Integrated Diagnostics Holdings plc delivered a robust FY 2024, with revenue rising 39% year on year to EGP 5.72 billion and net profit more than doubling to EGP 1.01 billion, supported by margin expansion across the P&L and strong Q4 momentum that sets a constructive tone for FY 2025. EPS and immediate share-price reaction were not disclosed in the release, so after-hours movement is not available.

About Integrated Diagnostics Holdings plc

Integrated Diagnostics Holdings plc (IDH) is a Jersey-registered diagnostics services provider listed on the London Stock Exchange under ticker IDHC. The group operates over 628 branches across Egypt, Jordan, Nigeria, Saudi Arabia and Sudan, offering more than 3,000 clinical pathology and radiology tests under brands including Al Borg, Al Mokhtabar, Biolab, Echo-Lab and Biolab KSA.

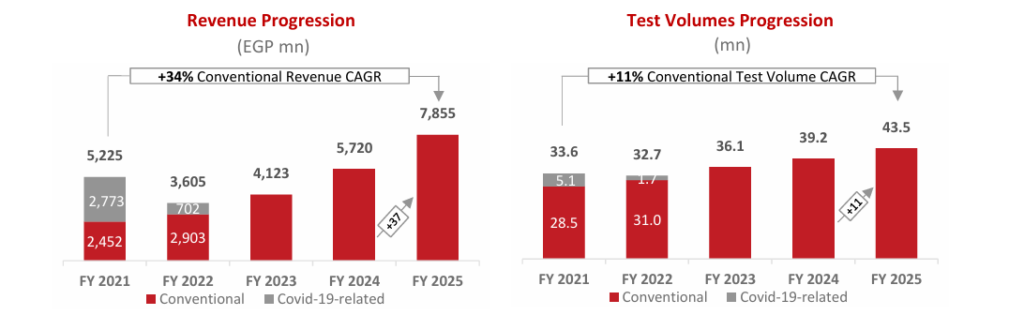

In 2024 IDH served 8.9 million patients and performed 39.2 million tests, highlighting the scale of its regional footprint. While the exact founding year is not specified in the release, the company cites “over 40 years of experience,” pointing to roots in the early 1980s. Market capitalization, P/E ratio, dividend yield and employee count are not disclosed in the FY 2024 results; however, shares outstanding stand at 581,326,272, and the company reiterates its long-standing dividend policy while deferring the FY 2024 payout decision until after its half‑year 2025 results.

Top Financial Highlights

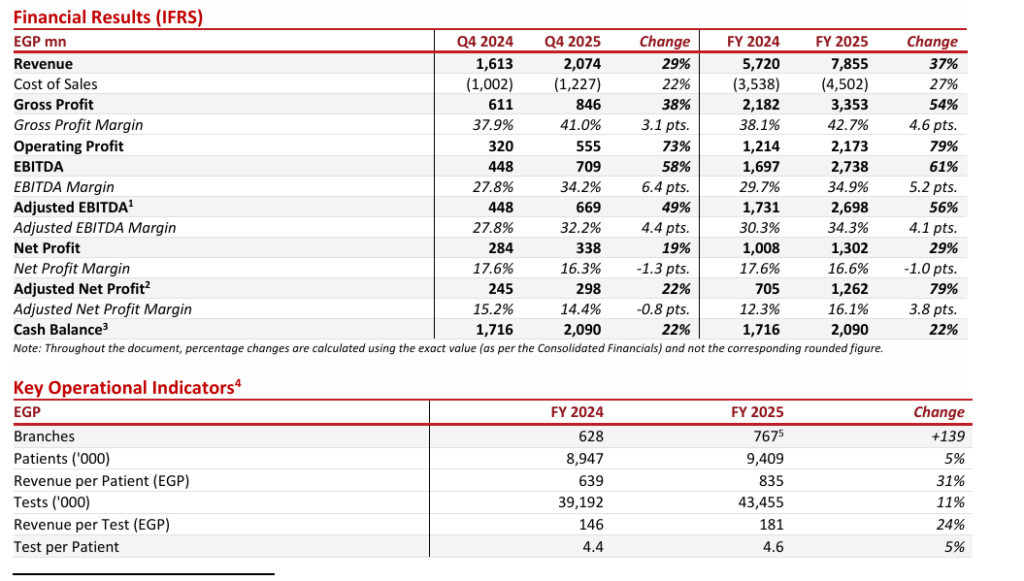

- Revenue reached EGP 5,720 million in FY 2024, up 39% from EGP 4,123 million in FY 2023.

- Net profit (profit after tax) rose to EGP 1,008 million, an increase of 115% from EGP 468 million a year earlier, with net margin improving to 17.6% from 11.4%.

- Q4 2024 revenue was EGP 1,613 million, up 51% year on year and the highest quarterly revenue in the year.

- Q4 2024 net profit came in at EGP 284 million, rising 251% from Q4 2023, with a quarterly net margin of 17.6% versus 7.6% a year earlier.

- Gross profit for FY 2024 was EGP 2,182 million, up 43%, with gross margin expanding to 38.1% from 37.0%.

- Operating profit increased to EGP 1,214 million in FY 2024 from EGP 738 million, a 65% rise.

- Adjusted EBITDA reached EGP 1,731 million in FY 2024, up 45%, and the adjusted EBITDA margin improved to 30.3% from 28.9%.

- Cash balance more than doubled to EGP 1,716 million at year end, a 105% increase from EGP 835 million in FY 2023.

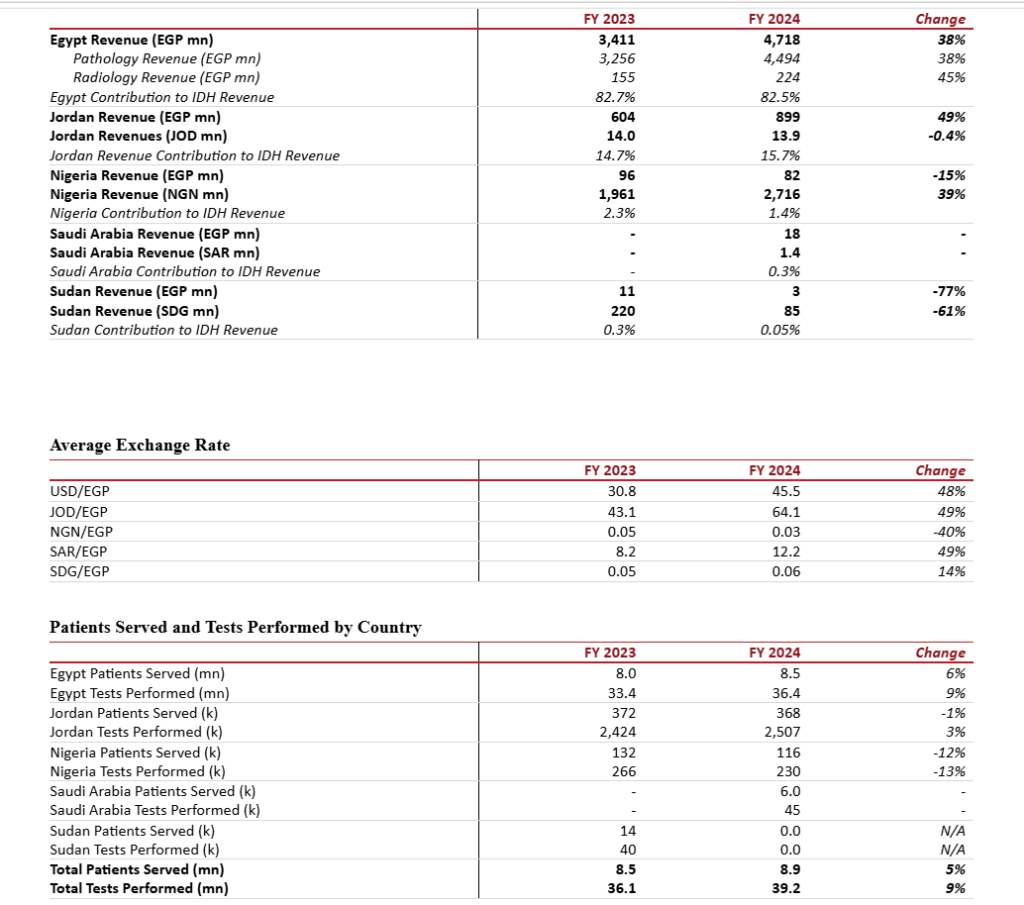

- Egypt, representing 82.5% of revenue, generated EGP 4,718 million in FY 2024, up 38%, supported by 9% growth in tests and 27% higher revenue per test.

- Jordan revenue was JOD 13.9 million (stable in local currency), translating to EGP 899 million, up 49% in EGP terms due to FX effects.

- Nigeria delivered NGN 2,716 million in revenue, up 39%, though in EGP terms revenue fell 15% to EGP 82 million on Naira weakness.

- Saudi Arabia (Biolab KSA), launched in 2024, generated SAR 1.4 million of revenue and performed 45 thousand tests, with Q4 revenue of SAR 0.625 million, up 39% quarter on quarter.

- Branch network expanded to 628 branches, a net increase of 27 sites, including 43 new branches in Egypt and two in Saudi Arabia, while most Sudan branches remain closed.

- Operational metrics improved: tests increased 9% to 39.2 million, patients rose 5% to 8.9 million, revenue per test climbed 28% to EGP 146, and tests per patient rose to 4.4 from 4.2.

- FX gains of EGP 303 million (up 245%) and a 41% drop in net interest expense supported bottom-line growth, while management notes that even excluding FX gains net profit would have risen 85% year on year.

Revenue Contribution by Country

Beat or Miss?

| Metric | Reported FY 2024 | Difference / Analysis |

| Revenue | EGP 5,720 mn | Strong 39% YoY growth driven by 9% higher test volumes and 28% higher revenue per test. |

| Net profit | EGP 1,008 mn | 115% YoY increase; margin expanded from 11.4% to 17.6%, aided by FX gains and lower net interest expense. |

| Adjusted EBITDA | EGP 1,731 mn | 45% YoY growth and margin improvement to 30.3%; reflects cost optimization and operating leverage. |

| Gross profit | EGP 2,182 mn | 43% YoY growth with gross margin up 1.2 percentage points to 38.1%. |

| Cash balance | EGP 1,716 mn | 105% YoY increase, indicating stronger liquidity and balance sheet flexibility. |

| EPS | N/A | Not disclosed in the FY 2024 press release. |

| Dividend per share | Deferred decision | Board deferred FY 2024 dividend declaration until after H1 2025 results. |

What Leadership Is Saying?

“As I reflect back on 2024, I am proud of all that IDH has been able to achieve despite the significant operational challenges that the business continued to face across its growing footprint. Over the past twelve months, we made notable progress on all key pillars of our growth and value creation strategy… we enter the new year stronger and leaner than ever, well-placed to continue capturing growth opportunities across our more mature and newer markets while driving positive impacts in the communities where we operate.”

– Dr. Hend El‑Sherbini, CEO“His extensive experience in Egypt and neighbouring markets has already proven indispensable, helping us successfully navigate the challenges faced across our markets over the past year.” – Board commentary on CFO Sherif El Zeiny’s role in steering financial and risk management

Historical Performance

FY 2024 vs FY 2023 (YoY)

| Category | FY 2024 | FY 2023 | Change (%) |

| Revenue | EGP 5,720 mn | EGP 4,123 mn | 39% |

| Gross profit | EGP 2,182 mn | EGP 1,524 mn | 43% |

| Operating profit | EGP 1,214 mn | EGP 738 mn | 65% |

| Net profit | EGP 1,008 mn | EGP 468 mn | 115% |

| Adjusted EBITDA | EGP 1,731 mn | EGP 1,192 mn | 45% |

| Cash balance | EGP 1,716 mn | EGP 835 mn | 105% |

| Patients (000s) | 8,947 | 8,512 | 5% |

| Tests (000s) | 39,192 | 36,102 | 9% |

Q4 2024 vs Q4 2023

| Category | Q4 2024 | Q4 2023 | Change (%) |

| Revenue | EGP 1,613 mn | EGP 1,069 mn | 51% |

| Gross profit | EGP 611 mn | EGP 387 mn | 58% |

| Net profit | EGP 284 mn | EGP 81 mn | 251% |

How the Market Reacted?

The FY 2024 results announcement focuses on operating and financial performance and does not mention the share price reaction on the London Stock Exchange. Based on the strong double‑digit growth in revenue, adjusted EBITDA and net profit, alongside margin expansion and a sizeable increase in cash balances, the overall tone of the release is constructive and management’s outlook is cautiously optimistic heading into 2025.

However, risks remain from macroeconomic volatility in Egypt and Nigeria and ongoing conflict in Sudan and parts of the wider region, which management acknowledges as continuing headwinds. In absence of explicit trading data, the immediate after‑hours stock movement cannot be assessed from the announcement.