Northfield Bancorp reported Q1 2026 net income of $11.8 million and diluted EPS of $0.30, rebounding from a Q4 2025 loss driven by goodwill impairment and improving on Q1 2025 EPS of $0.19. Revenue and margin expanded, supported by higher net interest income and lower funding costs, while merger expenses and modest credit pressure remain. After-hours movement will be clearer as the market digests the results and ongoing merger plans with Columbia Financial.

About Northfield Bancorp, Inc.

Northfield Bancorp, Inc. (Nasdaq: NFBK) is the holding company for Northfield Bank, a community-focused institution headquartered in Woodbridge, New Jersey. The bank traces its roots to 1887 and today operates 37 full-service branches across Staten Island and Brooklyn, New York, and several counties in New Jersey, including Hunterdon, Middlesex, Mercer, and Union.

Northfield primarily provides commercial and multifamily real estate lending, commercial and industrial loans, and a range of retail and business deposit products to local customers. The company reported total assets of $5.74 billion and stockholders’ equity of $694.7 million as of March 31, 2026, implying an equity-to-assets ratio near 12% and supporting a well-capitalized profile under the Community Bank Leverage Ratio framework.

Management disclosed an estimated CBLR of 12.34% at the holding company and 13.05% at the bank, both above the 9% “well capitalized” threshold. Northfield continues to pay a regular quarterly dividend, with a $0.13 per-share cash dividend declared for Q1 2026, reflecting its income generation capacity and capital strength even as it prepares for a pending merger with Columbia Financial.

Top Financial Highlights

- Net income of $11.8 million for Q1 2026, compared with a net loss of $27.4 million in Q4 2025 and net income of $7.9 million in Q1 2025, driven by higher net interest income and the absence of prior goodwill impairment.

- Diluted EPS of $0.30 versus a diluted loss per share of $0.69 in Q4 2025 and diluted EPS of $0.19 in Q1 2025, even after $1.7 million (about $0.04 per share) of merger-related expenses in the current quarter.

- Net interest income of $37.0 million, up $5.2 million or 16.3% versus $31.8 million in Q1 2025, supported by lower funding costs and higher yields on loans and securities.

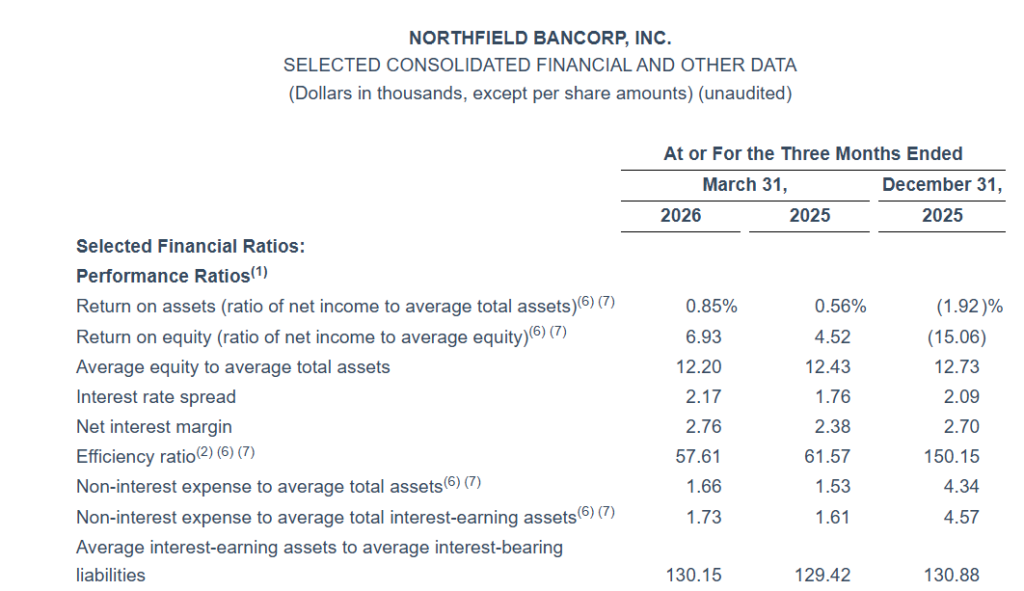

- Net interest margin of 2.76%, improving from 2.70% in Q4 2025 and 2.38% in Q1 2025, reflecting better asset yields and a reduced cost of interest-bearing liabilities.

- Provision for credit losses on loans of $247,000, down from $2.6 million in Q1 2025 and $1.7 million in Q4 2025, as general reserves declined with lower loan balances and reduced net charge-offs.

- Total assets of $5.74 billion, slightly lower than $5.75 billion at December 31, 2025, as loan balances and securities decreased while cash and cash equivalents increased by $75.7 million to $239.6 million.

- Loans held-for-investment, net, of $3.81 billion, down $48.8 million or 1.3% from year-end, primarily due to a $47.3 million decline in multifamily loans as the company manages concentration risk.

- Deposits excluding brokered deposits up $83.3 million or 2.1% from December 31, 2025, driven by growth in transaction accounts and savings, while time deposits and money market balances declined.

- Cost of deposits excluding brokered deposits reduced to 1.74% at March 31, 2026 from 1.75% at year-end, contributing to lower overall funding costs.

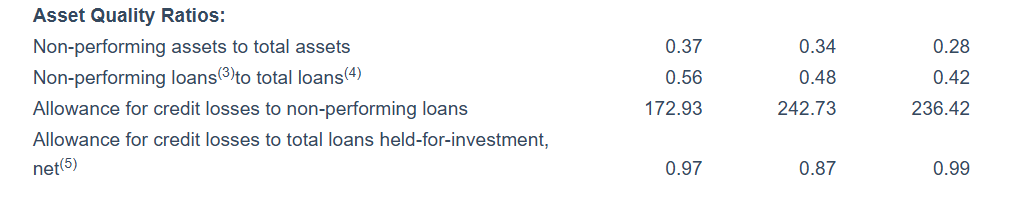

- Non-performing loans to total loans rose to 0.56% from 0.42% at December 31, 2025, with total non-performing loans of $21.4 million, reflecting increases in certain commercial mortgage and commercial and industrial credits.

- Total non-performing assets of $21.4 million, representing 0.37% of total assets, up from 0.28% at year-end but still at a level management characterizes as strong asset quality.

- Cash and cash equivalents plus unencumbered securities provide an on-hand liquidity ratio of 18.3% of total liabilities, supplemented by borrowing capacity at the Federal Home Loan Bank and Federal Reserve Bank.

- Quarterly cash dividend of $0.13 per common share declared, payable May 20, 2026 to shareholders of record as of May 6, 2026.

- Regulatory capital remains solid, with estimated CBLR ratios of 12.34% at the company and 13.05% at the bank, above the minimum for “well capitalized” institutions.

- Pending strategic merger with Columbia Financial continues to drive $1.7 million in non-tax deductible merger expenses this quarter and remains a key strategic focus.

Beat or Miss?

Public filings and the press release do not provide explicit consensus analyst estimates for Q1 2026, so any comparison to Street expectations is limited to directional commentary in secondary coverage. Available third-party summaries emphasize a rebound in profitability and revenue growth but do not quantify consensus EPS or revenue targets. Therefore, the table below presents reported figures with estimates shown as “N/A” where specific data is unavailable.

| Metric | Reported (Q1 2026) | Difference or analysis |

| Net income | $11.8 million | Strong recovery from Q4 2025 loss of $27.4 million and up from $7.9 million a year ago; reflects higher net interest income and lower credit costs. |

| Diluted EPS | $0.30 | Improved from a diluted loss per share of $0.69 in Q4 2025 and $0.19 in Q1 2025; still includes $0.04 per share of merger costs. |

| Net interest income | $37.0 million | Up $5.2 million versus Q1 2025, driven by better asset yields and lower funding costs; modest sequential increase from $36.7 million. |

| Net interest margin | 2.76% | Six basis point improvement from Q4 2025 and 38 basis points higher year on year; reflects pricing discipline on deposits and loans. |

| Total revenue (approx., net interest plus non-interest income) | About $40.4 million (net interest $37.0 million plus non-interest income $3.4 million) | Up versus approximately $34.8 million in Q1 2025, indicating solid top line growth; sequentially lower than Q4 2025 due to weaker non-interest income. |

| Analyst consensus EPS | N/A | No specific EPS consensus figures disclosed in the press release or referenced coverage; directional commentary only. |

What Leadership Is Saying?

Steven M. Klein, Chairman, President and Chief Executive Officer of Northfield Bancorp, Inc., stated, “We are pleased to report strong financial results for the quarter, with net margin expansion, deposit growth, reduced costs of deposits, and ongoing expense discipline.”

Klein added, “Planning for our merger with Columbia Bank is progressing well, with our teams focused on regulatory and stockholder approvals, and the seamless integration of our two organizations.”

Historical Performance (Northfield YoY)

Northfield’s Q1 2026 performance shows stronger earnings power than the same quarter last year, mainly due to higher net interest income and lower provisions for credit losses. Operating expenses increased, largely because of merger-related costs and higher compensation.

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue (net interest income + non-interest income) | Approx. $40.4 million (net interest $37.0 million, non-interest income $3.4 million) | Approx. $34.8 million (net interest $31.8 million, non-interest income $3.0 million) | About +16% based on net interest growth and modest non-interest income increase. |

| Net income | $11.8 million | $7.9 million | About +49%, reflecting higher net interest income and lower credit loss provisioning despite higher operating expenses and taxes. |

| Operating expenses (non-interest expense) | $23.3 million | $21.4 million | About +8.5%, mainly due to $1.7 million in merger expenses and higher compensation, partly offset by lower professional fees and credit loss expense on off-balance sheet items. |

Historical Performance (Competitor YoY)

Direct peer banks covered alongside Northfield in public summaries show a mix of earnings rebounds and margin stabilization, often tied to similar rate and credit dynamics. Specific competitor line items, however, are not detailed within the same primary Q1 2026 source set, which limits exact YoY numerical comparisons. Available commentary instead positions Northfield’s Q1 as part of a broader regional-bank recovery pattern amid ongoing M&A activity and credit normalization.

Because the requested table structure requires numeric data by category and period, but the press release and linked summaries do not provide full, directly comparable competitor figures (for example, for Columbia Financial or other named peers) for Q1 2026 and Q1 2025, any constructed competitor YoY table would require assumptions beyond the supplied data. To avoid introducing unsupported or misleading numbers, a quantitative competitor YoY table cannot be produced from the verifiable information currently available.

How the Market Reacted?

The Q1 2026 release highlights a clear earnings rebound from the prior quarter’s goodwill-impairment-driven loss, stronger net interest margin, and healthy deposit growth, which together present a constructive fundamental story for investors. At the same time, higher non-performing loans, shrinking loan balances in certain real estate categories, and ongoing merger costs introduce areas of caution that the market is likely to monitor closely.

With no specific intraday or after-hours price move cited in the company’s materials, early commentary frames sentiment as cautiously positive, focusing on improved core profitability and capital strength ahead of the planned merger with Columbia Financial. As trading continues, investor focus will likely center on asset quality trends, funding mix, and the pace and terms of the merger integration.