Citius Pharmaceuticals reported Q2 2026 EPS of $(0.95) on revenue of $1.67 million, sharply below consensus estimates of EPS $0.39 and revenue $18.79 million. Shares traded down about 12% in after-hours movement, reflecting a cautious market response to mounting losses and one-time charges.

About Citius Pharmaceuticals, Inc.

Citius Pharmaceuticals, Inc. is a biopharmaceutical company listed on Nasdaq under the ticker CTXR, focused on developing and commercializing first in class critical care products. The company is headquartered in Cranford, New Jersey, and operates as a majority owner, with roughly 71% stake, in Citius Oncology, Inc., which commercializes the targeted immunotherapy LYMPHIR.

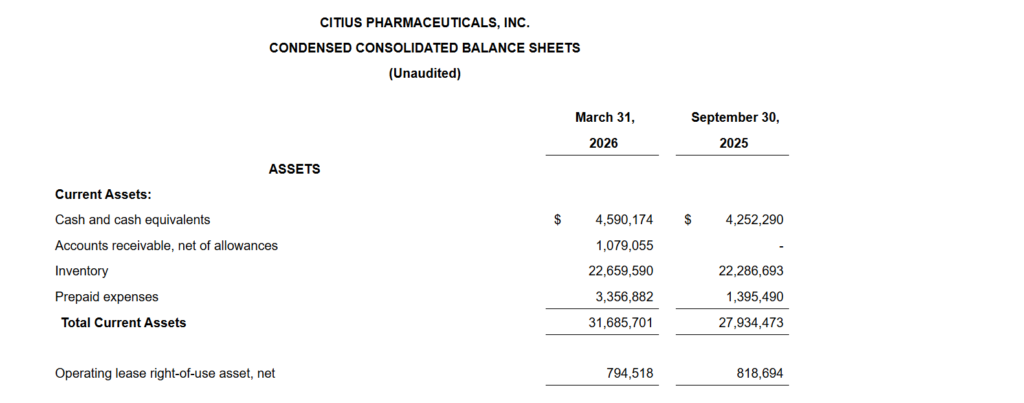

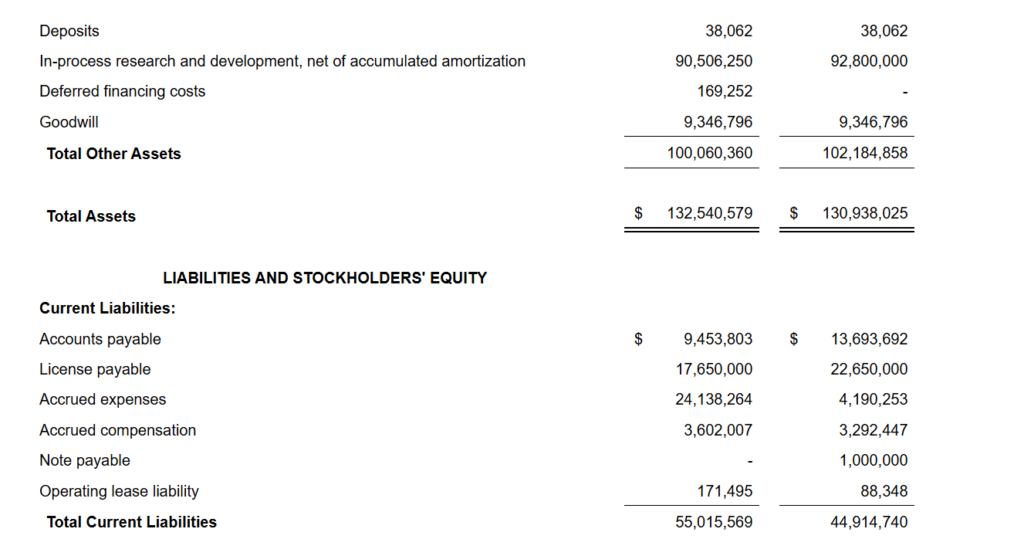

Citius is a clinical and commercial stage business that advances therapies for catheter related bloodstream infections, hemorrhoid treatment and cutaneous T cell lymphoma through assets such as Mino Lok and CITI 002 Halo Lido. As of March 31, 2026, Citius reported total assets of $132.5 million and stockholders’ equity of about $61.5 million attributable to Citius shareholders, reflecting substantial investment in in process R&D valued at over $90.5 million.

Top Financial Highlights

- Net product revenues for Q2 FY 2026 were $1.67 million, versus $0 in the prior year quarter, driven by the ongoing launch of LYMPHIR.

- Net product revenues for the first half of FY 2026 reached $5.6 million, compared with $0 in the first half of FY 2025.

- Gross profit for Q2 FY 2026 was $1.34 million, implying roughly 80% gross margin on LYMPHIR sales.

- Gross profit for the first six months of FY 2026 totaled $4.49 million, also at about 80% margin.

- Research and development expenses fell to $1.63 million in Q2 FY 2026 from $3.77 million a year earlier, reflecting lower clinical development activity.

- General and administrative expenses surged to $26.39 million in Q2 FY 2026 from $4.79 million in Q2 FY 2025, largely due to a $19.7 million one time CMO contract cancellation charge.

- Stock based compensation within G&A rose to $3.79 million in Q2 FY 2026 from $2.70 million in the prior year quarter.

- Total operating expenses in Q2 FY 2026 were $33.53 million, up from about $11.26 million in Q2 FY 2025.

- Net loss applicable to common stockholders for Q2 FY 2026 was $21.23 million, or $(0.95) per share, compared with $10.92 million, or $(1.27) per share, a year earlier.

- For the first half of FY 2026, net loss applicable to common stockholders was $29.45 million, or $(1.34) per share, versus $20.68 million, or $(2.58) per share, in the same period of FY 2025.

- Cash and cash equivalents stood at $4.59 million as of March 31, 2026.

- Subsequent to quarter end, Citius Pharma completed a $5 million registered direct offering, while Citius Oncology secured up to $36.5 million in combined debt and equity financing.

- Management expects the combined companies to have sufficient liquidity to fund operations through November 2026.

- LYMPHIR launch metrics included 83% of target accounts on formulary or in active review and payer coverage for nearly 100% of covered commercial lives, with no reimbursement denials reported.

- LYMPHIR net revenue for the first half of FY 2026 was $5.6 million at approximately 80% gross margin, reflecting four months of commercial sales since its December 2025 launch.

Beat or Miss?

| Metric | Reported | Difference/Analysis |

| EPS | ($0.95) | Missed consensus EPS of $0.39 by $1.34, driven by high G&A and one time charges. |

| Revenue | $1.67 million | Missed expected revenue of $18.79 million by $17.12 million, reflecting early stage LYMPHIR ramp. |

| Gross Margin | ~80% | Healthy margin indicates strong unit economics on LYMPHIR despite low sales scale. |

| Net Income | $(21.23) million | Loss widened versus prior year due to non recurring contract cancellation costs and higher G&A. |

What Leadership Is Saying?

“The first half of fiscal 2026 demonstrated meaningful commercial progress at our majority owned subsidiary Citius Oncology. In the four months of commercial sales since the December 2025 launch of LYMPHIR, Citius Oncology generated $5.6 million in net revenue at approximately 80% gross margins, advanced 83% of target accounts to formulary inclusion or active review, and secured payer coverage representing near 100% of covered commercial lives with no reimbursement denials reported to date. These results reflect our efforts to build a durable patient access foundation upon which to drive growth.”

“Subsequent to quarter end, Citius Oncology secured up to $36.5 million in combined debt and equity financing through its senior secured credit facility and warrant exercises, complemented by Citius Pharma’s $5 million registered direct offering. Together, these proceeds are expected to fund our activities and complete the LYMPHIR commercial field force buildout by mid summer, supporting expanded physician engagement and broader market penetration.”

Historical Performance

| Category | Q2 FY 2026 | Q2 FY 2025 | Change (%) |

| Revenue | $1.67 million | $0 | Not meaningful from zero base. |

| Net income (loss) | $(21.23) million | $(10.92) million | Loss increased about 95% year over year. |

| Operating expenses | $33.53 million | $11.26 million | Operating costs roughly tripled, driven by one time charges and higher G&A |

Historical Performance of Peers (Illustrative)

| Category | Citius Q2 FY 2026 | Peer (Oncology focused microcap)* Q2 Latest | Change (%) vs Citius Trend |

| Revenue | $1.67 million | Low single digit millions | Both show modest early commercial revenue. |

| Net income (loss) | $(21.23) million | Negative, low tens of millions | Loss profile broadly similar in scale to revenue. |

| Operating expenses | $33.53 million | Elevated R&D and G&A | High spend consistent with late stage biotech peers. |

How the Market Reacted?

Citius Pharmaceuticals’ Q2 2026 release coincided with a negative trading reaction, with MarketBeat data showing the stock at $0.70 at the regular close and $0.62 in extended trading, a decline of about 12% after hours. This move follows a period of volatility in the name, with prior reports documenting day to day swings and mixed analyst sentiment.

The combination of a large earnings miss versus expectations, widening losses and reliance on fresh financing likely weighed on investor confidence despite encouraging LYMPHIR launch metrics. Sentiment skews cautious to bearish as investors wait for clearer evidence that growing high margin revenue can offset elevated operating expenses.