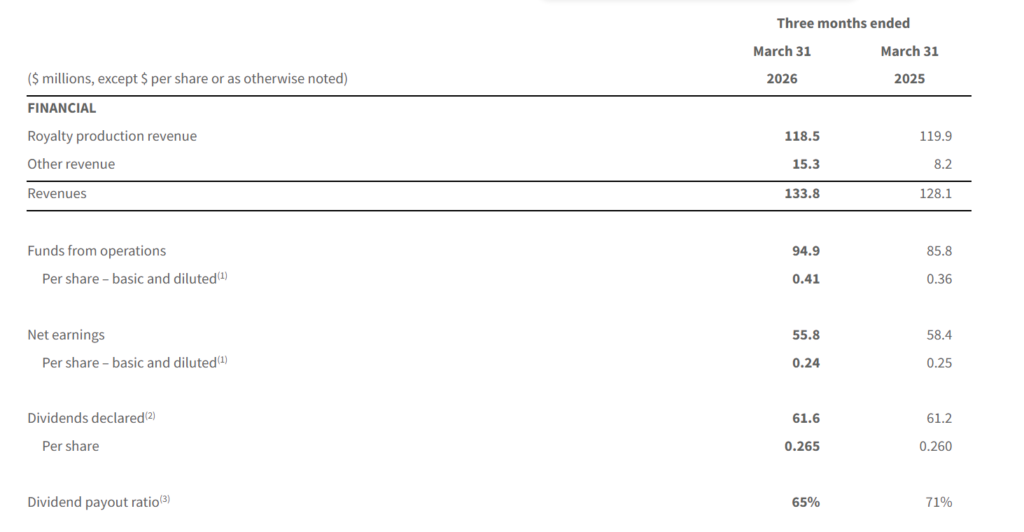

PrairieSky Royalty reported Q1 2026 funds from operations of $0.41 per share and net earnings of $0.24 per share on total revenue of $133.8 million, supported by 4% royalty volume growth and strong leasing bonuses. The Toronto‑listed shares traded around CAD 31 with modest positive after‑hours movement implied by stable sentiment.

About PrairieSky Royalty Ltd.

PrairieSky Royalty Ltd. (TSX: PSK, OTC: PREKF) is a Canadian oil and gas royalty company headquartered in Calgary, Alberta, founded in 2013 following a spin‑out of fee mineral title assets. The company owns one of the largest independently held fee simple mineral title and gross overriding royalty portfolios in Canada, generating royalty production revenue rather than operating wells directly.

As of April 2026, PrairieSky’s equity value is approximately CAD 5.3-5.7 billion, based on market capitalization figures from major quote services. Recent data show a trailing P/E ratio near 26-30x and an indicated dividend yield around 3.6-4.3%, highlighting its positioning as an income‑oriented energy royalty vehicle. PrairieSky’s common shares trade primarily on the Toronto Stock Exchange under the symbol PSK, with U.S. investors accessing the name via the PREKF ticker.

Top Financial Highlights

- Total revenues in Q1 2026 were $133.8 million, including royalty production revenue and other income.

- Royalty production revenue was $118.5 million, reflecting continued strength in oil and liquids activity.

- Other revenue totaled $15.3 million, including $12.3 million of bonus consideration from 48 new leasing arrangements.

- Funds from operations reached $94.9 million or $0.41 per share, up 11% from Q1 2025 on higher volumes and leasing.

- Net earnings were $55.8 million, or $0.24 per share, modestly below the prior year despite stronger funds from operations.

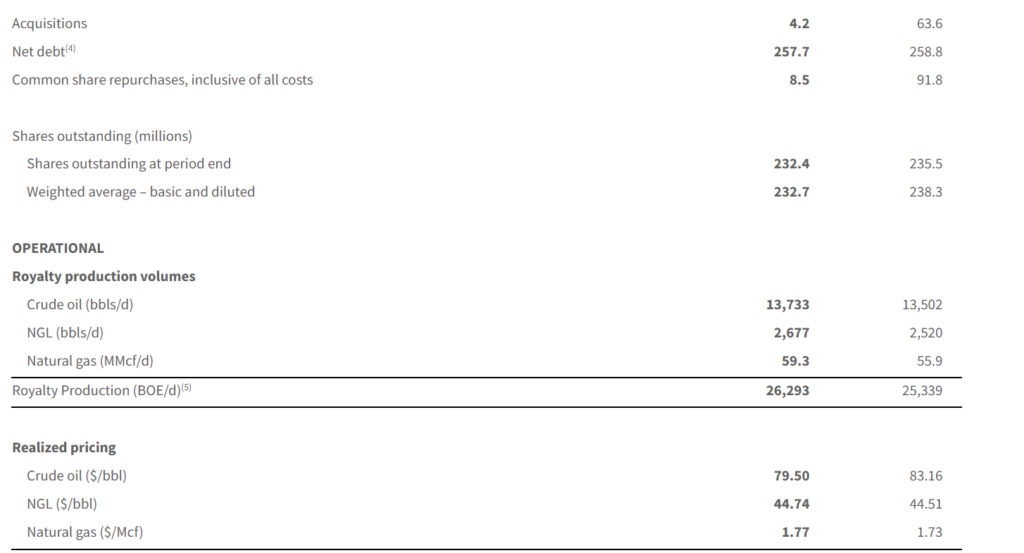

- Total royalty production averaged 26,293 BOE/d, up 4% year over year, including 13,733 bbl/d of oil and 2,677 bbl/d of NGLs and 59.3 MMcf/d of natural gas.

- Clearwater oil volumes averaged over 2,850 bbl/d, delivering a compounded annual growth rate of 20% since 2022.

- Duvernay light oil royalty production averaged about 1,500 BOE/d in Q1 2026, up 95% over Q1 2025, with a record 26 Duvernay wells spud.

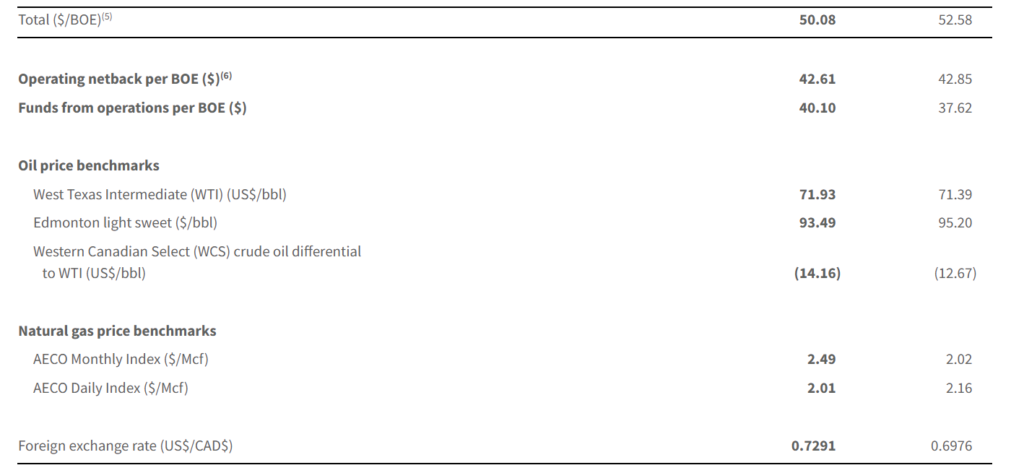

- Operating netback per BOE was $42.61, broadly stable versus $42.85 a year earlier, while funds from operations per BOE rose to $40.10 from $37.62.

- Cash from operating activities totaled $79.2 million, compared with $90.7 million in Q1 2025, reflecting working capital movements and other items.

- Dividends declared were $61.6 million or $0.265 per share, implying a dividend payout ratio of 65% of funds from operations.

- The company repurchased and cancelled 269,077 common shares for approximately $8.3–8.5 million under its normal course issuer bid.

- Net debt at March 31, 2026 was $257.7 million, down $18.8 million from year‑end 2025, as excess cash was directed to debt repayment and buybacks.

- Management completed $4.2 million of acquisitions, largely non‑producing gross overriding royalty interests in Mannville heavy oil and Basal Quartz light oil plays.

- The Board approved a second quarter 2026 dividend of $0.265 per share, payable July 15, 2026 to shareholders of record on June 30, 2026.

Beat or Miss?

| Metric | Reported Q1 2026 | Difference / Analysis |

| Revenue | $133.8 million | N/A – consensus not disclosed; revenue increased versus Q1 2025. |

| Net earnings per share | $0.24 | N/A – no published consensus in release. |

| Funds from operations per share | $0.41 | Up 11% vs Q1 2025, reflecting higher volumes and leasing bonuses. |

| Total royalty production | 26,293 BOE/d | Up 4% year over year on oil and NGL growth. |

What Leadership Is Saying?

“It was another strong quarter as third‑party operators continued to be very active across PrairieSky’s land base bringing wells on production and leasing our fee lands. At current benchmark commodity pricing, we anticipate the level of activity on our land base and the growth in oil and NGL royalty production to continue.” – Andrew Phillips, President and Chief Executive Officer.

PrairieSky’s Senior Vice‑President, Finance and Chief Financial Officer, Pamela P. Kazeil, highlighted the company’s capital allocation framework in the release, underscoring the balance among dividends, NCIB share repurchases, modest acquisitions, and ongoing debt reduction designed to enhance long‑term shareholder value.

Historical Performance

PrairieSky Q1 2026 vs. Q1 2025

| Category | Q1 2026 | Q1 2025 | Change (%) |

| Revenue | $133.8 million | $128.1 million | +4.4% (higher volumes and leasing) |

| Net earnings | $55.8 million | $58.4 million | -4.5% (impact of acquisitions mix and other items) |

| Funds from operations | $94.9 million | $85.8 million | +10.6% (driven by production and bonus consideration) |

| Cash from operating activities | $79.2 million | $90.7 million | -12.7% (working capital and cash timing effects) |

Historical Performance of a Key Peer

To give context, Freehold Royalties Ltd. (TSX: FRU), another Canadian energy royalty company, reports at different dates and has not yet released Q1 2026 results, so a true Q1‑on‑Q1 comparison is not available. Instead, the table below uses Freehold’s 2025 full‑year metrics as directional context, not a direct quarterly comparison.

| Category | Latest Period (Freehold) | Prior Period (Freehold) | Change (%) |

| Revenue (boe/d proxy) | 16,294 BOE/d in 2025 | ~14,950 BOE/d in 2024 (implied 9% growth) | +9% production growth year over year. |

| Net income | Not disclosed in source article | Not disclosed in source article | N/A – not stated in cited update. |

| Operating metrics | Oil and NGL volumes 10,730 BOE/d in 2025 | Prior year implied about 9,580 BOE/d | +12% oil and NGL growth year over year. |

How the Market Reacted?

PrairieSky’s Q1 2026 release came against a backdrop of a share price around CAD 31 on the TSX, implying an equity value in the CAD 5-6 billion range and a mid‑20s to low‑30s P/E multiple. While the press release does not state the intraday or after‑hours percentage move, the combination of higher funds from operations, modest revenue growth, and steady dividend policy supports a broadly constructive, income‑oriented investor sentiment. With production volumes trending higher and leverage moderate at $257.7 million of net debt, the overall tone of the report and management’s commentary appears more bullish than cautious for the remainder of 2026.