Local Bounti reported a net loss of $12.7 million and adjusted EBITDA loss of $5.7 million on revenue of $13.3 million, with 15% top line growth and improved margins year over year, while shares’ after-hours movement was not disclosed in the release.

About Local Bounti

Local Bounti Corporation (NYSE: LOCL) is a U.S. controlled environment agriculture company that operates advanced indoor growing facilities and services approximately 13,000 retail doors across the country. It uses its patented Stack & Flow Technology to grow lettuce and other leafy greens with about 90% less land and 90% less water than conventional farming methods, positioning the business as a sustainability focused supplier to national and regional grocers.

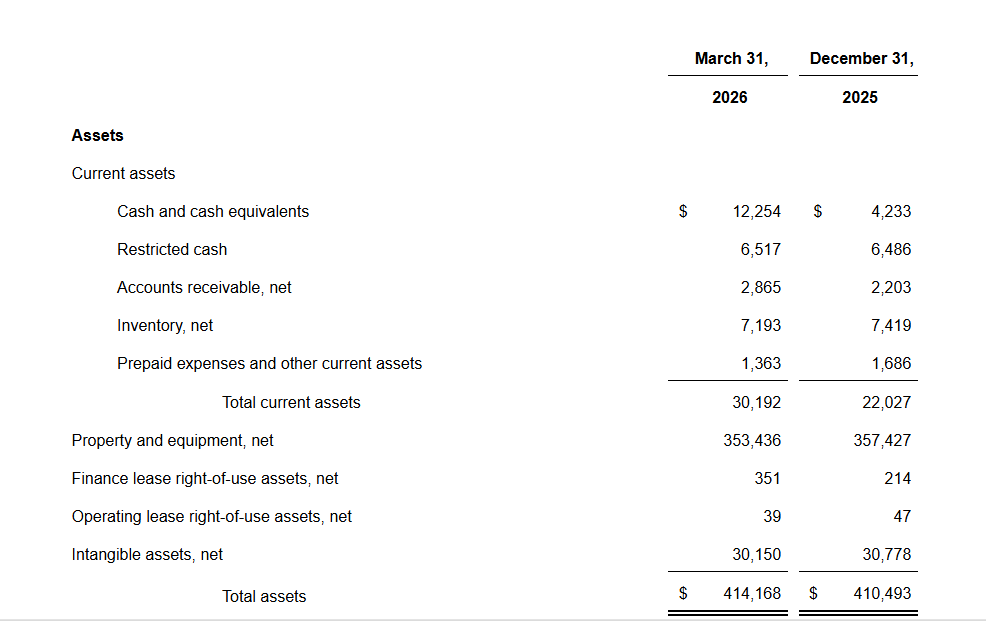

Headquartered in Hamilton, Montana, the company ended the first quarter of 2026 with total assets of $414.2 million and a stockholders’ deficit of $178.0 million, reflecting a capital intensive growth model funded largely through debt. Local Bounti had approximately 22.8 million common shares outstanding and a fully diluted share count of about 41.6 million as of March 31, 2026, but the press release did not disclose market capitalization, P/E ratio, dividend yield, or employee count.

Top Financial Highlights

- Sales increased 15% to $13.3 million in Q1 2026 from $11.6 million in Q1 2025, driven by higher production and growth at facilities in Georgia, Texas, and Washington.

- Gross profit was $1.5 million, essentially flat versus $1.5 million in the prior year quarter.

- Adjusted gross margin was 29%, stable compared with both Q1 2025 and Q4 2025, after excluding depreciation, stock based compensation, and other non core items.

- Net loss improved to $12.7 million from a net loss of $37.7 million a year earlier, helped by sharply lower net interest expense following 2025 debt restructuring.

- Net interest expense fell to $4.0 million in Q1 2026 from $18.8 million in Q1 2025, delivering a key driver of bottom line improvement.

- Adjusted EBITDA loss improved 35% to $5.7 million, compared with a loss of $8.8 million in the prior year quarter.

- General and administrative expenses decreased to $7.5 million from $8.1 million, reflecting cost savings across the organization.

- Adjusted general and administrative expense fell 30% to $4.1 million, versus $5.8 million in Q1 2025, after excluding stock based compensation, depreciation, and other non core items.

- The company recorded a $5.2 million gain from change in fair value of warrant liabilities, compared with a $3.5 million loss from this item in the prior year period.

- Cash, cash equivalents, and restricted cash totaled $18.8 million at March 31, 2026, giving management some flexibility as it pursues growth and partnership initiatives.

- Local Bounti received a $15 million investment from an existing strategic investor in March 2026, supplementing prior 2025 capital actions.

- The company’s long term debt principal stood at $328.0 million at quarter end, with net long term debt (including premium and discount) of $490.8 million and accrued interest of $19.0 million.

- Management reiterated its expectation for continued sequential improvements in revenue and adjusted EBITDA loss rate in 2026, targeting a path toward positive adjusted EBITDA.

- Local Bounti reported that tower upgrades completed in 2025 have delivered an approximate 10% increase in run rate yield capacity, with additional yield gains expected from select investments in California facilities.

- The company currently supports a six SKU rollout across more than 250 stores for a large premier retail customer and continues strong growth with a major e commerce and DTC customer following more than 600% sales growth in 2025.

Beat or Miss?

Analyst consensus estimates were not cited in the company’s press release, so the comparison is framed against expectations mentioned qualitatively and uses “N/A” where explicit numbers are absent.

| Metric | Reported Q1 2026 | Difference/Analysis |

| Revenue | $13.3 million | Up 15% year over year, reflecting higher production and new retail wins |

| Net loss | $12.7 million | Material improvement vs $37.7 million in Q1 2025, aided by lower interest expense |

| Adjusted EBITDA | $(5.7) million | 35% better than $(8.8) million last year, signaling operating leverage progress |

| Gross margin | 11.5% GAAP, 29% adjusted | Gross profit stable, with adjusted margin steady year over year |

| EPS (basic/diluted) | $(0.53) | Improved vs $(4.32) a year ago but still clearly loss making |

| Operating cash flow | N/A | Not separately detailed in the press release |

| Guidance vs consensus | N/A | Company guided to sequential improvements but did not disclose Street expectations |

What Leadership Is Saying?

“Our first quarter results reflect the operating discipline this team has built over the past several quarters — 15% revenue growth, a 35% improvement in adjusted EBITDA loss, and a 30% reduction in adjusted G&A year-over-year. The improvement is grounded in tangible operating progress as our network is now running at full utilization, and the tower upgrades completed across our facilities last year are delivering an approximate 10% increase in run-rate yield capacity, with additional gains expected from the targeted investments we’re making in California to support our leading market position in living butterhead lettuce. Each quarter brings us closer to positive adjusted EBITDA, and I’m proud of the consistency our team continues to deliver.”

— Kathleen Valiasek, President and CEO, Local Bounti

“Two developments this quarter reinforce the long-term thesis for Local Bounti. The U.S. patent issued in February for our AI-driven growing optimization supports the competitive advantages we have built around our Stack and Flow platform, and the additional $15 million committed by an existing strategic investor signals continued conviction in where we’re headed. We continue to advance strategic partnership discussions and believe that we are in great position to capture demand for efficient capacity as the industry continues its migration to CEA products.”

— Craig Hurlbert, Executive Chairman, Local Bounti

Historical Performance

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $13.337 million | $11.605 million | 14.90% |

| Net Loss | -$12.718 million | -$37.675 million | -66.20% |

| Total Operating Expenses | $15.468 million | $17.195 million | -10.00% |

| Gross Profit | $1.534 million | $1.461 million | 5.00% |

| Adjusted EBITDA Loss | -$5.699 million | -$8.782 million | -35.10% |

| Adjusted G&A Expense | $4.066 million | $5.815 million | -30.10% |

| EPS (Basic and Diluted) | ($0.53) | ($4.32) | 87.7% |

Competitor Landscape

The controlled environment agriculture sector has seen significant consolidation. AppHarvest filed for Chapter 11 bankruptcy in July 2023, and Plenty Unlimited filed for Chapter 11 in March 2025, while AeroFarms also underwent restructuring. Gotham Greens remains one of the few private peers still operating at scale, with an estimated annual revenue of approximately $76.9 million to $84 million. The table below provides available comparable data for the CEA sector:

| Company | Revenue (Most Recent Annual / Q1 2026 Equivalent) | Net Income / Loss | Operating Status / Change |

| Local Bounti (LOCL) | $13.3M (Q1 2026) | -$12.7M (Q1 2026) | Active; -66.2% YoY net loss improvement |

| Gotham Greens (Private) | ~$76.9M–$84M (annual est.) | Not publicly disclosed | Active; private company |

| AppHarvest (APPH) | ~$6M (est., pre-bankruptcy) | Negative; undisclosed | Filed Chapter 11 bankruptcy July 2023 |

| Plenty Unlimited (Private) | Not publicly disclosed | Negative | Filed Chapter 11 bankruptcy March 2025 |

| AeroFarms (Private) | ~$15M (est. annual) | Negative | Underwent Chapter 11 restructuring 2023 |

How the Market Reacted?

Local Bounti’s stock (NYSE: LOCL) was trading at approximately $1.41 to $1.44 ahead of and at the close before the Q1 2026 earnings release on May 13, 2026. In extended trading, the stock ticked up to around $1.46, a gain of roughly +1.1%, suggesting the market received the EPS beat and improving EBITDA trajectory with mild optimism.

The sentiment of the report is broadly bullish relative to the company’s historical loss profile, with the net loss narrowing by more than 66% year-over-year and operating expenses falling 10%. However, the revenue miss versus the $19 million consensus estimate is a cautionary signal, and with a market cap of only ~$32 million against total liabilities of over $592 million, investors remain watchful of the company’s path to profitability and balance sheet sustainability.