | Q1 2025 (Restated) | Change (%) |

| Revenue | $186.3 million | $0 (nil) | N/A (first operating quarter) |

| Net Income (Loss) | $22.1 million | ($13,000) | N/A (pre-acquisition shell) |

| Cash from Operating Activities | $87.9 million | ($25,000) | N/A (no operations) |

| Gold Produced (Attributable) | 29,699 oz | 0 oz | N/A |

| Cash on Hand | $123.6 million | Minimal | N/A |

| Net Debt | $26.2 million | N/A | Significantly reduced from $93.0M at Dec 31, 2025 |

Competitor Historical Performance

Q1 2026 vs Q1 2025

The following table compares two prominent Canadian gold mining peers, Agnico Eagle Mines (TSX/NYSE: AEM) and Kinross Gold Corporation (TSX: K / NYSE: KGC), across Q1 2026 and Q1 2025.

Agnico Eagle Mines (AEM)

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $4.10 billion | $2.47 billion | 66.10% |

| Net Income | $1.70 billion | $815 million | 108.60% |

| Operating Cash Flow | $1.35 billion | $1.04 billion | 28.90% |

| EPS (Basic) | $3.39 | $1.62 | 109.30% |

| AISC per oz sold | $1,483 | $1,183 | 25.40% |

Kinross Gold (KGC)

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue (Metal Sales) | $2,407.7 million | $1,497.5 million | 60.80% |

| Net Income (Attributable) | $843.0 million | $368.0 million | 129.10% |

| Operating Cash Flow | $1,139.5 million | $607.1 million | 87.70% |

| EPS (Basic) | $0.70 | $0.30 | 133.30% |

| AISC per oz sold (Attributable) | $1,732 | $1,355 | 27.80% |

All three companies benefited from materially higher realized gold prices in Q1 2026. Agnico Eagle reported a realized gold price of approximately $4,861/oz, Kinross reported $4,873/oz, and Hemlo Mining reported $4,923/oz attributable, all broadly in line with prevailing gold market prices during the period.

How the Market Reacted?

The stock (TSXV: HMMC) traded at approximately C$6.35 on May 20, 2026, the day the financial results were released, and slipped approximately 7.7% to 7.9% intraday reaching lows near C$5.75 to C$5.85 during the session. This move followed the stock’s 52-week high of C$8.05 reached on February 25, 2026, and the shares have been consolidating since then. Stifel Canada previously maintained a Buy rating on HMMC with a price target of C$12.00 following Q4 2025 results.

The Q1 earnings miss on an EPS basis (reported $0.07 vs. estimated $0.13) appears to have contributed to near-term selling pressure, though the broader sentiment toward the stock remains constructive given management’s progress on the owner-operator transition, the Revolving Credit Facility repayment, and the launch of a 130,000-metre exploration drill program. Analysts point to an analyst consensus price target of approximately C$9.00, suggesting potential upside from current levels.