iHuman reported Q4 2025 diluted EPS of RMB 0.29 (US$0.04) and revenue of RMB 190.7 million (US$27.3 million), down 18.1% from a year earlier. Full-year revenue was RMB 807.0 million (US$115.4 million), a 12.5% decline, while the stock showed a modestly positive after-hours move around the release date.

About iHuman Inc.

iHuman Inc. (NYSE: IH) is a Beijing-based company focused on digital learning and intellectual development products for young children. It offers apps, interactive content, and smart devices that cover Chinese literacy, English, coding, math, and creative subjects for roughly ages three to eight. The company leverages technology, animation, and game-like experiences to keep children engaged while they build core skills.

As of early 2026, iHuman has a market capitalization of about US$80–85 million and trades on the New York Stock Exchange under the ticker IH. Public data shows a relatively low price-to-earnings ratio and a dividend yield supported in part by recurring special dividends. The firm traces its roots to a long history in the children’s education industry in China and now sells into both domestic and overseas markets through major app stores.

Top Financial Highlights

- Revenue for the quarter reached RMB 190.7 million (US$27.3 million), down 18.1% year over year.

- Gross profit was RMB 127.5 million, lower than the prior-year quarter.

- Gross margin stood at 66.9%, slightly below 67.2% a year earlier.

- Operating income was RMB 9.0 million (about US$1.3 million), declining from the prior year.

- Net income totaled RMB 15.4 million (around US$2.2 million), down more than 40% year over year.

- Diluted EPS per ADS was RMB 0.29 (US$0.04), compared with RMB 0.49 a year earlier.

- Total operating expenses were RMB 118.5 million, down about 16% from the prior year.

- Research and development expenses were RMB 44.9 million, reflecting lower spending levels.

- Sales and marketing expenses reached RMB 52.7 million, slightly lower than the previous year.

- General and administrative expenses were RMB 20.8 million, also declining year over year.

- Average total monthly active users were 23.57 million, compared with 25.78 million in Q4 2024.

- Total annual revenue reached RMB 807.0 million (about US$115.4 million), reflecting a 12.5% decline from 2024.

- Annual net income stood at RMB 95.4 million (about US$13.6 million), slightly lower than the prior year while remaining positive.

- Gross margin for the year was 67.9%, down from 69.4% in 2024.

- Total operating expenses for the year were RMB 480.9 million, about 15% lower than in 2024.

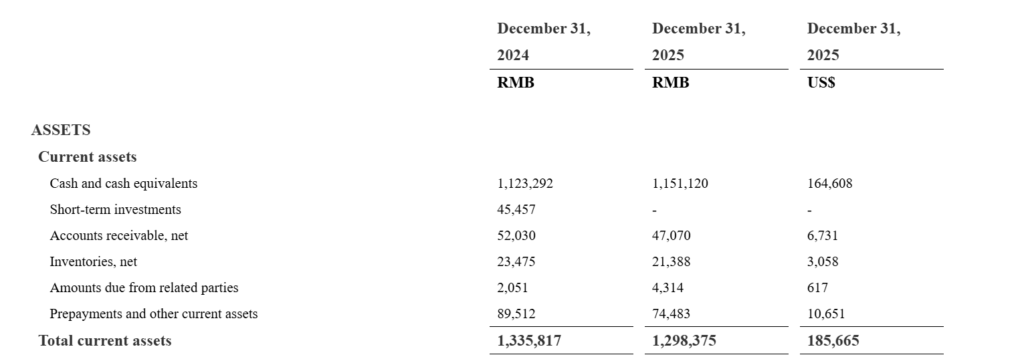

- Cash, cash equivalents, and short-term investments totaled RMB 1,151.1 million (around US$160 to 165 million) at year-end.

- Deferred revenue and customer advances reached RMB 219.9 million, indicating a solid base of prepaid services.

- Average total monthly active users for 2025 were 24.98 million, down from 26.47 million in 2024.

- A special cash dividend of US$0.10 per ADS was approved, with a total payout of about US$5.1 million scheduled for May 2026.

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands of Renminbi (“RMB”) and U.S. dollars (“US$”) except for number of shares, ADSs, per share and per ADS data)

Beat or Miss?

| Metric | Reported (Q4 2025) | Prior Year (Q4 2024) | Difference / Analysis |

| Revenue | RMB 190.7M (US$27.3M) | RMB 232.7M (about US$31.9M) | About 18.1% year-over-year decline in revenue |

| Gross profit | RMB 127.5M | RMB 156.4M | Gross profit down by high teens percentage |

| Gross margin | 66.90% | 67.20% | Slight compression of around 0.3 percentage points |

| Operating income | RMB 9.0M | RMB 14.9M | Operating profit lower by nearly 40% |

| Net income | RMB 15.4M | RMB 26.5M | Net income down more than 40% |

| Diluted EPS (per ADS) | RMB 0.29 | RMB 0.49 | Earnings per share lower by around 40% |

| Total operating expenses | RMB 118.5M | RMB 141.5M | Expenses reduced by about 16%, partly offsetting revenue drop |

| Average total MAUs | 23.57M | 25.78M | Active users declined by about 8-9% |

What Leadership Is Saying

“During the fourth quarter, we executed our key strategic plans and kept operations steady in a changing environment. As demographic trends reshape the children’s education sector, we have adjusted our product mix to support long-term stability. The launch of FreeTalk marks a major step in expanding beyond early childhood learning, increasing our addressable market and extending how long we can serve users. In 2026, we plan to keep investing in product development, content quality, and technology so we can improve user experience and learning outcomes.” – Dr. Peng Dai, Director and Chief Executive Officer

“In the quarter, we achieved better progress in our international business, where our global products gained wider recognition. Aha World, our open-ended digital world focused on exploration and creativity, performed especially well. From Thanksgiving through the New Year period, daily active users on the US Apple App Store rose by about 30%. Our board has approved a special cash dividend of US$0.02 per ordinary share, or US$0.10 per ADS, with a total of around US$5.1 million, the third year in a row that we have paid a special dividend, which reflects our confidence in the company’s financial strength.”– Ms. Vivien Weiwei Wang, Director and Chief Financial Officer

Historical Performance

Q4 year-over-year

| Category | Q4 2025 | Q4 2024 | Change (%) |

| Revenue | RMB 190.7M (US$27.3M) | RMB 232.7M (about US$31.9M) | Around -18.1% |

| Gross profit | RMB 127.5M | RMB 156.4M | Around -18.5% |

| Net income | RMB 15.4M | RMB 26.5M | Around -41.8% |

| Total operating expenses | RMB 118.5Mnasdaq | RMB 141.5M | Around -16.3% |

| R&D expenses | RMB 44.9M | RMB 63.3M | Around -29.0% |

| Sales and marketing | RMB 52.7M | RMB 54.1M | Around -2.6% |

| General and administrative | RMB 20.8M | RMB 24.1M | Around -13.7% |

| Average total MAUs | 23.57M | 25.78M | Around -8.6% |

| Diluted EPS (per ADS) | RMB 0.29 | RMB 0.49 | Around -40.8% |

Full-year comparison (2025 vs 2024)

| Category | FY 2025 | FY 2024 | Change (%) |

| Revenue | RMB 807.0M (about US$115.4M) | RMB 922.2M | Around -12.5% |

| Gross profit | RMB 547.6M | RMB 640.2M | Around -14.5% |

| Net income | RMB 95.4M | RMB 98.6M | Low single-digit decline |

| Total operating expenses | RMB 480.9M | RMB 568.2M | Around -15.4% |

| Gross margin | 67.90% | 69.40% | Compression of about 1.5 percentage points |

| Average total MAUs | 24.98M | 26.47M | Around -5.6% |

| Diluted EPS (per ADS) | RMB 1.78 | RMB 1.82 | Slight decline |

Historical Performance of Competitors

| Company | Category / Focus | Revenue Trend (2024–2025) | Net Income Trend | Notes |

| iHuman (IH) | Early childhood digital learning | Revenue down about 12.5% year over year | Remains profitable | Focused on ages 3-8 and gamified learning |

| TAL Education (TAL) | K–12 and non-academic education | Recovering after regulatory shock | Margins improving from low base | Pivot to non-academic and quality education |

| New Oriental (EDU) | Education, test prep, live commerce | Growth from live-streaming commerce | Profitability rebuilt | Larger, more diversified business |

| Other digital players | Broader digital content and children’s apps | Mixed, often not separately disclosed | Varies by segment | Includes app-store based competition |

How the Market Reacted?

Around the Q4 and full-year 2025 announcement at the end of March 2026, iHuman’s shares showed a small positive move in after-hours trading, with prices reported in the low US$1 range and a gain of roughly mid-single-digit percentages after the release. Over the surrounding week, the stock was slightly lower, which reflects concern about falling revenue and lower user metrics.

Investors appear to be balancing that weakness against the company’s continued profitability, strong cash position, and another special cash dividend. The overall tone of the report is cautious but supportive of the view that iHuman is managing costs and searching for new growth through products like FreeTalk and Aha World.